Open Banking for Payroll: Disbursement & Verification

Payroll platforms lose trust when salaries land late or on the wrong account. Open banking for payroll providers connects verification and disbursement to regulated bank rails — so you confirm employer and employee accounts before payday and initiate payouts with fewer manual checks. This guide maps open banking payroll use cases, when to use account data vs payment initiation, implementation steps, and what to ask vendors — without a regulatory lecture.

Open banking payroll: Using licensed third-party APIs to verify payment accounts and initiate salary or contractor disbursements from employer or platform accounts, with customer consent — reducing wrong-IBAN payouts and manual bank-file work.

What payroll use cases fit open banking?

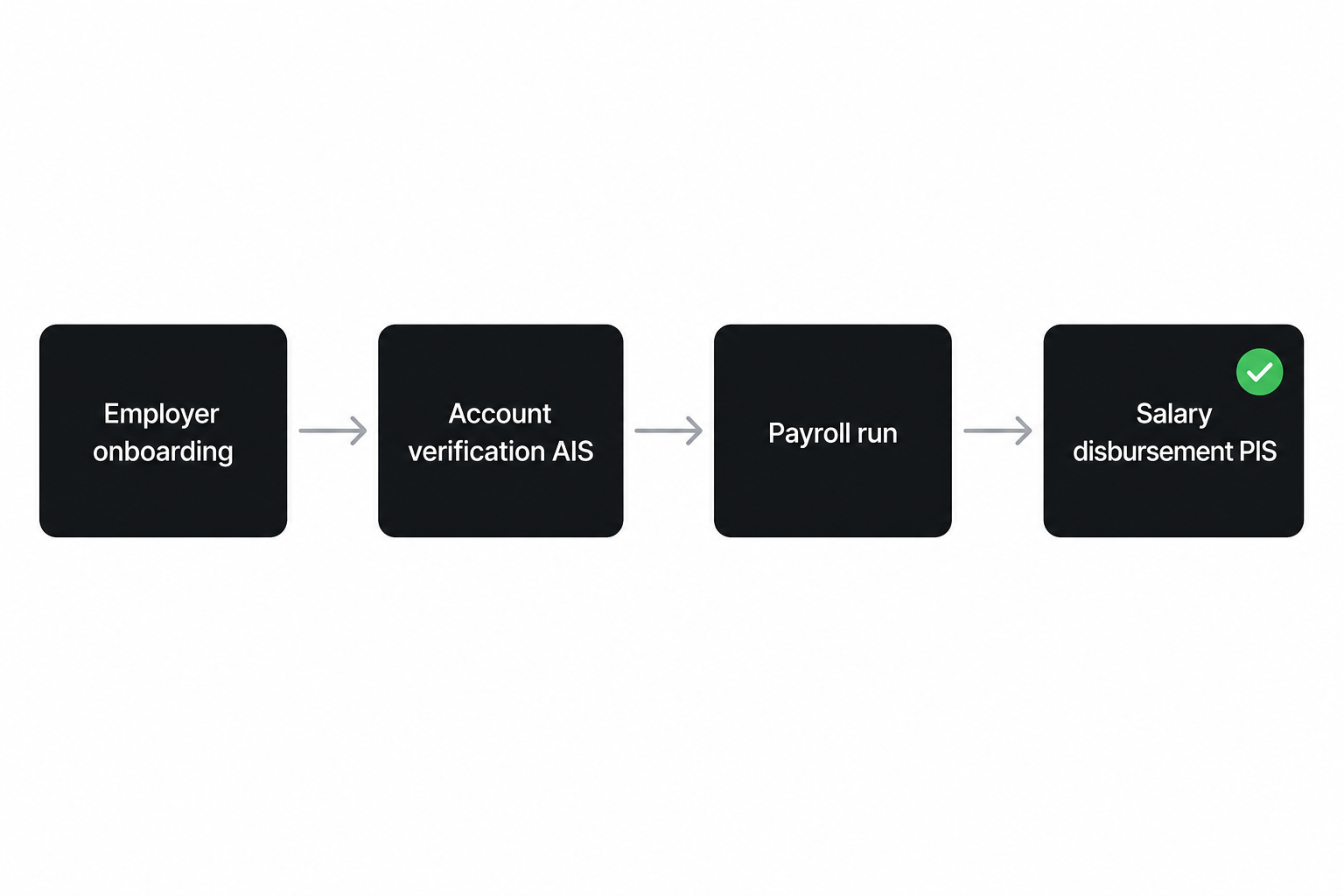

Payroll open banking api projects usually start with two jobs:

- Disbursement — pay employees and contractors from employer or platform balances via payment initiation or file replacement

- Verification — confirm account ownership and details before first run or when bank details change

Secondary flows include employer onboarding (verify the funding account), collections for payroll-funded products, and reconciliation (match bank confirmations to payroll lines).

Outcomes payroll buyers measure:

- Fewer failed payouts and support tickets on wrong IBAN

- Faster onboarding of new employers without micro-deposit delays

- Less manual ops exporting bank files and chasing status

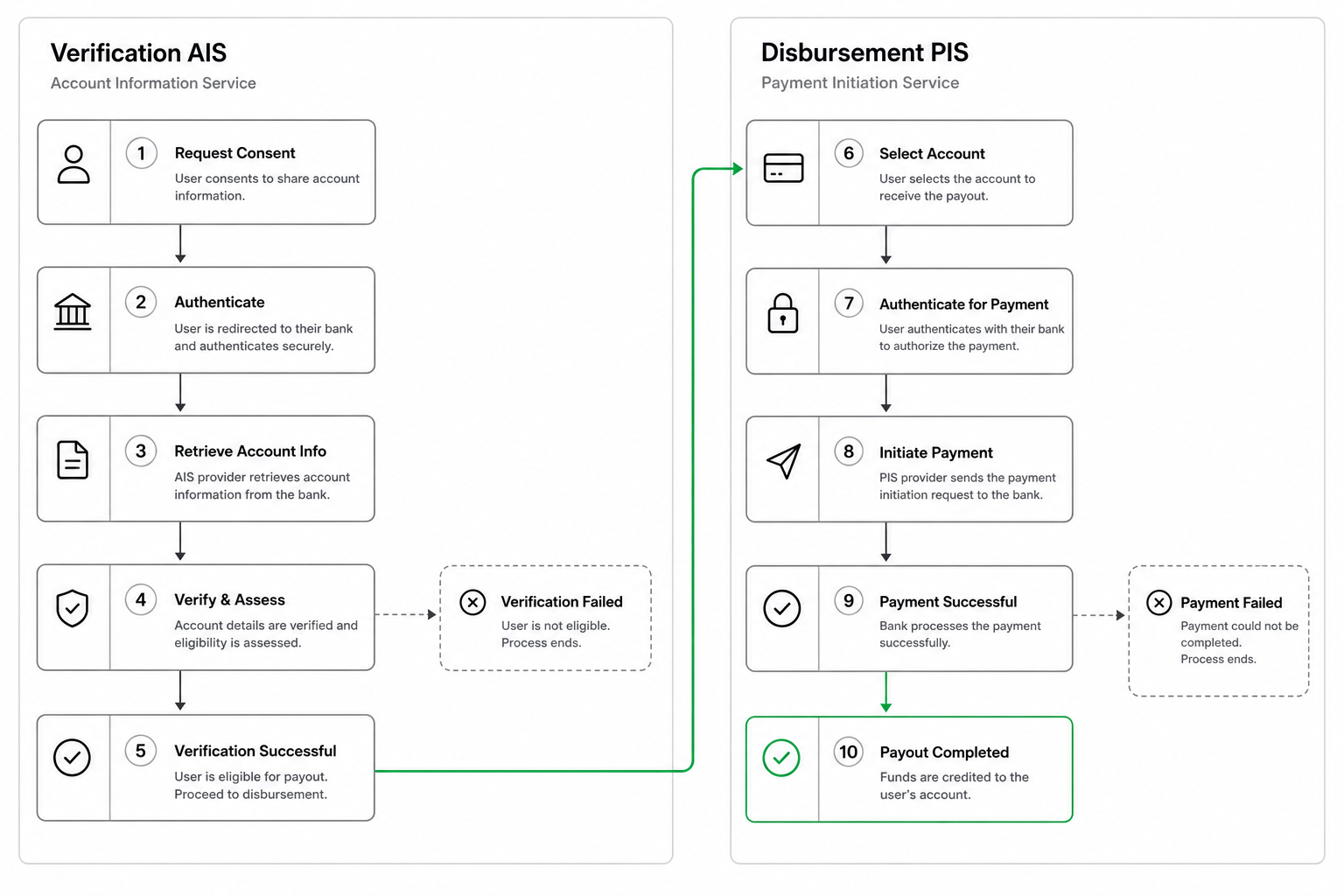

AIS vs PIS for payroll — which rail when?

Open banking payroll stacks often need both rails; they solve different problems.

| Need | Rail | Outcome |

|---|---|---|

| Verify employee or employer account | Account information (AIS) | Match name and IBAN before payday |

| Send salary or contractor payment | Payment initiation (PIS) | Move money with bank confirmation |

| Reconcile status | Webhooks + identifiers | Finance closes the run without CSV chasing |

AIS does not move money. PIS does not replace your payroll calculation — it executes authorised payments. For a plain-language split, see AIS vs PIS in open banking.

How do you implement open banking in payroll providers?

How to automate open banking in payroll providers follows a practical sequence:

- Define flows — employer funding verification, employee payout, contractor payout, retries

- Map banks — countries and institutions your employers and payees use

- Choose provider — coverage on that list, webhooks, B2B account support

- Integrate — consent UX, idempotent payment creation, status webhooks to payroll runs

- Pilot — one country, one employer segment, measure failure rate and ops time

- Scale — expand banks before you expand geography

Build consent into employer and employee journeys — payroll users expect clarity on who accesses their account and why.

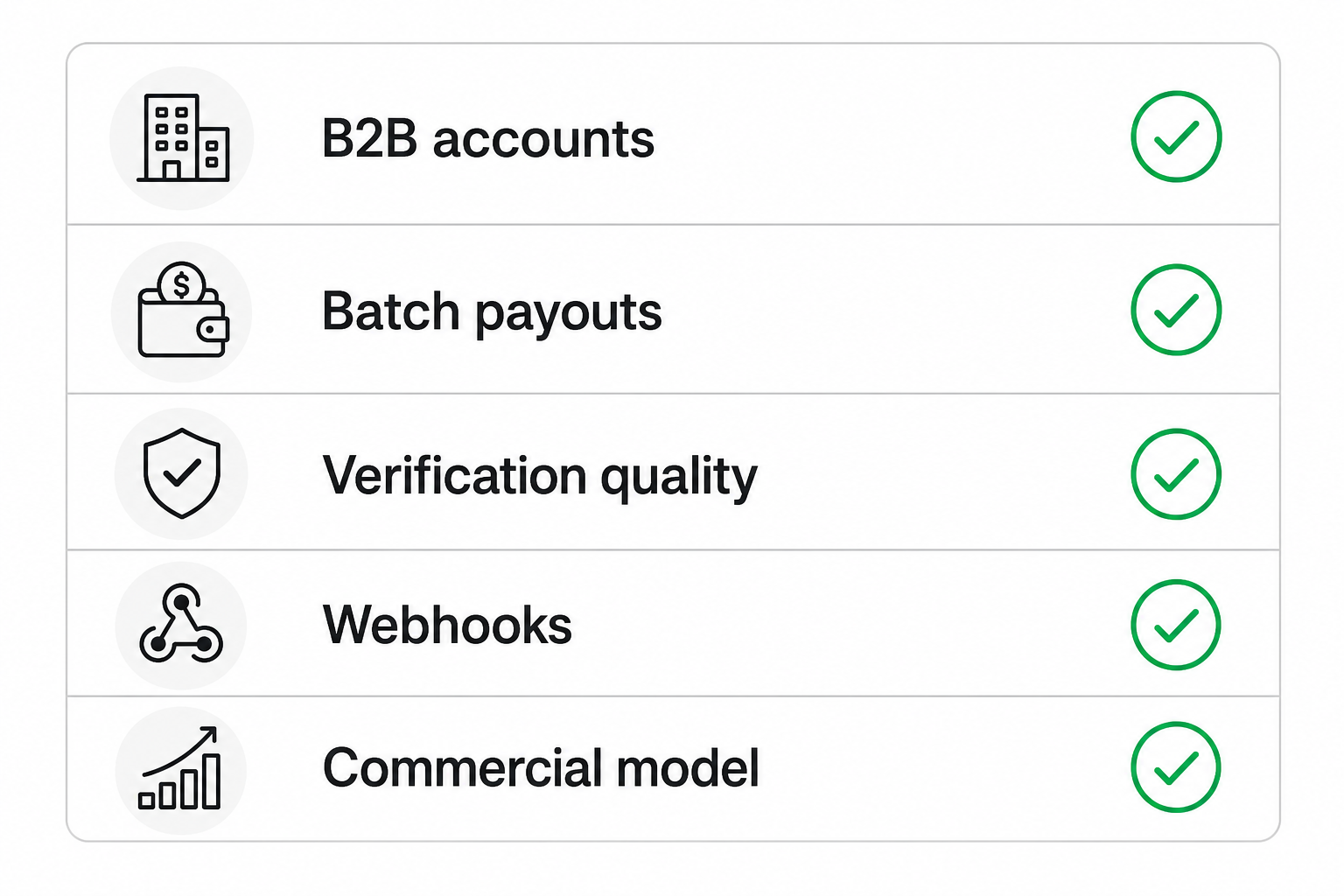

What provider criteria matter for payroll?

Salary disbursement open banking fails in production on details, not slides:

- B2B and business accounts — retail-only coverage misses employer funding accounts

- Bulk and batch behaviour — cut-off times, file vs API initiation, idempotency on retries

- Verification quality — name-IBAN match per bank; see instant account verification

- Webhooks — final status for each payment line tied to payroll run IDs

- Commercial model — per successful payout vs per verification; minimums

Compare vendors with open banking provider comparison and shortlist using how to shortlist open banking providers.

Frequently Asked Questions

What is open banking for payroll providers?

It is using regulated APIs to verify accounts and initiate salary or contractor payments from payroll software, with consent, instead of relying only on manual bank files.

Can open banking replace payroll calculation engines?

No. Open banking executes and verifies payments; gross-to-net, tax, and compliance logic stay in your payroll core.

Is open banking payroll the same as salary disbursement open banking?

Salary disbursement open banking focuses on the payout rail. Full open banking payroll often includes verification, employer funding checks, and reconciliation.

How do you automate open banking in payroll providers at scale?

Standardise webhooks into payroll run state, idempotent payment APIs, and bank-level monitoring. Automate retries only where your provider documents safe behaviour.

What is a payroll open banking API?

The REST (and webhook) surface your engineering team integrates — typically from a licensed TPP that connects to many banks, not from each bank directly.

How do I choose a provider for EU payroll payouts?

List employer and payee banks by country, test business-account initiation and verification in sandbox, then score webhooks and support. Use the provider directory when your criteria are fixed.

Conclusion

Open banking for payroll providers wins on fewer failed payouts and faster verification — not on regulatory vocabulary. Split AIS and PIS by job, test B2B bank coverage on mobile and desktop, and pilot one market before you promise EU-wide salary disbursement open banking. When your bank list is defined, match providers through structured comparison and the provider directory.

Related articles

- Open Banking for Accounting: 6 Use Cases for Finance Teams

Small businesses and their accountants lose hours every month to the same friction: customers pay invoices by card and eat margin on fees, or they pay by manua…

- Open Banking Utility Payments: How Suppliers Collect Bills

Utility billing teams lose margin on three predictable leaks: card interchange on high-volume inbound payments, failed direct debits that trigger dunning and c…

- Open Banking for Online Casinos: EU Deposits & Compliance

Licensed online casino operators lose players when deposits fail at the card gateway and when withdrawals sit in manual review. Open banking casino flows — pay…