Open Banking in Germany: Coverage and Provider Fit

Germany is where many EU payment roadmaps start — large banked population, strong mobile banking, and high B2B invoice volume — yet “open banking Germany” on a provider slide rarely matches what your customers experience in production. Coverage gaps, corporate account quirks, and different buyer behaviour than the UK or Nordics all show up in conversion and reconciliation metrics, not in marketing maps. This guide explains what German open banking is good for in B2B contexts, how to sanity-check coverage claims, and which provider evaluation questions matter before you commit budget.

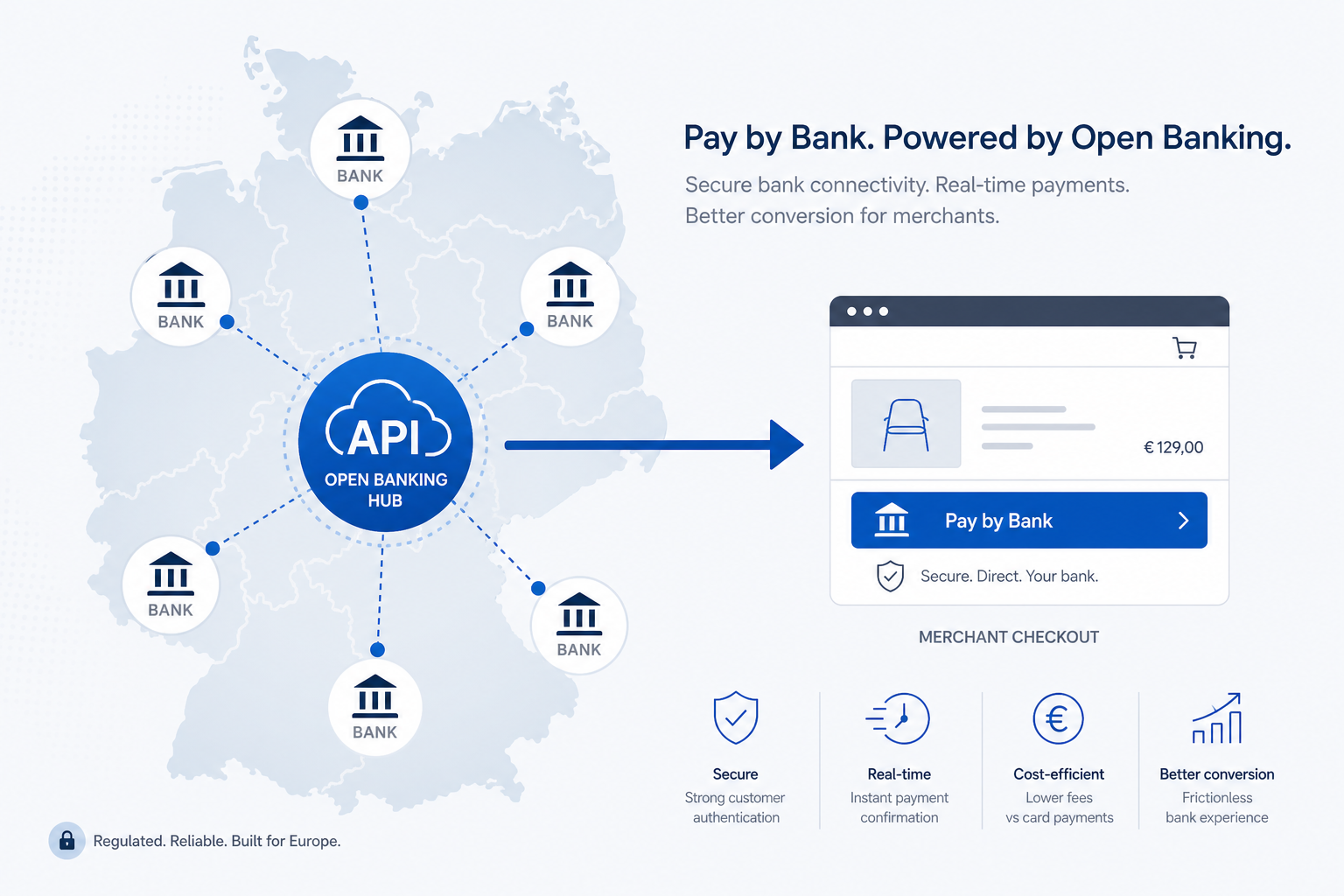

Open banking in Germany: Connecting to German banks through regulated APIs so your business can verify accounts, initiate customer payments, read consented transaction data, and reconcile cash — with customers approving access in their banking app.

Why Germany is a priority market — and a distinct one

German buyers and borrowers already pay by bank transfer for invoices, rent, and B2B procurement. Open banking productises that behaviour: instant confirmation at checkout, verified IBANs at onboarding, and structured feeds for finance instead of PDF uploads.

What makes Germany distinct for integrators:

- High retail bank concentration — a short list of institutions drives most consumer volume; winning them matters more than long tail checkboxes

- Strong mobile banking — authentication often completes in the banking app, which helps Pay by Bank UX when flows are mobile-first

- B2B Girokonto complexity — business accounts and authorisation patterns differ from consumer salary accounts; verify corporate coverage explicitly

- SEPA Instant adoption — instant settlement is valuable for open banking for marketplaces payouts and treasury, but participation still varies by bank pair

Germany-strong is not EU-strong. Treat France, Italy, or Poland as separate acceptance tests even if your contract says “Europe.”

What German open banking is used for in B2B

Teams operating in Germany typically prioritise these outcomes:

| Use case | Business outcome |

|---|---|

| Pay by Bank checkout | Lower cost per payment, immediate confirmation on eligible flows |

| Account verification | Fewer wrong-IBAN payouts and onboarding fraud |

| Invoice and B2B collection | Match incoming transfers to invoice IDs faster |

| Lending and onboarding | Bank-verified income and affordability — see open banking for lending |

| Marketplace payouts | Seller disbursement over SEPA with verified accounts |

| Recurring collection | First payment via bank app, renewals via SEPA Direct Debit where supported |

Retail-framed guides like open banking for e-commerce and pay by bank apply rail mechanics; German B2B teams add invoice references, ERP reconciliation, and corporate payer workflows on top.

Coverage: how to read provider claims honestly

Marketing materials cite “2,000+ banks” across Europe. For Germany, ask narrower questions:

- Which German institutions cover >80% of your user base? — list them by name, not percentage alone.

- Retail vs business accounts — does verification and payment initiation work on the Girokonto types you onboard?

- Redirect vs embedded UX — what does the customer see on mobile for each major bank?

- Downtime history — incident transparency for Deutsche Bank, Sparkassen groups, ING, Commerzbank, DKB, and neobanks you actually see in data.

- Instant vs standard SEPA — when Instant fails, what fallback timing do you communicate to treasury?

Run sandbox tests with real internal accounts at your top ten customer or borrower banks before shortlisting vendors. A provider optimised for UK open banking will not automatically feel native in Germany.

Regulatory context in plain terms

German open banking sits on EU payment rules implemented nationally — customers must consent, strong authentication applies for access and payments, and regulated providers hold the licences to call bank APIs on your behalf.

For B2B buyers this means:

- You usually integrate a licensed partner rather than becoming a payment institution on day one.

- Purpose and consent copy must match what you do (checkout vs lending vs verification).

- Data residency expectations are stricter in enterprise procurement — confirm EU hosting and subprocessors.

One authoritative overview: BaFin supervises German financial institutions; your provider should document how they meet local and EU requirements without you holding the licence directly. This is context for procurement, not a substitute for legal review.

Provider evaluation questions for the German market

Use this checklist in RFPs and technical diligence — score answers with evidence, not slides.

Coverage and reliability

- Name the top 15 German ASPSPs you support in production, with go-live dates.

- What is your measured success rate for payment initiation on those banks (last 90 days)?

- How do you handle bank maintenance windows and degraded modes?

Products your roadmap needs

- Pay by Bank: mobile deep links, QR, desktop redirect behaviour per major bank.

- Account verification: name–IBAN match rates on retail and business accounts.

- AIS depth: transaction history length, categorisation for lending or reconciliation.

- Payouts: outbound SEPA and Instant coverage for marketplace or lender disbursement.

- Recurring: SEPA Direct Debit mandate support after first authenticated payment.

Integration and ops

- Sandbox parity — do German banks in sandbox match production behaviour?

- Webhook delivery guarantees, retries, and signing for finance automation.

- Reference field rules compatible with German invoice numbers and ERP imports.

- Support SLAs in CET business hours for production incidents.

Commercial and risk

- Pricing model for successful vs failed initiation attempts.

- EU data residency, ISO 27001 / SOC 2, and subprocessors list.

- Sector acceptance: marketplaces, lenders, insurers, SaaS — named in contract.

- Exit terms and portability if you change provider after go-live.

No provider wins every German use case; matching depends on whether you optimise checkout conversion, lending data depth, or B2B payout reliability.

Common German deployment patterns

E-commerce and marketplaces — Pilot Pay by Bank on high-AOV DE baskets with card fallback; add seller verification before scaling weekly payouts. Cross-read open banking for marketplaces.

SaaS and B2B platforms — Verify Girokonto on annual invoice setup; collect first payment via bank app; move renewals to direct debit where mandates are supported. See open banking for SaaS platforms.

Lenders — Income verification on supported banks first; expand affordability and collections once consent renewal is automated. See income verification open banking.

Fintech infrastructure — If Germany is your launch market, treat connectivity depth as the product — see open banking for fintech for multi-market expansion after DE works.

Frequently Asked Questions

What is open banking in Germany?

Open banking in Germany is regulated API access to German bank accounts so businesses can verify accounts, initiate customer payments, and read consented transaction data — with customers approving in their banking app, usually via a licensed provider.

Is open banking widely used in Germany?

Adoption is strong relative to many EU markets for Pay by Bank and account verification, especially where mobile banking is common. Uniform “every bank, every flow” coverage does not exist — pilot and measure on your customer bank mix.

Do I need a German licence to use open banking?

Most non-bank businesses integrate a licensed open banking provider that holds the required EU authorisations. Your legal team confirms whether your specific model needs additional licensing beyond that partnership.

How is German open banking different from the UK?

The UK uses a separate open banking standard and regulator post-Brexit. EU PSD2 rules apply in Germany; technical stacks, bank lists, and contracts do not transfer one-to-one. Run separate integrations or providers if you need both markets.

Which German banks matter most for coverage?

Depends on your segment — consumer lenders care about retail neobanks and Sparkassen reach; B2B invoice platforms care about business Girokonto support. List the banks your users actually hold and test those in sandbox.

Can open banking replace cards in Germany?

For many flows it supplements rather than replaces cards — especially where customers expect card chargeback habits or international buyers use non-German banks. Most teams run dual rails with data-driven routing.

How do I evaluate open banking providers for Germany?

Demand named bank coverage, sandbox proof on your top institutions, success-rate data, business-account support, Instant payout honesty, EU hosting, and sector fit in contract. Weight criteria by your primary use case — checkout vs lending vs payouts.

Closing thought

Open banking Germany rewards specificity: name the banks your customers use, test business accounts if you are B2B, and separate marketing coverage from production success rates. Once German flows work, expand to the next EU country with the same discipline — not the assumption that one “EU” integration behaves identically everywhere.

Related articles

- Open Banking UK vs EU: What B2B Teams Need to Know

Your product roadmap probably mentions "Europe" as one market — but open banking UK vs EU is not a single integration. UK and EU buyers use different bank apps…

- Open Banking Providers Nordics: Coverage Guide (2026)

Open banking providers nordics buyers care about one thing first: whether pay by bank and account verification work on the banks their customers actually use i…

- Recurring Pay by Bank: UK Variable Billing on Bank Rails

Billing teams lose margin when every renewal runs on a card that expires, and they lose days of cash visibility when Direct Debit returns land late. Recurring…