Best Open Banking APIs for Account Verification (2026)

Wrong-IBAN payouts and slow onboarding checks cost more than a bad API choice — they cost support tickets, compliance rework, and customers who abandon before their first transfer. The best open banking APIs for account verification in 2026 are the ones that return a reliable name-and-account match in seconds for the banks your users actually use, with webhooks and fields your product can act on — not the provider with the longest feature list on a landing page. This guide covers what “instant” means in practice, how UK and EU checks differ, and what to validate in sandbox before you commit engineering time.

Instant account verification (open banking API): Confirming that a bank account exists and belongs to the person or business you expect — usually within seconds of the customer approving access in their banking app — via a licensed provider’s API instead of manual statement uploads or multi-day micro-deposit tests.

What “instant” means — and what it does not

Instant verification means your onboarding or payout flow can continue in the same session: the user selects their bank, authenticates, and your backend receives a structured result (match, no match, partial, or unavailable) before they leave the screen. It does not mean every bank returns the same fields at the same speed — coverage and response quality vary by institution and country.

Providers market “real-time” checks, but your acceptance criteria should be concrete:

- Latency — p95 under a few seconds after consent, for your top five banks per market

- Match semantics — exact name match, fuzzy match, or “account found but name unavailable”

- Persistence — whether you store a verification token for later payouts or must re-check

- Failure clarity — distinct errors for user cancel, bank timeout, and unsupported institution

If verification blocks a payment or seller payout, treat latency and match-rate SLAs as product requirements, not nice-to-have API metrics.

Verification-only API vs a full open banking stack

Some teams only need instant account verification — IBAN and name match at onboarding or before first payout — without shipping Pay by Bank checkout or ongoing AIS aggregation. A verification-led API (often AIS with a narrow consent scope) can go live faster and with a smaller integration surface than a full PIS + AIS platform.

Choose a full stack when the same provider must also handle payments, recurring collection, or multi-product roadmaps in one contract. The best open banking API providers for developers (2026) guide covers sandbox, coverage maps, and PIS/AIS depth for that wider evaluation. If verification is your only near-term need, still validate holder-name quality on your top banks before you sign — coverage labels on a website do not replace sandbox tests.

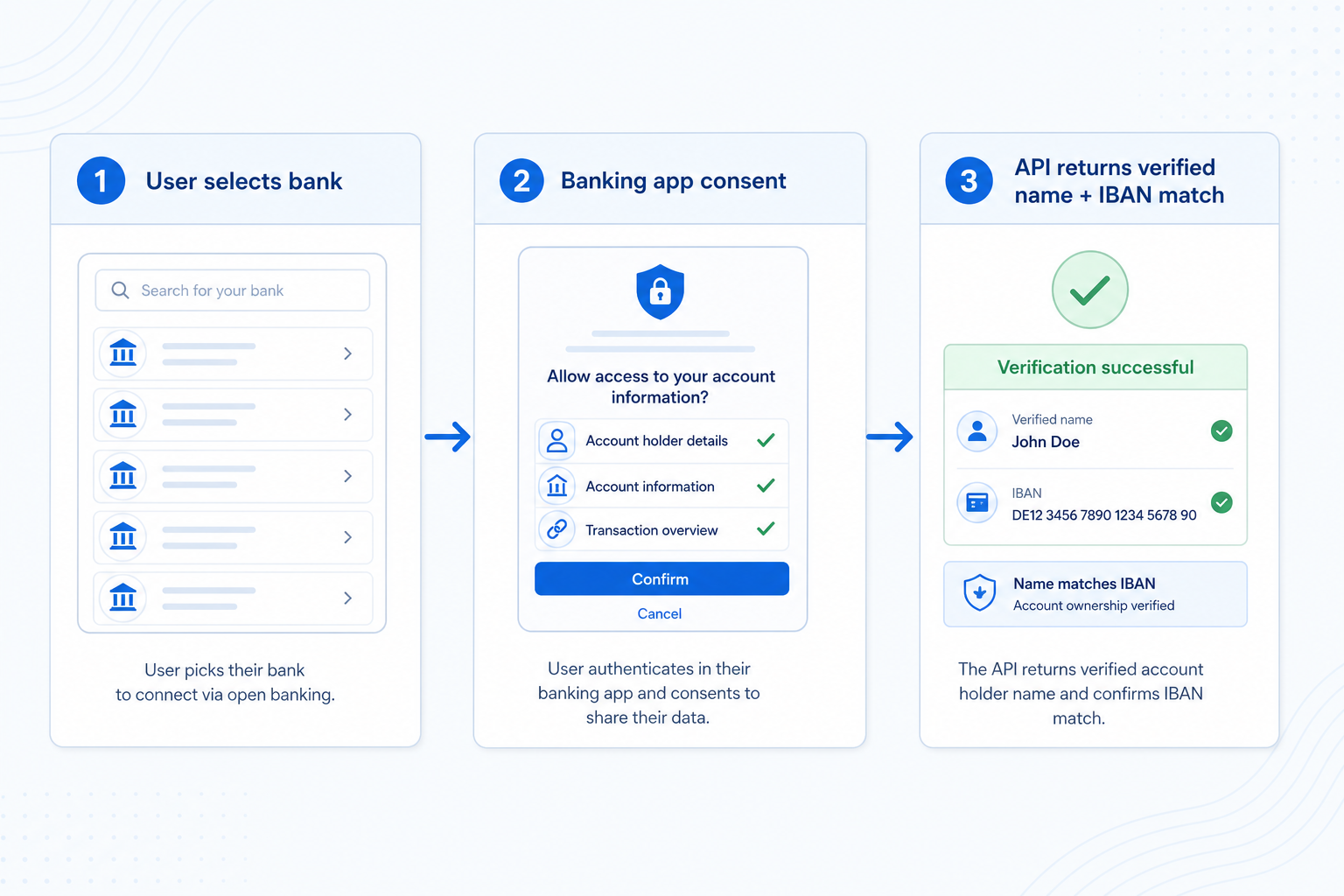

How open banking verification works in one integration

Most instant checks use account information with customer consent: the user proves they control the account through their bank’s app, and the provider returns account details your system compares to what you collected (name, company name, IBAN).

Typical flow:

- Collect details — IBAN and legal name (or company registration name for B2B).

- Redirect or embedded bank selection — user picks their institution.

- Strong customer authentication — handled by the bank; you do not see credentials.

- API response — holder name, masked or full account identifiers, and a match outcome.

- Downstream action — unlock payout, save mandate, or flag manual review.

Some products add a penny-test payment or combined verify-and-pay: first payment initiation doubles as ownership proof. That is slower than pure AIS-style verification but useful when you will charge the same account immediately after — a pattern common in open banking for SaaS B2B onboarding.

Trade-off: consent is required every time unless your provider supports refresh rules you can legally rely on; not all banks expose holder name on every account type (e.g. some business accounts).

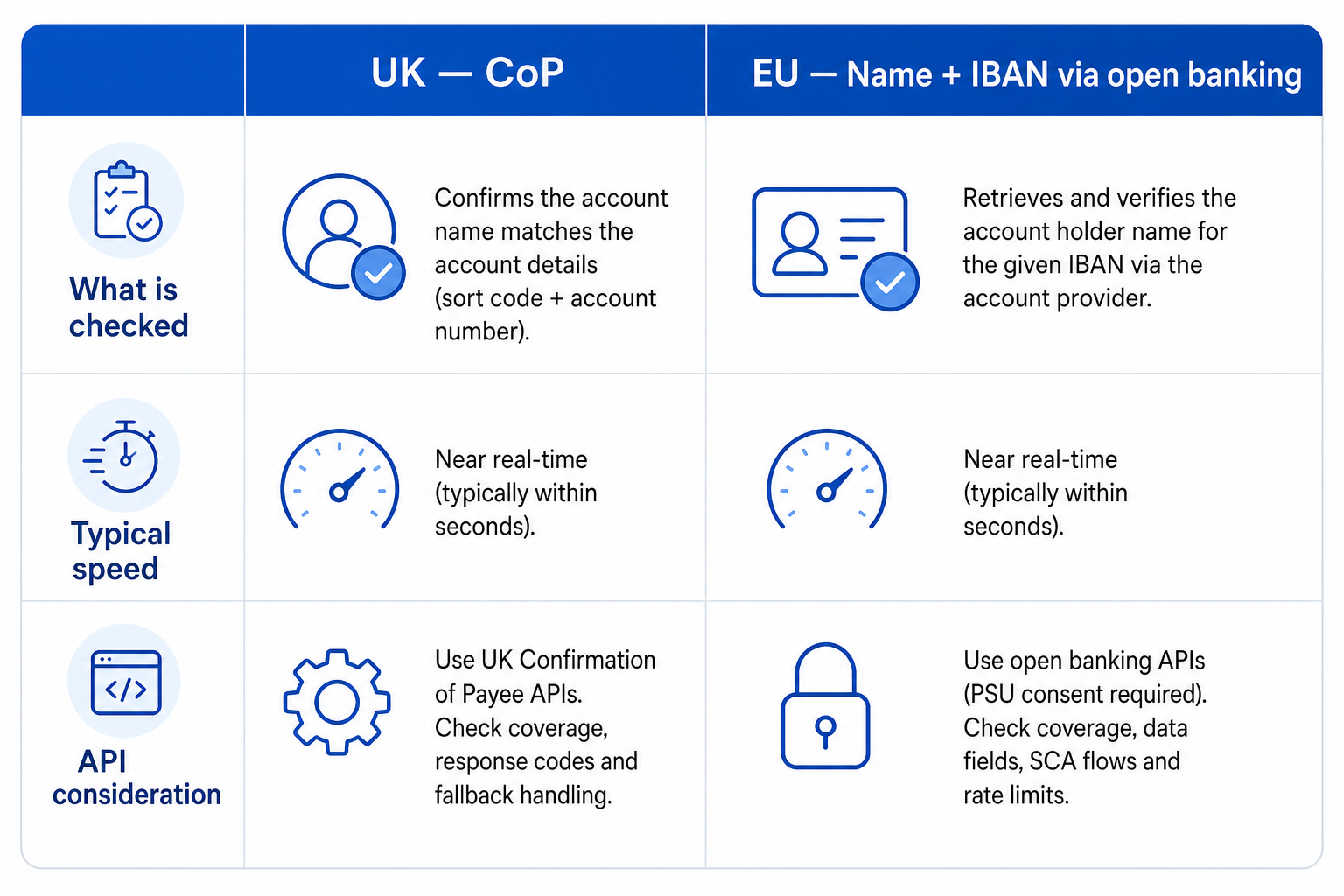

UK Confirmation of Payee vs EU name-and-IBAN checks

Verification is not one global standard. Your API provider must support the check type your corridor needs.

United Kingdom

In the UK, Confirmation of Payee (CoP) is the scheme many users expect when sending money to a new payee. Open banking verification APIs often integrate CoP-style name matching for UK sort code and account number, or IBAN where applicable. Ask whether CoP is a first-class product with documented match codes (MTCH, CMTC, NMTC, etc.) or a generic AIS name field you must interpret yourself.

Euro area and EU markets

In much of the EU, verification is name and IBAN consistency via open banking account data — not a single EU-wide CoP equivalent. Match quality depends on what each ASPSP returns: full legal name, truncated name, or joint-account ambiguity. For cross-border SEPA, validate behaviour on both payer and payee country banks you care about.

Multi-market products

If you operate in the UK and the EU, confirm whether one API contract covers both CoP and EU verification flows, or whether you maintain separate integrations and result schemas. The best open banking API providers for developers checklist for country-level bank lists applies here too — verification coverage is per bank, not per continent label.

| Market | Typical check | What to validate in sandbox |

|---|---|---|

| UK | CoP / payee name match | Match codes, sort-code accounts, business vs personal |

| EU / SEPA | AIS holder name vs IBAN | Joint accounts, missing name fields, non-Latin characters |

| Multi-market | Both schemas | One webhook format or documented per-region payloads |

Criteria to compare verification API providers

No provider wins every bank and every match type. Score against your onboarding funnel and risk model.

| Criterion | Why it matters |

|---|---|

| Bank coverage per country | Verification fails closed if the user’s bank is unsupported |

| Match rate on your top banks | Marketing “99%” means little without your institution mix |

| Response time (p95) | Drop-off rises when users wait on a spinner after bank login |

| Name matching logic | Exact, fuzzy, normalised company names; handling of GmbH, Ltd, accents |

| Business vs retail accounts | B2B payouts need legal-entity name rules, not consumer first name only |

| Webhooks and idempotency | Async completion when banks slow; safe retries on your side |

| Sandbox fidelity | Test banks that return no-match and partial-match, not only success |

| Compliance packaging | EU data residency, audit logs, sector acceptance (lending, marketplaces, iGaming) |

| Pricing model | Per check, per active user, or bundled with payments — affects unit economics at scale |

Run verification against your top ten customer banks in sandbox before any commercial shortlist. A provider strong for German retail neobanks may be weak for French business accounts your marketplace sellers use.

Instant open banking vs micro-deposits and manual review

| Method | Speed | Typical trade-off |

|---|---|---|

| Open banking (instant) | Seconds | Requires user action; bank coverage gaps |

| Micro-deposits | 1–3 days | High friction; cheap but slow for onboarding |

| Manual statement upload | Hours–days | Ops cost; fraud and quality variance |

| Registry-only IBAN format check | Milliseconds | Format valid ≠ account exists or name matches |

Instant verification fits when speed drives conversion — seller onboarding, lender funding, wallet activation, or pre-payout checks in open banking for fintech products. Micro-deposits still appear as a fallback for unsupported banks; ask if your provider documents a fallback path or if you build one yourself.

Integration patterns developers should plan for

Pre-payout gate — block withdrawals until verified: true on the beneficiary account. Common in marketplaces and open banking for e-commerce seller flows.

Onboarding-only — verify once at signup; store provider reference ID for later payment initiation against the same account.

Verify then collect — match name, then trigger Pay by Bank or SEPA Direct Debit on the verified IBAN (recurring collection builds on the same trust layer).

Step-up review — automatic pass on strong match; route fuzzy or unavailable to manual KYC.

Engineering checklist beyond the REST tour:

- Normalise names before compare (trim, legal suffixes, transliteration)

- Handle

name_not_availablewithout treating it as success - Log verification ID for audits; do not rely only on client-side state

- Rate-limit repeat attempts to reduce abuse

How to narrow your shortlist without a six-week bake-off

“Best open banking API provider for instant account verification” in search results usually reflects someone else’s bank mix. Yours should come from:

- List countries and banks where verification failures hurt most today.

- Run 20 sandbox checks — mix personal, business, match, no-match, and cancelled consent.

- Measure p95 latency and match clarity on those runs, not vendor slide decks.

- Compare two or three finalists on webhook quality and support responsiveness during the spike.

Structured matching on use case, countries, and technical needs gets you to sandbox-ready candidates faster than reading twelve generic API comparisons — then engineering time goes on proof, not discovery.

Frequently Asked Questions

What are the best open banking APIs for account verification?

There is no universal best — the right provider depends on which banks your users have, whether you need UK Confirmation of Payee, EU name-and-IBAN matching, or both, and how fast you need a pass/fail result in onboarding. Shortlist vendors with strong coverage on your top institutions, clear match semantics, and sandbox banks that expose failure paths.

What is the best open banking API provider for instant account verification?

Same criteria as above: match quality and bank coverage for your corridors beat generic rankings. Use sandbox tests on your top ten institutions before you sign.

How fast is instant bank account verification?

Most flows complete in seconds after the user finishes bank authentication — often under five seconds for supported institutions. Latency varies by bank load and redirect method; measure p95 on your production bank mix, not marketing averages.

Is open banking account verification the same as KYC?

No. Verification confirms account ownership and name consistency for a specific IBAN. Full KYC may still require identity documents, sanctions screening, and risk scoring. Open banking verification is usually one input to a broader compliance workflow.

Do I need Confirmation of Payee if I already use open banking verification?

In the UK, CoP is the standard payee-check mechanism many banks use. Open banking verification APIs often align with CoP outcomes for UK accounts. In the EU, there is no single CoP equivalent — you rely on account data returned after consent. Multi-market products should support both models.

Can I verify a business bank account instantly?

Often yes, when the bank returns the legal account name via open banking. Business accounts sometimes return trading names, joint holders, or incomplete labels — test your top B2B banks in sandbox and define fuzzy-match rules for company names.

What should we test in sandbox before signing a contract?

Unsupported bank handling, no-match and partial-match responses, webhook delivery on slow banks, business vs retail accounts, UK and EU corridors if both apply, and error codes your app can show users without generic failures.

Conclusion

The best open banking API provider for instant account verification is the one that reliably confirms name and account for your customers’ banks in the time your onboarding allows — with clear outcomes when a match is not possible. Map UK CoP vs EU checks, measure latency and match quality on real institutions, and plan fallbacks for gaps. Verification is a small API surface with outsized impact on fraud, payouts, and conversion; choose it with the same rigour as payments.

Related articles

- Income Verification With Open Banking for EU Lenders

Manual payslips and uploaded PDFs slow underwriting and still miss what actually hits the borrower’s account. Income verification open banking lets applicants…

- Open Banking for Lending: 8 Use Cases for EU Credit Teams

EU consumer and SME lenders still lose days on manual payslips, stale bank PDFs, and self-declared income that does not match what actually lands in the accoun…

- Open Banking Subscription Billing: UK & EU Bank-Rail Renewals

Subscription revenue bleeds when renewals depend on cards that expire, chargebacks that eat margin, or mandates that cannot match a variable invoice. Open bank…