Open Banking for E-commerce: 8 EU Checkout Use Cases

European e-commerce and marketplace operators move billions through card rails every year — checkout, seller payouts, refunds, and cross-border baskets — yet much of that stack still carries interchange, chargeback exposure, and settlement delays that account-to-account payments were built to avoid. Open banking e-commerce is no longer a pilot category: under PSD2 (Payment Services Directive 2), licensed TPPs (Third Party Providers) can initiate payments and read account data with explicit customer consent, and retailers from fashion to marketplaces are shipping Pay by Bank and payout flows in production across the EU. This article maps eight use cases checkout and payments teams are deploying today, the trade-offs against cards, and how to sequence an integration without boiling the ocean.

Open banking for e-commerce: The use of regulated PSD2 APIs — covering PIS (Payment Initiation Service) and AIS (Account Information Service) — by online retailers, marketplaces, and payment orchestrators to collect at checkout, disburse to sellers, verify accounts, and reconcile orders, with explicit customer consent under PSD2.

Why open banking matters for e-commerce specifically

E-commerce unit economics are dominated by payment cost, conversion at checkout, and how fast settled funds hit your account. Card schemes bundle dispute workflows many teams already know; they also charge interchange that scales with GMV. Open banking payment initiation is typically priced per successful transaction without interchange, and authorised account-to-account payments do not carry card-style chargeback rights once the customer completes SCA (Strong Customer Authentication) in their banking app.

According to the European Payments Council, SEPA Instant Credit Transfer can settle in seconds where both banks participate — a meaningful difference versus card acquirer settlement cycles for cash-flow-sensitive merchants.

Patterns to keep in mind as you read the use cases below:

- PIS moves money; AIS reads data. Most e-commerce roadmaps need one or both.

- SCA applies on every initiated payment and on fresh account data consent, with the standard 180-day re-consent window for ongoing AIS.

- You do not need your own TPP licence. Most merchants integrate through a regulated open banking provider that holds AISP/PISP authorisation in your markets.

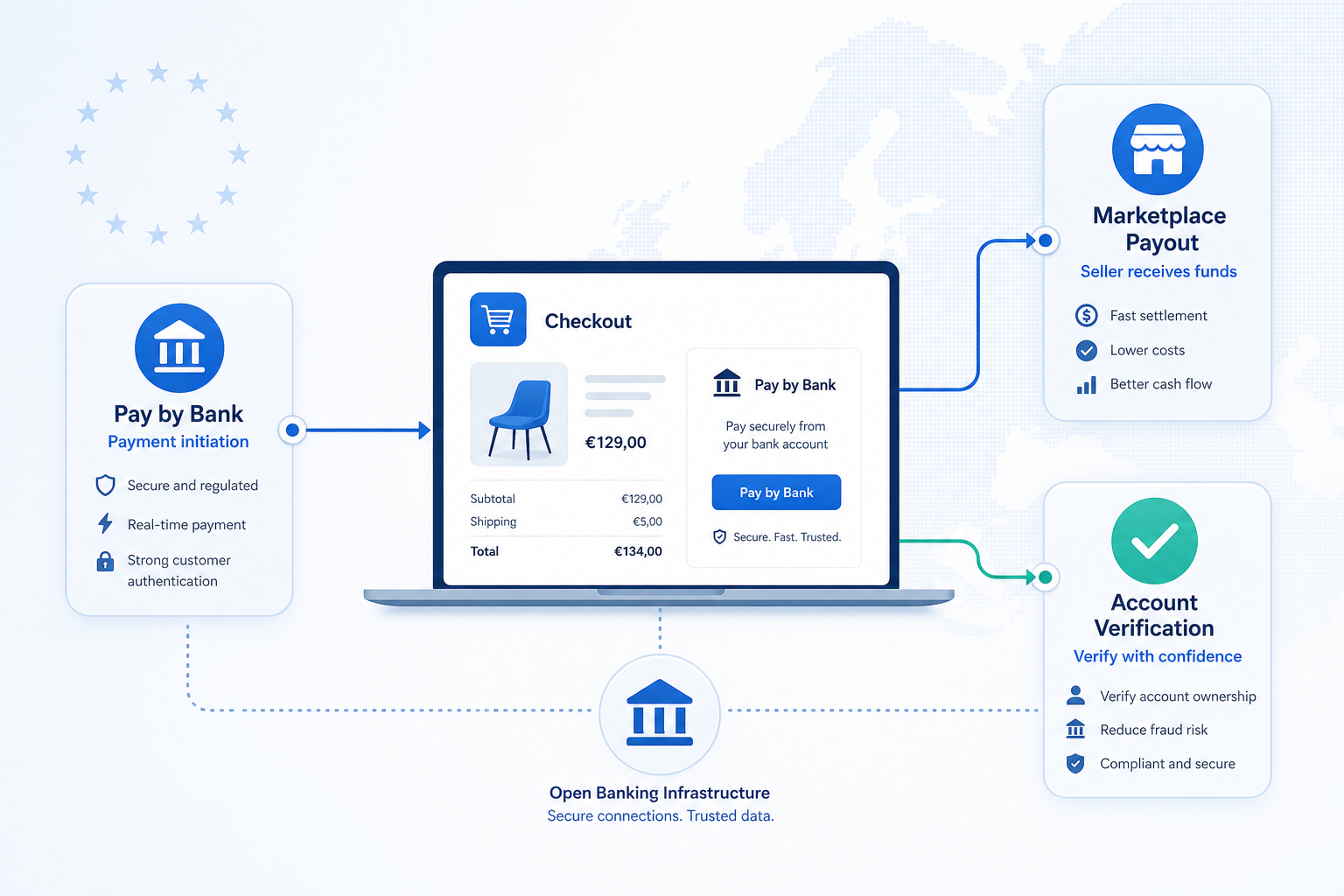

1. Pay by Bank at checkout

The highest-visibility open banking e-commerce use case is replacing or supplementing cards at checkout with Pay by Bank — the customer selects their bank, authenticates in the mobile banking app, and authorises an account-to-account payment initiated by your PIS provider.

The benefit pattern is consistent across D2C, subscription-first brands, and high-AOV retail:

- Lower cost per successful payment versus card interchange, especially on baskets above typical card fee floors

- Immediate payment confirmation when the bank returns success — useful for order fulfilment triggers

- Reduced chargeback exposure on authorised push payments versus card disputes

- Deterministic reconciliation — IBAN and payment reference returned with the transaction

The trade-off is conversion: bank redirect flows depend on device, bank UX, and customer trust. Mobile checkout usually outperforms desktop; fallback to card or wallet remains essential. For a structured comparison of fees, chargebacks, settlement, and UX, see pay by bank vs cards at checkout.

2. Instant settlement and cash-flow timing

Where your acquirer settles card funds on T+1 or longer, SEPA Instant can put inbound checkout funds in your merchant account in seconds — subject to your bank, your provider, and cut-off rules. For inventory-heavy retailers and flash-sale operators, that shifts working-capital assumptions without changing what the customer sees at checkout.

Instant settlement is not universal: bank participation varies by country, and some providers route standard SEPA Credit Transfer when Instant is unavailable. Model both paths in your treasury forecast rather than assuming every payment clears in real time.

3. Chargeback and dispute profile

Card chargebacks are a material cost line for e-commerce — friendly fraud, delivery disputes, and scheme rules all flow through acquirer chargeback queues. Open banking payment initiation is a customer-authorised push from their account; once authorised under PSD2, there is no equivalent card chargeback right. Disputes still happen — unclear refund policies, unauthorised use of an account — but the operational pattern is different and often routes through bank complaint processes rather than scheme chargeback reason codes.

This is not "zero risk": consent clarity, order descriptors, and refund SLAs matter as much as on cards. Teams that win here treat Pay by Bank as a product surface with explicit copy, not a hidden rail.

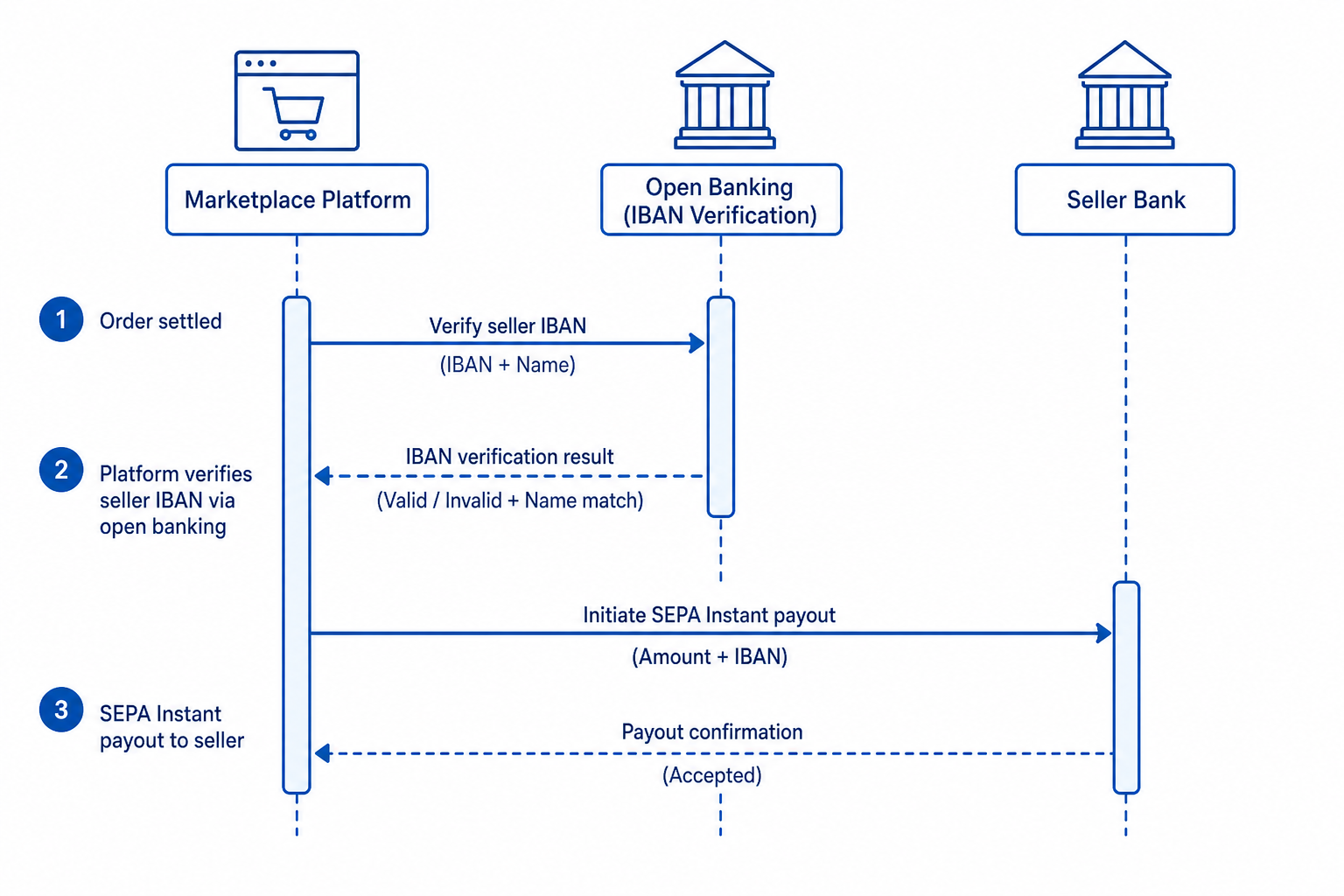

4. Marketplace and seller payouts

Marketplaces sit on two-sided money movement: collect from buyers, disburse to sellers after fees. Open banking PIS supports outbound payouts to verified seller IBANs — often combined with AIS to confirm account holder name before the first disbursement. That reduces misdirected payouts and fraud where sellers supply incorrect bank details.

Split-payment models vary by provider: some orchestrate platform-collect-then-disburse; others integrate with escrow or e-money partners. The integration choice matters as much as the use case — seller KYC, holding periods, and regulatory status of the marketplace entity all constrain architecture.

5. Refunds and returns

Refund volume scales with GMV. Card refunds reverse through acquirer paths with scheme timing and partial-refund quirks. Payment initiation to a pre-verified customer IBAN can be faster to execute operationally once the account was confirmed at checkout — fewer wrong-IBAN failures than manual SEPA entry in a contact centre.

High-return categories (fashion, home goods) should still measure cost per refund rail and customer communication: a bank-account refund feels different from "refund to card" and support scripts need to match.

6. Cross-border EU checkout

Selling across EU markets means multiple ASPSPs (Account Servicing Payment Service Providers) and local bank UX. Open banking coverage is not uniform — a provider strong in Germany may be weaker in Southern or Eastern EU markets. Checkout teams should map target countries to bank connectivity and fallback rails before committing to Pay by Bank as the primary method.

For UK–EU operations, treat UK open banking and EU PSD2 as separate regulatory and technical stacks; do not assume one integration behaves identically in both.

7. Account verification and fraud at onboarding

Before first payout to a seller or high-risk checkout, you need confidence the bank account belongs to the right party. AIS-backed account verification returns holder name and IBAN match in an SCA-authenticated step — the same pattern insurers use for policyholder accounts, applied here to merchant onboarding and marketplace seller KYC.

This reduces application fraud, wrong-IBAN disbursements, and manual review queues. It also unlocks cleaner recurring flows when you store a verified mandate reference rather than re-asking for bank details.

| Signal | Manual onboarding | Open banking verification |

|---|---|---|

| Account ownership | IBAN typed by user | API-confirmed name match |

| Payout risk | Post-hoc bounce handling | Pre-disbursement check |

| Fraud pattern | Synthetic IBANs | Bank-authenticated identity |

8. Reconciliation and finance operations

AIS transaction feeds give finance teams categorised inbound and outbound movements tied to order references — useful when card settlements batch across schemes and descriptors. Combined with PIS confirmation webhooks, ops can match order ID to bank movement without waiting for acquirer reports.

The win compounds for marketplaces reconciling platform fees, seller liabilities, and VAT lines across entities. AIS does not replace your ERP; it shortens the gap between bank statement and order ledger.

How to choose which use cases to start with

Most retailers do not deploy all eight at once. Sequencing that tends to work:

- Start with Pay by Bank on a defined basket — one country, one device segment, measurable conversion versus card — with card fallback live.

- Add account verification before marketplace payouts or high-value outbound flows.

- Layer instant settlement once treasury and provider SLAs are understood.

- Expand AIS reconciliation and cross-border coverage after the core checkout path is stable.

Provider fit depends on markets, transaction volume, and whether you need PIS only or PIS plus AIS on one contract. See also: /blog/open-banking-psd2-explained and /blog/pay-by-bank-vs-cards-for-checkout.

How to evaluate open banking providers for e-commerce

Look for: PSD2 licensing (AISP and PISP) in every country you sell into, bank API coverage and published uptime, Pay by Bank conversion tooling (redirect, deep link, QR where relevant), SEPA Instant support on inbound and outbound, account verification with name match, webhook reliability for order fulfilment, and contractual SLAs. EU data residency, PCI scope boundaries (you should not handle credentials), and ISO 27001 / SOC 2 evidence belong on any enterprise vendor review.

No single provider wins every market — matching depends on your GMV, AOV distribution, and which use cases you prioritise first.

Frequently Asked Questions

What is open banking for e-commerce?

Open banking for e-commerce is the use of regulated PSD2 APIs by online retailers and marketplaces to initiate customer payments at checkout, disburse funds to sellers, verify bank accounts, and access transaction data for reconciliation — all with explicit customer consent. Merchants typically integrate through a licensed open banking provider rather than holding a TPP licence themselves.

Is open banking legal for online retailers in the EU?

Yes. PSD2 has applied across the EU since 2018 and permits regulated third parties — and merchants using them — to initiate payments and access account information with customer consent. Selling goods online does not require you to become a payment institution if you partner with a licensed AISP or PISP for the regulated activities.

What is the difference between AIS and PIS for e-commerce?

PIS (Payment Initiation Service) moves money — checkout collection, refunds, and seller payouts. AIS (Account Information Service) reads account data — balances, transactions, and verified account holder names — for onboarding, fraud checks, and reconciliation. Many e-commerce programmes combine both: verify via AIS, collect via PIS.

How does Pay by Bank conversion compare to cards at checkout?

Pay by Bank conversion depends on market, device, bank UX, and basket value. Cards remain familiar globally; Pay by Bank can reduce cost and chargeback exposure where customers trust bank-app authorisation. Most merchants run both with data-driven routing rather than forcing a single rail. Deeper trade-offs are covered in pay by bank vs cards at checkout.

Can open banking eliminate chargebacks for merchants?

Open banking push payments authorised by the customer do not follow card chargeback schemes, which changes dispute handling and cost profile. That is not the same as zero customer complaints — refunds, fraud, and bank complaints still require clear policies and ops playbooks.

How do I evaluate open banking providers for e-commerce use cases?

Prioritise country coverage where you sell, PIS and AIS capability on one integration if you need both, SEPA Instant support, account verification quality, webhook and reconciliation tooling, and SLAs on bank API availability. Align technical due diligence with your checkout stack (Shopify, custom, marketplace platform) and settlement currency needs.

Closing thought

Open banking is not one checkout button — it is a set of regulated building blocks for collection, disbursement, verification, and reporting. The retailers getting value tend to start with a narrow Pay by Bank experiment, measure conversion and unit economics honestly, and expand into payouts and ops use cases once the pattern works. Every catalogue and market mix is different; provider matching should follow your volumes, countries, and which of these eight use cases you need first.

Related articles

- Open Banking for Payroll: Disbursement & Verification

Payroll platforms lose trust when salaries land late or on the wrong account. Open banking for payroll providers connects verification and disbursement to regu…

- Open Banking for Online Casinos: EU Deposits & Compliance

Licensed online casino operators lose players when deposits fail at the card gateway and when withdrawals sit in manual review. Open banking casino flows — pay…

- Open Banking for Marketplaces: 8 Use Cases for EU Platforms

Two-sided platforms live on money moving twice: collect from buyers, hold or route platform fees, pay sellers on time. Cards work until interchange, chargeback…