Open Banking for Fintech: 8 Use Cases for EU Product Teams

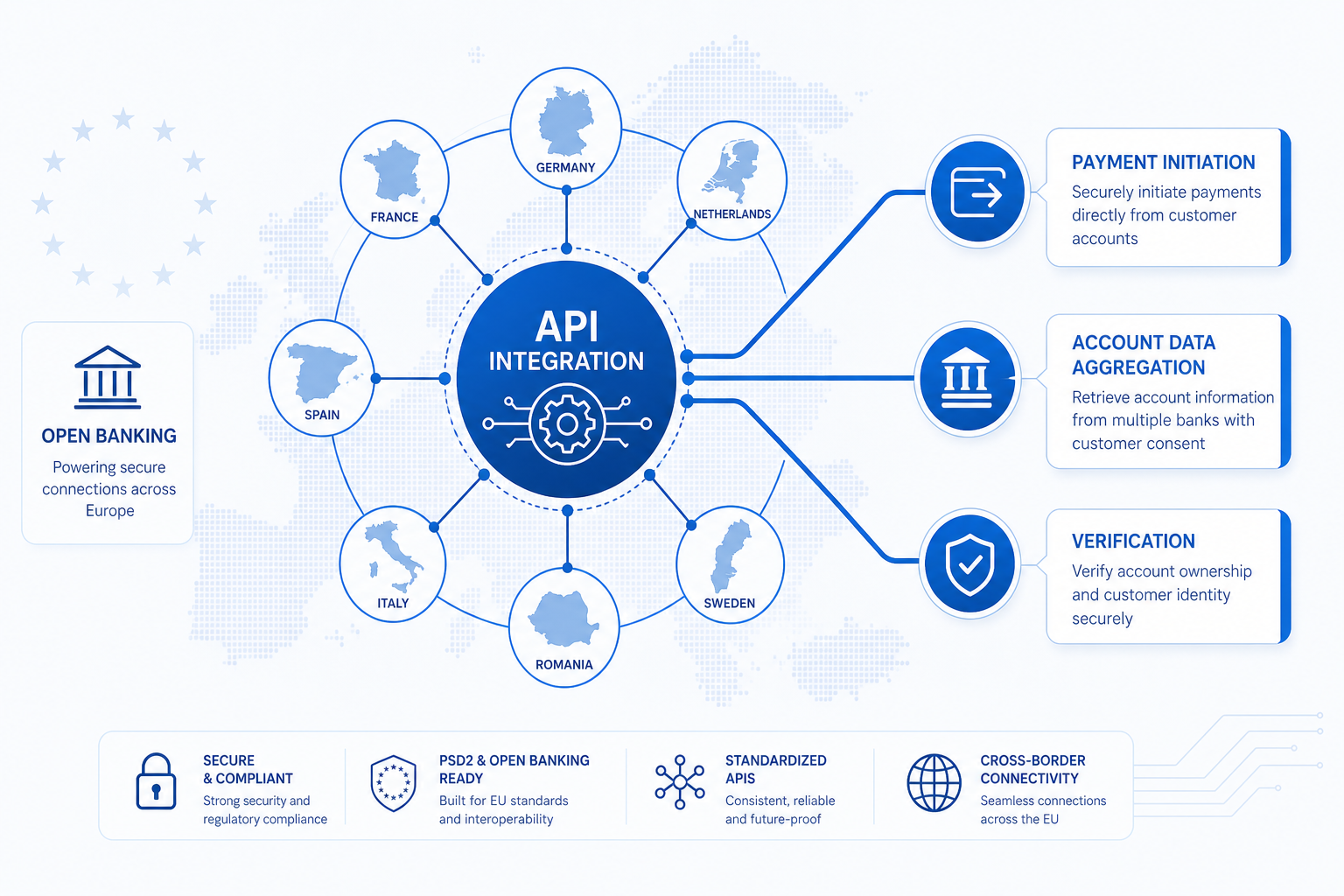

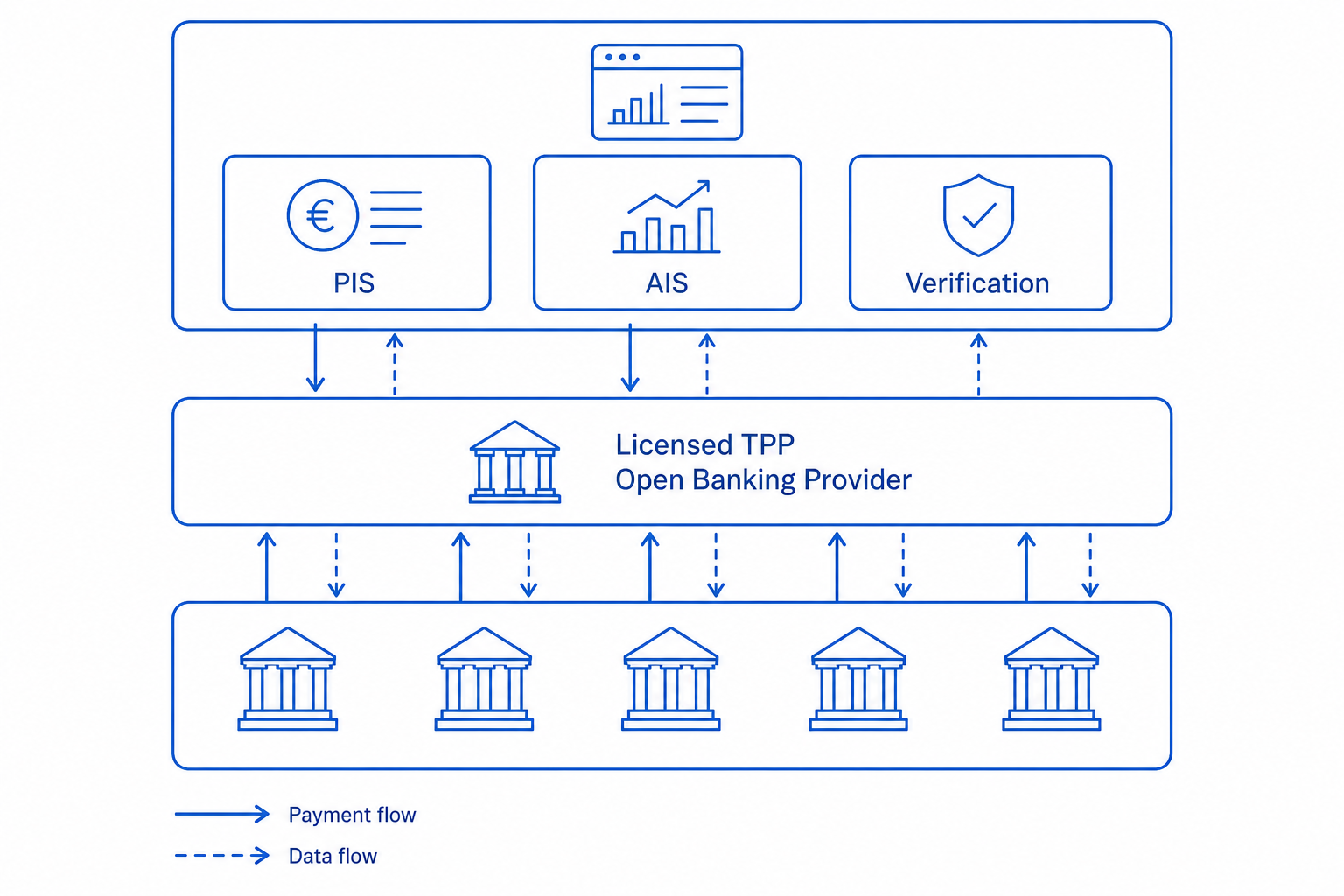

EU fintechs rarely fail because the product idea is wrong — they stall when payments, account data, and verification need to work across ten bank APIs, three regulatory passports, and a roadmap that assumed one country would scale cleanly. Open banking fintech is the regulated shortcut: under PSD2 (Payment Services Directive 2), licensed TPPs (Third Party Providers) connect to ASPSPs (Account Servicing Payment Service Providers) on your behalf so you can offer PIS (Payment Initiation Service) and AIS (Account Information Service) with explicit customer consent. This article maps eight use cases product and engineering teams ship today — from single-integration multi-market coverage to build-versus-partner licensing — plus how to sequence them without rebuilding your stack per country.

Open banking for fintech: The use of regulated PSD2 APIs — PIS for moving money, AIS for reading account data, and verification services for onboarding — by fintech companies to power payments, data products, and compliance workflows across EU markets, typically through one regulated provider integration rather than direct bank-by-bank builds.

Why open banking matters for fintech specifically

Fintech roadmaps compress three hard problems: getting customers to move money, getting permission to read their financial data, and proving who owns the account — often in multiple EU countries at once. Building direct integrations with every target bank burns engineering capacity and still leaves you maintaining SCA (Strong Customer Authentication) flows per ASPSP.

According to the European Banking Authority, PSD2 established the framework for third-party access to payment accounts; most growth-stage fintechs consume that framework through a licensed aggregator rather than applying for their own AISP/PISP authorisation on day one.

Patterns to keep in mind:

- Full-stack usually means PIS plus AIS plus verification on one contract — not three unrelated vendors.

- Coverage is geographic, not abstract: Germany-strong is not France-strong.

- Regulated activities stay with the licensed party in the chain; your product layer handles UX and business logic.

1. Multi-market EU connectivity from one integration

The first open banking fintech use case is operational: one API contract, one sandbox, one production certification path that reaches banks in the countries on your expansion map. Without that, every new market becomes a bespoke integration project — redirect URLs, error codes, and consent flows differ by ASPSP.

What to validate before you sign:

- Bank count and quality per country — not just a headline EU number

- Uptime and incident transparency — production SLAs, not marketing claims

- Fallback behaviour when a bank API is down — retry, reroute, or graceful degrade

- UK and EU treated separately if you operate in both post-Brexit

This use case is the foundation for everything else on the list. Payments-only or data-only providers can work early, but multi-product fintechs usually converge on a partner that covers both PIS and AIS in the same markets you plan to sell into.

2. Payment initiation inside your product

PIS lets your users pay in, pay out, or top up via account-to-account rails — Pay by Bank at checkout, wallet funding, invoice collection, or disbursement to end users. For fintechs, payment initiation is often the revenue rail: lower variable cost than cards on eligible flows, immediate confirmation when the bank returns success, and reconciliation metadata (IBAN, reference) attached to the transaction.

Trade-offs are product-shaped, not only technical: redirect flows need mobile-first UX, clear bank selection, and card or wallet fallback where conversion data says you need it. For checkout-specific economics and dispute profiles, see pay by bank vs cards at checkout — the comparison is retail-framed but the rail mechanics apply to consumer-facing fintech apps too.

3. Account aggregation and data products

AIS powers personal finance managers, business dashboards, affordability views, and categorised transaction feeds. The customer consents once (with SCA), and your app reads balances and history within PSD2 limits — including the standard 180-day re-consent cycle for ongoing access.

For fintech data products, the engineering work is as much enrichment and UX as connectivity: categorisation quality, handling joint accounts, multi-currency display, and clear consent renewal before access silently expires. Regulators expect transparent purpose limitation — you read accounts for the use case the customer agreed to, not an open-ended data grab.

4. Account verification and KYC at onboarding

Before you move money to or from a new user, you need confidence the account is theirs. AIS-backed verification returns account holder name and IBAN match in an authenticated step — faster than manual statement upload and harder to spoof than typed bank details.

This use case cuts onboarding fraud, wrong-IBAN payouts, and compliance review backlog. It pairs naturally with payment initiation: verify on signup, initiate payments against the same verified account later. Vertical-specific depth exists elsewhere — open banking for e-commerce covers merchant and marketplace onboarding — but the verification primitive is the same.

5. Lending and affordability decisioning

Consumer and SME lenders use AIS to confirm income patterns, recurring obligations, and balance volatility instead of relying on self-declared figures alone. The underwriter gets structured, source-verified signals: salary regularity, gig-economy volatility, existing loan repayments visible as outgoings.

Open banking does not replace credit policy or regulatory affordability rules — it feeds them with better evidence and a defensible audit trail. Teams should align data retention, consent scope, and model governance with legal before launching automated decisions on AIS data.

6. Outbound payouts and treasury operations

Neobanks, marketplaces, and payout-heavy fintechs use PIS (and SEPA Credit Transfer / SEPA Instant where supported) to send funds to user IBANs — withdrawals, seller settlements, affiliate payments. Instant payout capability depends on receiving-bank participation; your provider should document country-level Instant coverage honestly.

Treasury teams care about cut-offs, failed-payment handling, and whether inbound customer funds and outbound disbursements reconcile in one reporting surface. Webhook reliability matters as much as raw API latency — ops runs on events, not happy-path demos.

7. Build vs partner: your own TPP licence or a regulated provider

Not every fintech needs to become a licensed AISP or PISP. Holding authorisation brings capital requirements, ongoing regulatory reporting, direct ASPSP maintenance, and operational responsibility for consent and incident management. Partnering routes regulated activity through a provider that already holds passports in your target markets — you integrate APIs and own the product experience.

| Factor | Partner with licensed provider | Apply for own AISP/PISP |

|---|---|---|

| Time to market | Months via API integration | Often 12–24+ months to authorisation |

| Engineering focus | Product and orchestration | Regulatory ops plus bank connectivity |

| Control | Contractual SLAs and roadmap dependency | Direct ASPSP relationships |

| Fit | Most seed to Series B fintechs | Scale players with payments as core licence |

Many teams start partnered, then reassess licensing when payment or data activity becomes the regulated core of the business — not because open banking requires it on day one.

8. Reconciliation and operational reporting

AIS feeds plus PIS webhooks give finance and ops a near-real-time ledger: which user payment cleared, which payout failed, which consent expired. That shortens month-end matching between your internal transaction table and bank statements — especially when you run multiple rails (cards plus open banking plus SEPA files).

This use case rarely wins a board deck on its own, but it determines whether payments scale without hiring another reconciliation analyst per country.

How to choose which use cases to start with

Most fintechs sequence deliberately:

- Lock multi-market coverage for your first two or three countries on one provider shortlist.

- Ship the revenue rail — usually PIS for pay-in or pay-out — with measurable conversion and failure logging.

- Add verification before high-risk outbound money movement.

- Layer AIS for data products or underwriting once consent UX and legal sign-off are ready.

See also: /blog/open-banking-psd2-explained and /blog/pay-by-bank-vs-cards-for-checkout.

How to evaluate open banking providers for fintech use cases

Prioritise: PSD2 licensing in every market you operate in, combined PIS and AIS if you need full-stack, documented bank coverage per country, sandbox parity with production, webhook and idempotency design, SEPA Instant support where payouts matter, account verification quality, EU data residency, and ISO 27001 / SOC 2 evidence. API ergonomics (SDKs, error models, versioning policy) determine engineering velocity as much as bank count.

Provider fit is geography- and product-specific — a lending-focused AIS strength does not automatically mean strong Pay by Bank conversion in your target retail segment.

Frequently Asked Questions

What is open banking for fintech companies?

Open banking for fintech is the use of regulated PSD2 APIs to initiate payments (PIS), access account information (AIS), and verify bank accounts with customer consent — typically via integration with a licensed TPP rather than building direct connections to every bank. It enables multi-market EU products without maintaining a separate bank integration per country.

Do fintechs need their own TPP licence to use open banking?

No. Most fintechs partner with a licensed AISP and/or PISP that holds authorisation in the markets they serve. Applying for your own licence is an option at scale when regulated payment or data activity is core to the business model, but it is not a prerequisite to ship PSD2-based features.

What is the difference between AIS and PIS for fintech products?

PIS moves money — collections, top-ups, payouts, and refunds initiated from a user's bank account. AIS reads data — balances, transactions, and account holder details for aggregation, underwriting, and verification. Full-stack fintech products often use both: AIS to understand the customer, PIS to move funds.

How does open banking help fintechs expand across EU markets?

A single regulated provider integration can reach multiple ASPSPs across countries, replacing bespoke bank projects per market. Coverage still varies by country and bank — expansion planning should map target markets to actual connectivity, not assume uniform EU-wide behaviour.

Can open banking replace card processing in a fintech app?

For eligible flows, yes — Pay by Bank and account-to-account payments can reduce interchange and change dispute dynamics. Most consumer fintechs keep cards or wallets as fallback while they measure open banking conversion by segment. The right mix is empirical, not ideological.

How do I evaluate open banking providers for a fintech roadmap?

Match provider strengths to your use case stack: PIS-only, AIS-only, or combined; country coverage; Instant payout support; verification and categorisation quality; regulatory passports; SLAs; and engineering fit (API design, webhooks, sandbox). Align commercial terms with projected payment and data volumes before you hard-code a single vendor.

Closing thought

Open banking for fintech is infrastructure that lets product teams focus on the customer problem — lending, payments, wealth, embedded finance — instead of rebuilding bank connectivity every time you enter a new EU market. The teams that move fastest treat provider choice as a product decision tied to geography and use-case stack, start with one measurable rail, and expand into data and verification once consent and ops patterns are proven. Your markets, licence strategy, and roadmap determine which of these eight use cases comes first.

Related articles

- Open Banking for Payroll: Disbursement & Verification

Payroll platforms lose trust when salaries land late or on the wrong account. Open banking for payroll providers connects verification and disbursement to regu…

- Open Banking for Online Casinos: EU Deposits & Compliance

Licensed online casino operators lose players when deposits fail at the card gateway and when withdrawals sit in manual review. Open banking casino flows — pay…

- Open Banking for Marketplaces: 8 Use Cases for EU Platforms

Two-sided platforms live on money moving twice: collect from buyers, hold or route platform fees, pay sellers on time. Cards work until interchange, chargeback…