Open Banking for SaaS: 8 Use Cases for EU Platforms

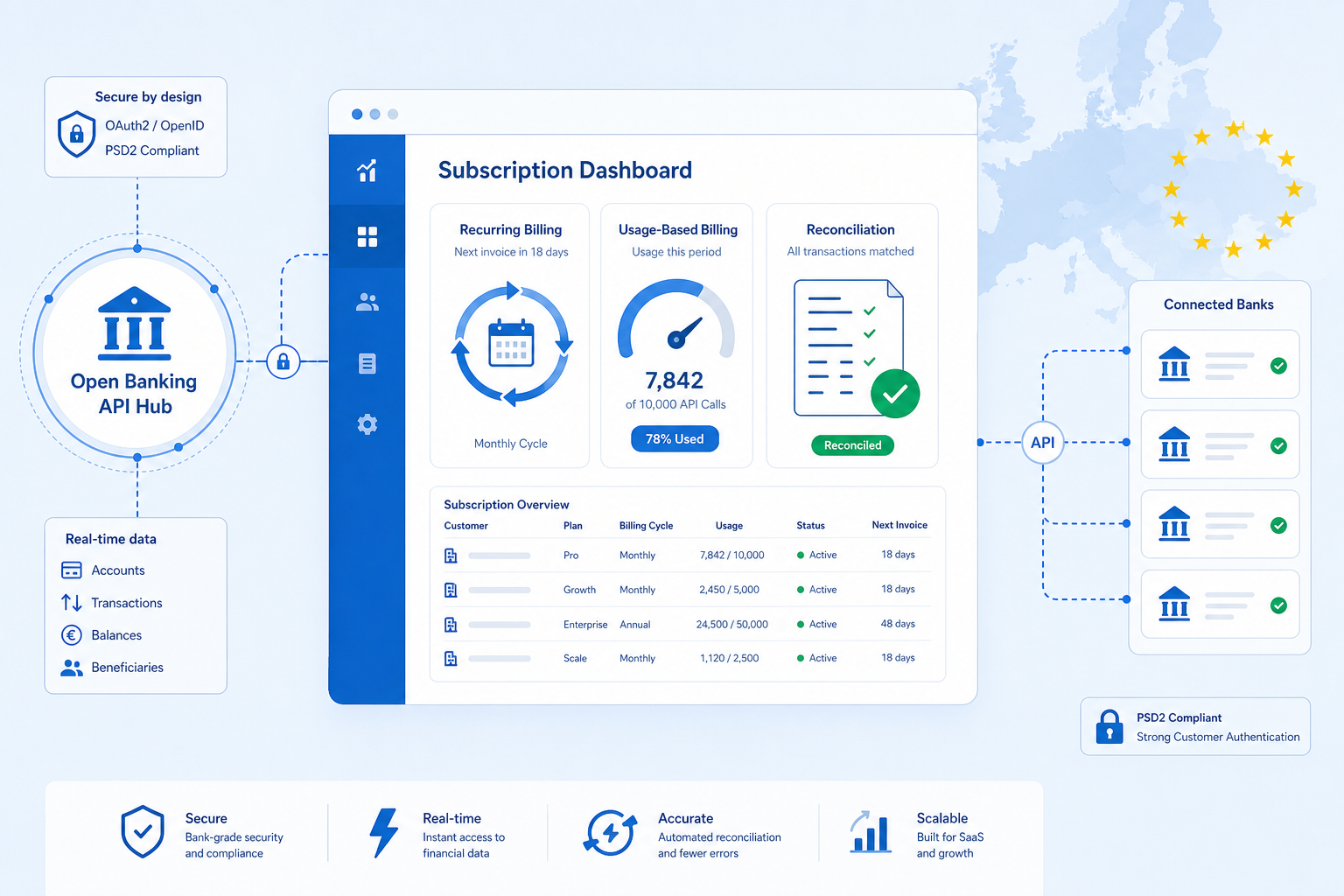

EU SaaS platforms billing thousands of subscriptions hit the same wall: cards expire and kill renewals, usage invoices change every month, and finance still matches bank lines to invoice numbers by hand. Open banking for SaaS lets you collect from customer bank accounts, verify those accounts, and reconcile payments to subscriptions — usually through one provider integration instead of wiring up every EU bank yourself. Customers consent in their banking app; you get confirmation, references, and data your billing system can use. Below are eight use cases operators ship today, how they differ from open banking for fintech (where payments are the product), and a sensible order to roll them out.

Open banking for SaaS: Collecting subscriptions and variable charges from customer bank accounts, verifying account ownership, setting up recurring collection, and matching inbound cash to invoices — without relying only on cards or manual transfers.

Why open banking matters for SaaS specifically

SaaS revenue is recurring and operational. Invuntary churn from failed card payments, usage true-ups that do not fit a stored card, and B2B customers who pay by transfer with useless references all hit the same teams — billing, finance, and support.

Open banking addresses outcomes those teams measure:

- Less involuntary churn when collection runs on a verified bank account and mandate, not an expiring card

- Usage and true-up invoices collected without waiting for manual transfers

- Hours back for finance when payments auto-match to subscription and invoice IDs

- Fewer wrong-IBAN disasters on large B2B annual deals

You typically integrate a licensed open banking provider — you do not need to become a bank. Your product stays software; payments become a managed rail.

1. Recurring subscription collection

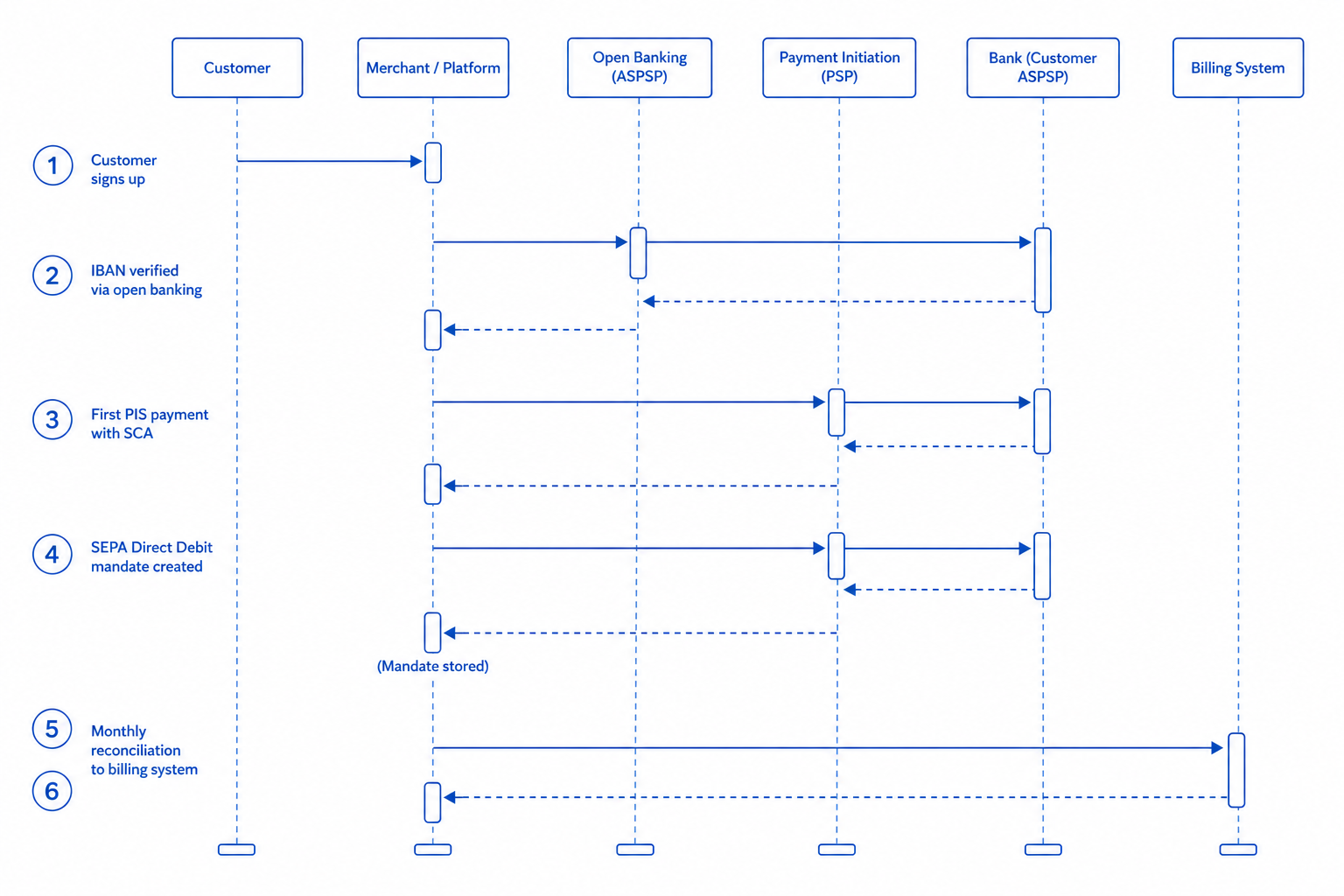

You collect renewals from the customer's bank account instead of hoping their card still works next month. A pattern that works well: first payment via Pay by Bank in the banking app, verify the account, then a SEPA Direct Debit mandate for the recurring amount — the same hybrid many insurers use for annual premiums converted to monthly collection.

Benefits for platform billing teams:

- Lower ongoing cost than card interchange on eligible B2B and B2C tiers

- Fewer expiry-driven failures once the mandate is active

- Clear payment references tied to subscription IDs

Trade-off: first payment still needs bank-app authorisation; mandate setup must meet SEPA scheme rules and your customer's consent UX. Not every provider bundles PIS and mandate management — validate before you commit.

2. Usage-based and variable invoicing

You charge this month's true-up, seat add-on, or overage without a separate manual transfer chase. The customer authorises the exact amount in their banking app for that invoice — useful when the bill changes every period and a stored card is often wrong or over limit.

This fits mid-cycle charges, annual true-ups, and overage lines that would otherwise sit unpaid until someone notices a failed card. Pair variable PIS with recurring SEPA DD for the predictable base subscription where possible.

3. Automated reconciliation

Your billing system matches each payment to the right subscription or invoice without analysts downloading bank CSVs. Payment confirmations and transaction feeds carry references your finance team can trust — which account paid, which failed, which needs dunning.

Done well, finance sees near-real-time cash application — which subscription paid, which failed, which needs dunning. Done poorly, you add another disconnected data source. Idempotent webhooks, stable reference formats, and retry handling belong in the same epic as the Pay by Bank button.

4. Pay by Bank for payment method onboarding

When a new EU customer chooses how to pay, Pay by Bank can replace card capture as the primary onboarding rail — especially for B2B accounts where the payer is the company's finance team, not a product user's wallet.

The customer selects their bank, approves in the app, and you receive a verified account ready for this invoice and future collection. For checkout-style trade-offs between bank and card rails, see pay by bank vs cards at checkout — the UX patterns overlap even though SaaS billing logic sits in your subscription engine, not a cart.

5. Account verification for B2B customers

B2B SaaS still fights wrong-IBAN transfers: the customer types an account on an invoice PDF, finance sends €12,000 to the wrong account, and cash application stalls. Account verification confirms the company name matches the IBAN before you store collection or payout details.

That reduces onboarding fraud, speeds first invoice collection, and gives sales ops confidence when upgrading an account to annual bank-paid terms.

6. Reducing failed payments and involuntary churn

Card-on-file churn from expiry and soft declines is a known SaaS metric. Bank-account-based collection, once a mandate is active, removes expiry — though mandates can still fail for insufficient funds or revocation.

Open banking is not a magic churn cure: you still need dunning, retry logic, and clear customer communications. It is an additional rail to test on segments where cards underperform — often higher-AOV B2B and Northern European markets with strong bank-app adoption.

7. Multi-market EU customer billing

Selling SaaS across Germany, France, and the Nordics means payers use different banks. One provider integration can cover many countries, but coverage is never uniform — map where your customers actually bank before you make Pay by Bank the default.

For connectivity depth (uptime, sandbox, expansion), see open banking for fintech; add billing webhooks and mandate support to that checklist.

8. Finance ops and cash application

Accounts-receivable teams on enterprise tiers often still reconcile open invoices to bank lines manually. Transaction feeds categorise inbound payments and surface who paid; combined with payment confirmations, ops close periods faster and dispute fewer "we already paid" tickets.

This use case matters most as AR volume scales — typically when bank transfer is a deliberate payment option on annual contracts, not only when cards fail.

How to choose which use cases to start with

Most SaaS platforms sequence like this:

- Account verification on B2B onboarding or annual invoice setup.

- Pay by Bank for first payment on a pilot segment with card fallback.

- SEPA Direct Debit for recurring base subscription where mandates are supported.

- Reconciliation automation once payment volume justifies engineering on webhooks and reference schemas.

See also: /blog/open-banking-psd2-explained and /blog/pay-by-bank-vs-cards-for-checkout.

How to evaluate open banking providers for SaaS billing

Prioritise: coverage in your customer countries, reliable one-off and recurring collection, mandate support if you need pull billing, account verification quality, webhooks that your billing system can consume, stable payment references, sandbox that matches production markets, EU data residency, and security certifications. Confirm the provider accepts SaaS billing models in contract — some treat platforms differently from simple checkout merchants.

Provider fit depends on B2B versus B2C mix, usage-based complexity, and how much of your revenue already arrives via manual transfer today.

Frequently Asked Questions

What is open banking for SaaS platforms?

Open banking for SaaS means your platform can collect subscription and variable payments from customer bank accounts, verify those accounts, run recurring collection, and reconcile cash to billing records — usually through one provider integration instead of building bank connections per country.

How is open banking for SaaS different from open banking for fintech?

Fintech open banking usually supports companies whose core product is financial services — wallets, lending, payments apps. SaaS open banking supports software platforms billing for subscriptions and services: the platform needs collection and reconciliation infrastructure, not a banking licence for its end product.

Should we use bank transfer, direct debit, or both for subscriptions?

Many EU SaaS operators take the first payment via Pay by Bank, then set up SEPA Direct Debit on the verified account for renewals. Usage overages stay as one-off bank authorisations per invoice. The right mix depends on failure rates, cost, and what your customers already prefer in each market.

Can open banking replace cards for B2B SaaS entirely?

Rarely in one step. Enterprise buyers often still expect invoice plus transfer or card options. Open banking adds a lower-friction bank rail and better reconciliation for customers who already pay by transfer — measure adoption by tier and country rather than forcing a single method.

How do I evaluate open banking providers for a SaaS billing stack?

Validate country coverage, recurring and variable collection support, mandate capabilities, webhook and reference-field design, billing-system integration effort, SLAs, and sector acceptance in contract. Run a pilot on one plan and one market before rewiring global checkout.

Closing thought

Open banking for SaaS is less about a novel checkout button and more about making bank rails as programmable as cards — recurring collection, variable lines, and books that close without a spreadsheet in the loop. Platforms that win start with verification and one measurable billing segment, prove reconciliation end-to-end, then expand markets. Your pricing model, customer segment, and existing transfer volume decide which of these eight use cases comes first.

Related articles

- Open Banking for Payroll: Disbursement & Verification

Payroll platforms lose trust when salaries land late or on the wrong account. Open banking for payroll providers connects verification and disbursement to regu…

- Open Banking for Online Casinos: EU Deposits & Compliance

Licensed online casino operators lose players when deposits fail at the card gateway and when withdrawals sit in manual review. Open banking casino flows — pay…

- Open Banking for Marketplaces: 8 Use Cases for EU Platforms

Two-sided platforms live on money moving twice: collect from buyers, hold or route platform fees, pay sellers on time. Cards work until interchange, chargeback…