Best Open Banking API Providers for Developers (2026)

Your team should not pick an open banking API provider from a headline bank count. The best open banking API providers for developers in 2026 are the ones that cover your customers’ countries and banks, give you a sandbox that behaves like production, and ship documentation your engineers can live in for months — not the vendor with the largest map on a sales deck. The right shortlist depends on region (EU, UK, US, LatAm) and build stage (hobby sandbox, indie live traffic, startup production, enterprise) as much as on API surface. This guide walks through that order: geography first, free-tier and pricing friction, sandbox and docs, API products, then how to narrow to two or three names you can pilot in a week.

Last updated: June 2026.

At a glance — typical fit by developer profile

Verify every name against your top banks in sandbox — no row below is a universal winner.

| Profile | Commonly shortlisted (examples) | Strong when you need… |

|---|---|---|

| EU/UK solo dev or side project | Enable Banking, Yapily Connect | Self-serve signup, restricted production on your own accounts, AIS/PIS without your own TPP licence |

| US solo dev or side project | Teller.io, SimpleFIN Bridge | Free or low-cost live connections; read-only personal tools vs full fintech stack |

| EU/UK startup — payments-led | TrueLayer, Volt, Token.io | Pay by Bank, VRP, hosted payment pages, UK/EU bank lists in Console |

| EU/UK startup — data-led | Tink, Salt Edge, Enable Banking | AIS, enrichment, verification; one platform for aggregation + downstream products |

| US startup | Plaid, Quiltt | Broad US coverage, Link-style hosted auth, SDKs; plan for sales-led production pricing |

| Enterprise / regulated TPP | Token.io, Salt Edge, Akoya (US) | VRP at scale, global breadth, or US API-only regulatory positioning |

For procurement-style comparison (pricing, RFP, commercial fit), see open banking provider comparison and how to choose an open banking provider in the EU. For account verification only, see instant account verification APIs.

Open banking API provider (for developers): A licensed aggregator that exposes one REST (or SDK) integration to reach many banks for payment initiation, account data, or verification — so your product team ships features instead of maintaining separate bank connectors per country.

Map your countries before you compare APIs

Start by listing where your users hold accounts — not where your company is registered. Open banking coverage is geographic: a provider strong in Germany is not automatically strong in Poland or Portugal, and UK open banking behaves differently from EU PSD2 rails after Brexit.

What to document before any demo call

- Customer countries — every market you sell into today and on the 12-month roadmap.

- Target banks and neobanks — the ten institutions that cover most of your volume (e.g. Revolut, ING, CaixaBank, Nordea).

- UK vs EU — if you need both, confirm whether one API contract and one consent UX cover both or whether you maintain separate flows.

- CEE and Nordics gaps — these markets often have thinner coverage; verify per bank, not per region label on a map.

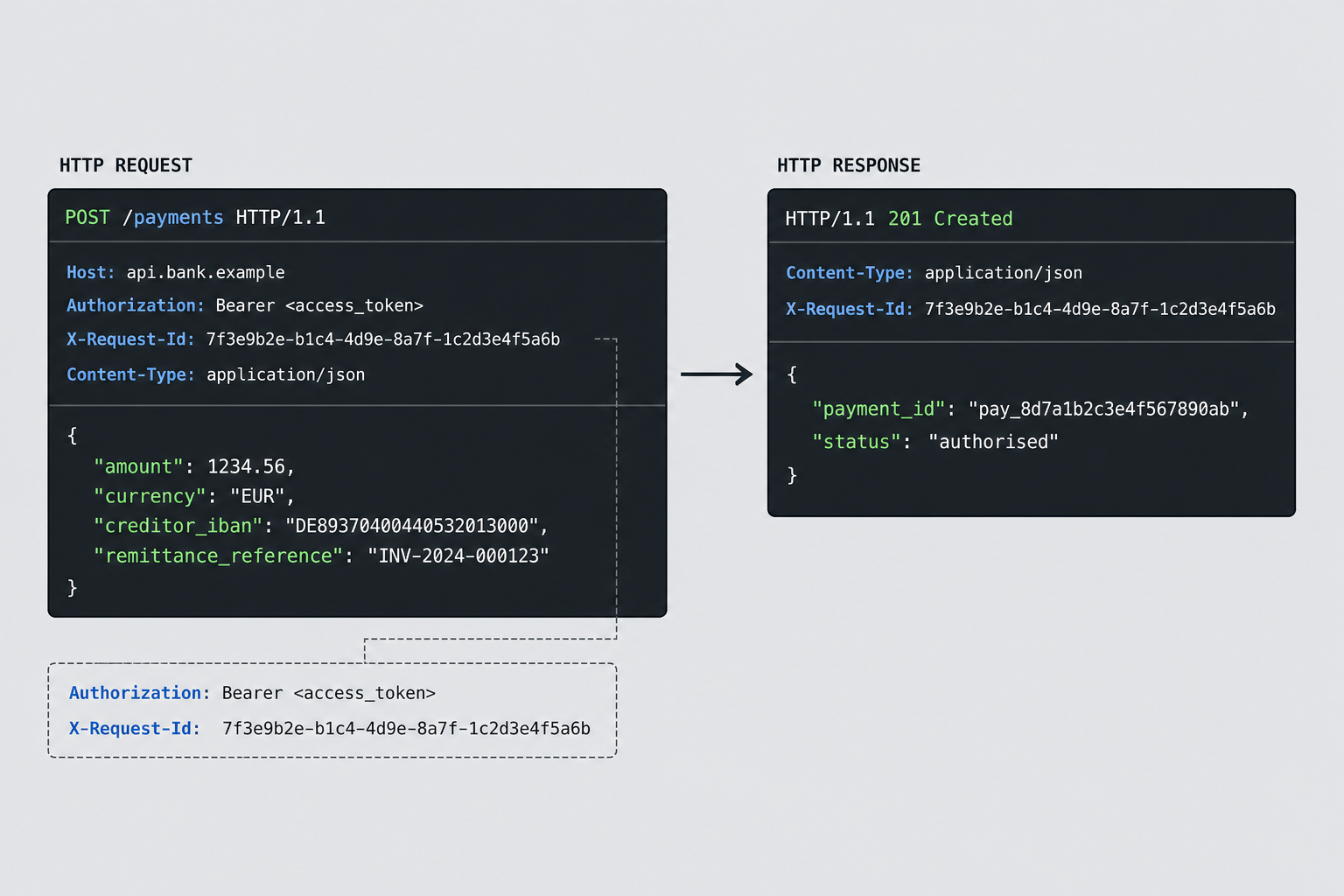

Ask each vendor for a per-country institution list (or console export), not a single “3,000+ banks” number. TrueLayer’s Supported Providers table in Console filters by country, product (Data, Payments, VRP), SEPA Instant, and auth flows — that is the level of detail you need for your spike.

US and LatAm: different default stacks

There is no single national open banking API in the US yet — despite CFPB Section 1033 momentum, production traffic still flows through aggregators (Plaid, MX, Finicity, Akoya, Teller.io). Shortlist by whether you need regulated bank APIs (Akoya) or fastest time-to-first-call (Plaid sandbox, Teller free tier). In Latin America, Belvo and Pluggy dominate sandbox-friendly onboarding for Mexico, Brazil, and regional Open Finance — treat them as separate spikes from EU vendors.

Coverage signals from major platforms (verify before you sign)

These figures come from providers’ own public pages — use them as a starting point for your RFP, then validate your banks in sandbox.

| Provider | Public coverage signal | Typical fit when… |

|---|---|---|

| Tink | 3,400+ institutions, 18 European markets (market capabilities docs) | You need broad AIS plus payments products on one platform |

| Yapily | 19 countries, 2,000+ banks (strong UK and Germany) | Developer-focused infrastructure across UK and core EU |

| Enable Banking | 2,700+ ASPSPs across 30 countries (provider claim) | EU/UK indie or small team; PSD2-native AIS/PIS with self-serve Control Panel |

| Token.io | 21 countries including UK, Nordics, and CEE | Enterprise payments and multi-market PIS |

| TrueLayer | Filterable provider table in Console (country, PIS/AIS/VRP) | UK-strong payments plus EU data; validate banks in Console |

| Plaid | 12,000+ institutions in 20+ countries (provider claim) | US/Canada-first; EU/UK production is sales-contracted |

Germany-strong is not France-strong. Treat every country as a separate acceptance test. Headline totals often mix banks, branches, and non-bank data sources — MX’s public “50,000+” count, for example, is not comparable to Tink’s institution count without reading each vendor’s definition.

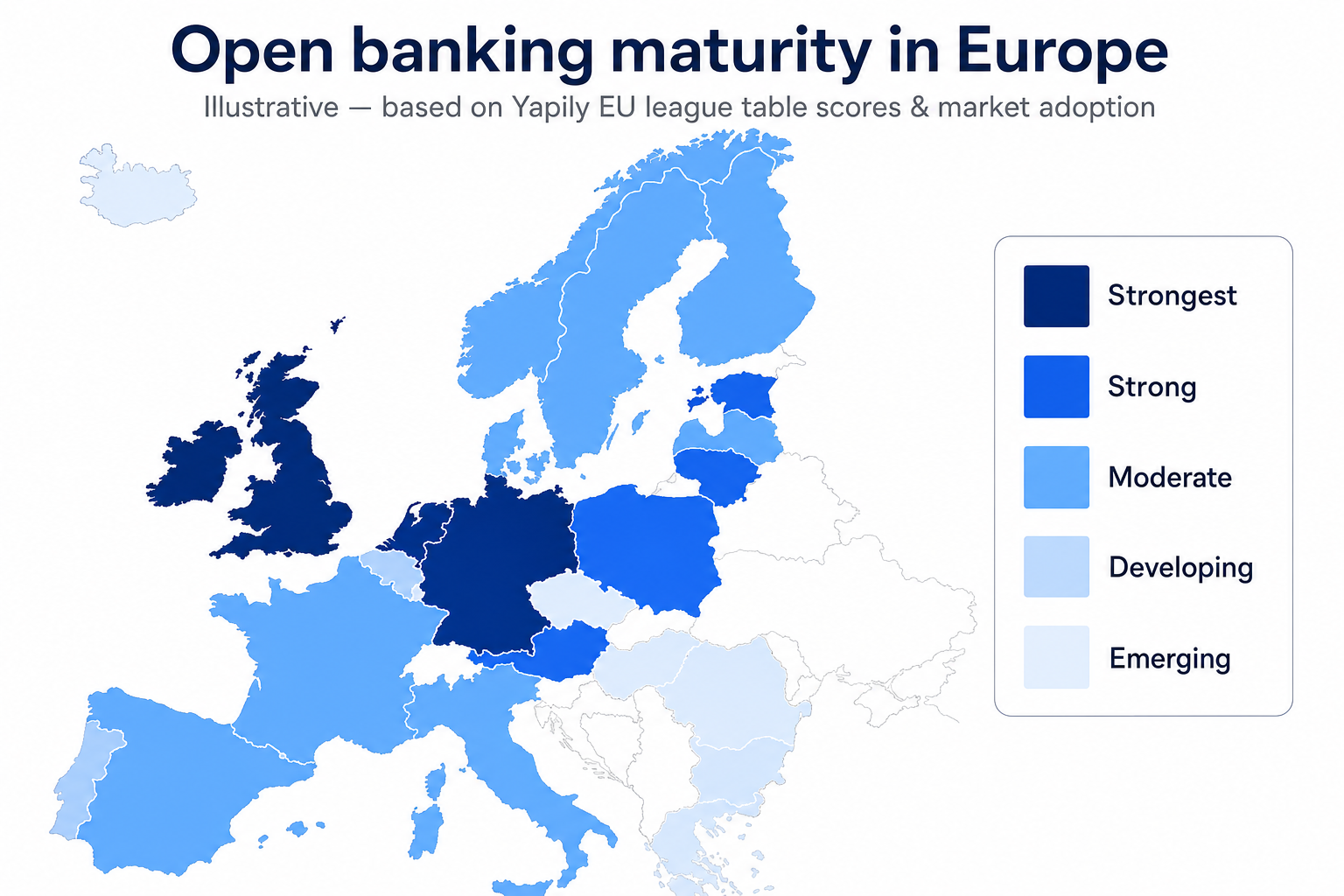

The map below illustrates regulatory and adoption maturity by country (darker = stronger open banking ecosystems), using Yapily’s European Open Banking League Table scores and complementary market data (e.g. UK and Germany leading on TPP volume per Konsentus Q4 2025). It is not a bank-level coverage map — still validate your institutions in sandbox.

Free tiers and indie-friendly APIs in 2026

Solo developers and small teams need a path to live traffic without a sales call — not only an unlimited sandbox. What you can use in production without negotiating varies sharply by region.

EU/UK — new builds: Enable Banking is the most practical replacement for teams that relied on GoCardless Bank Account Data (formerly Nordigen). Self-serve Control Panel signup, JWT-based REST, native SDKs, and Restricted Production (whitelist your own accounts for live testing) fit personal tools and early products. Community reports (e.g. open-source budgeting projects migrating off Nordigen) align with that pattern — still verify your banks.

EU/UK — GoCardless Bank Account Data (legacy only): As of mid-2025, GoCardless has stopped onboarding new customers to Bank Account Data, per independent reports (Invoice Ninja support forum, Actual Budget GitHub issue #5505). Existing integrations may continue; do not start new projects on this API unless you already have credentials. GoCardless has not published a broad press statement on the wind-down — monitor official channels if you maintain a legacy integration.

US — hobby and side projects: Teller.io offers a 100 free live connections on its developer tier (per its pricing page) plus an unrestricted sandbox. SimpleFIN Bridge charges $15/year for read-only access to thousands of US institutions (daily refresh, 24 requests/day) — suited to self-hosted budgeting, not production fintech.

Backup EU path: Yapily Connect lets unregulated developers operate under Yapily’s TPP licence with a free starter tier in sandbox — useful when you need hosted auth without holding your own eIDAS certificates.

For verification-heavy AIS (IBAN/name match), see instant account verification APIs — coverage is per bank, not per aggregator brand.

Pricing and onboarding friction developers feel first

Most production pricing is hidden behind sales — that is the single largest developer-experience gap in open banking. Plan your spike around who publishes enough numbers to budget without a call.

| What you can plan without sales (examples) | What still requires a call |

|---|---|

| Plaid pay-as-you-go tiers (partial US; EU/UK custom-only) | TrueLayer, Tink, Yapily, Volt, Token.io production |

| Teller free tier (100 live connections) | Trustly, Brite Payments, most enterprise EU merchants |

| SimpleFIN ($15/yr read-only) | MX, Finicity, Akoya production access |

| Enable Banking restricted production → paid scale | GoCardless BAD (closed to new signups) |

Plaid publishes pay-as-you-go and growth tiers; third-party analyses (e.g. Getmonetizely citing Tearsheet, 2025) cite rough per-link Auth costs of about $1.50–$2.00 at low volume falling toward $0.30–$0.60 at scale — directional only; get a quote before you model unit economics. Community reports flag surprise stacked product fees and long-standing connectivity issues with some US institutions — treat those as signals to test in your sandbox, not as settled verdicts.

Onboarding friction often matters more than docs polish: certificate setup (Token.io header signing), eIDAS QWAC/QSEAL for regulated TPPs, KYC for production (Volt, many US aggregators), or 12-month minimum contracts (e.g. Basiq in Australia for production). A fast sandbox signup does not mean a fast go-live.

Sandbox quality that actually predicts production

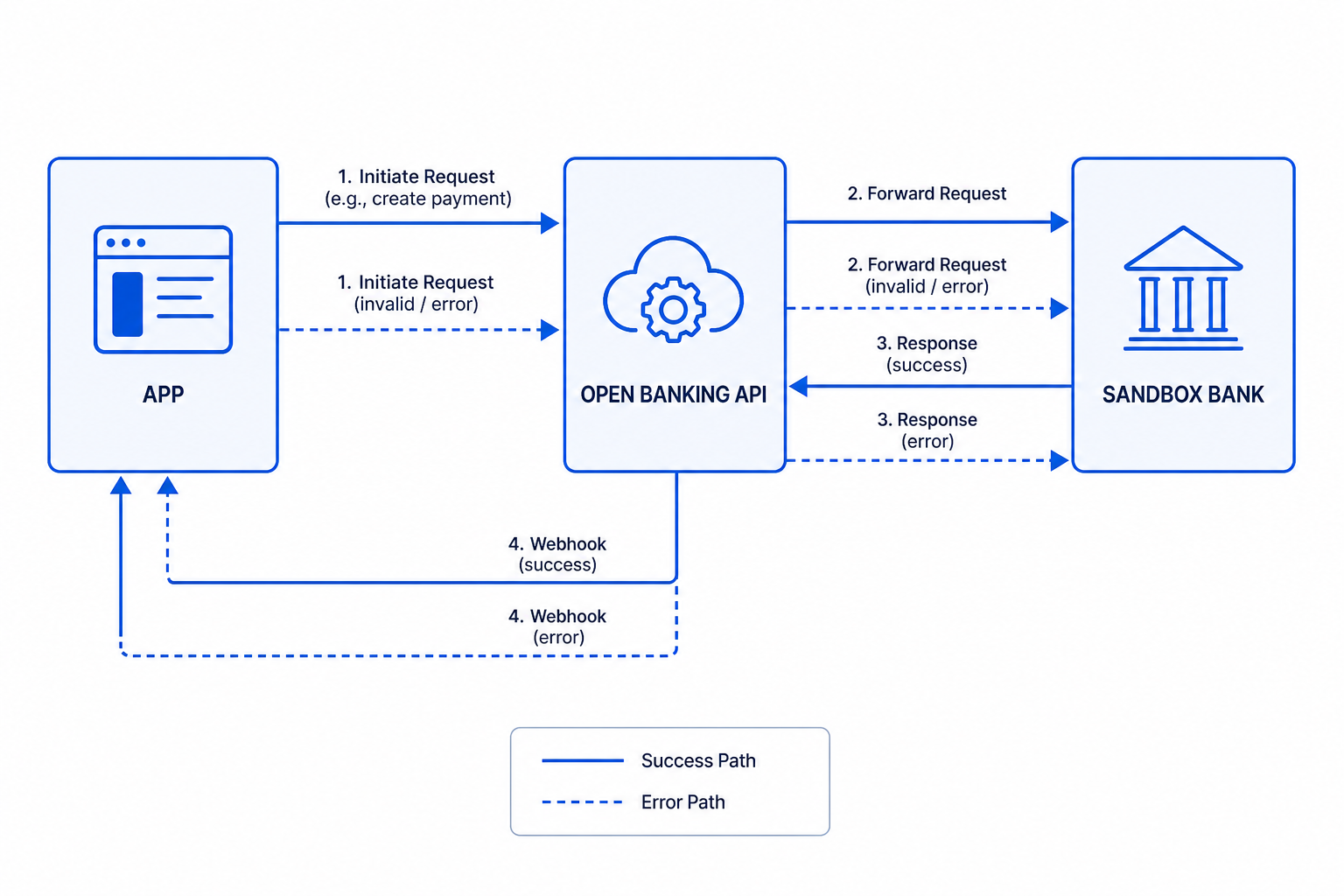

A sandbox that only returns happy paths teaches the wrong lessons. Before you compare open banking API providers for developers, run the same flows you expect in production — consent redirect, payment status, webhooks, and revocation — against test banks in each target country.

What good looks like:

- Institution parity — sandbox banks for DE, FR, and UK if those are live markets, not only one domestic mock.

- Webhook delivery — signed callbacks with the same payload shape as production; test idempotent retries.

- Unhappy paths — timeouts, partial AIS payloads, and failed payment statuses, not only

executed. - Traceability — request IDs that appear in the provider dashboard when production breaks at 2 a.m.

- Auth and errors — token refresh, consent expiry, and documented error codes for every failure mode you see in sandbox.

- Observability — correlate your logs with the provider dashboard before you go live.

Production gates to plan for: Akoya offers self-serve sandbox since 2022 but production still requires Data Recipient Hub agreements. Brite Payments publishes sandbox docs but issues credentials via sales. Basiq allows instant sandbox keys but production carries a 12-month minimum. Budget four to twelve weeks after sandbox sign-off for security review, contracts, and bank certification — parallelise legal and engineering.

Documentation and developer experience

Documentation is where your team spends the first four to eight weeks. Score providers on what you can verify in a two-day spike, not on portal polish.

Checklist for a 48-hour doc review

| Area | What to test |

|---|---|

| Onboarding | Sandbox API keys, environment URLs, and “first successful call” without a sales call |

| Reference | OpenAPI or Postman collection; every error code you hit in sandbox documented |

| Auth | OAuth or token flow explained with copy-paste examples |

| SDKs | Official client for your stack (Node, Python, etc.) or clear REST-only path |

| Versioning | Changelog, deprecation policy, and breaking-change notice period |

| Operations | Status page, incident history, and support channel for integration blockers |

Fast time-to-first-call (often under 15 minutes): Plaid Sandbox and Plaid Link, Teller sandbox, Enable Banking Quick Start, Belvo sandbox keys, SimpleFIN demo token curl. 30–60 minutes: Tink Console, TrueLayer Console with sandbox- client IDs, Yapily preconfigured Modelo sandboxes. If your spike needs three support tickets to complete one consent flow, factor that into total cost of ownership.

Yapily routes developers to docs.yapily.com and an API Console; TrueLayer ships Console, Postman, and Insomnia plugins; Enable Banking documents working SDK samples in Java, JavaScript, and Python.

API surface beyond the REST tour

Match API products to the job — pay-in, payout, onboarding, or lending signals — before you admire endpoint counts.

Payments (PIS)

Payment initiation covers Pay by Bank checkout, wallet top-ups, invoice collection, and disbursements. Ask about:

- Redirect vs app-to-app vs decoupled flows per bank

- Final payment status (

executedvsauthorised) per institution - SEPA Instant support where you need sub-minute settlement

- Stable payment references for reconciliation

Account data (AIS)

Account aggregation powers verification, affordability, and treasury views. Tink publishes 3,400+ institutions and background refresh up to four times per day on connected accounts — confirm refresh rules and re-consent UX for your use case.

Verification and VRP

Many products combine ownership checks with payments. Variable recurring payments (VRP) are the UK/EU stickiness battleground for subscriptions and sweeping — confirm per-bank VRP support (TrueLayer’s provider table exposes this). In the US, Section 1033 and FDX alignment favour aggregators investing in regulated data access (Akoya, Finicity, MX) alongside Plaid.

Hosted Link vs raw bank APIs

Plaid Link, TrueLayer hosted payment pages, Belvo Connect, Yapily Hosted Pages, and similar widgets absorb bank-specific SCA and redirect quirks — weeks saved vs raw PSD2 integration. Use raw APIs when you are a regulated TPP shipping a custom UX or when Token.io/Salt Edge expect your own eIDAS certificates. Yapily Connect and Enable Banking explicitly support unregulated teams using the aggregator’s licence.

Webhooks and reconciliation

Production systems need:

- Idempotent webhook handlers and replay safety

- Consistent metadata (IBAN, remitter, reference) on success and failure

- Rate limits and pagination on AIS endpoints — some banks cap daily calls per account

If you are building multi-market fintech features on top of this stack, see open banking for fintech for how product teams sequence PIS, AIS, and verification — this post stays on vendor selection for developers.

Providers developers evaluate in 2026 (by fit, not rank)

No single aggregator wins every use case. Capsules below are typical engineering fits — your sandbox results override them. Profiles on openbankingcompare.com add capability tags; confirm bank-level coverage in each console.

| Group | Examples | Developer notes |

|---|---|---|

| Broad EU + UK connectivity | Tink, Yapily, TrueLayer, Salt Edge, Enable Banking | Compare institution lists per country; check combined PIS + AIS |

| Payments and checkout rails | TrueLayer, Volt, Trustly, Token.io | Conversion, Instant payouts, VRP roadmaps |

| US connectivity | Plaid, Teller.io, Akoya, MX, Finicity | Plaid for breadth; Teller for indie free tier; Akoya for bank-API positioning |

| AIS and verification-led | Enable Banking, Tink, Salt Edge | Onboarding and data quality; GoCardless BAD only for existing integrations |

| LatAm | Belvo, Pluggy, Fintoc | Belvo sandbox is among the cleanest API references in the category |

Enable Banking — Pan-European AIS/PIS; self-serve Control Panel; Restricted Production for own accounts; strong fit for EU/UK indie devs post–GoCardless BAD closure.

Tink — Visa-acquired platform; 3,400+ institutions across 18 markets (market capabilities). Fits VC-backed EU fintechs and data-heavy products; production is enterprise-gated.

Yapily — 19 countries, white-label REST, Yapily Connect for unregulated teams.

TrueLayer — UK/EU payments and data; VRP and Pay by Bank; filter banks in Console.

Plaid — US/Canada default for many startups; unlimited free Sandbox; EU/UK production requires custom sales. Build a thin provider-abstraction layer early if you may add MX, Finicity, or Akoya later.

Teller.io — US indie option: 100 free live connections; reverse-engineered bank access — fast until a bank changes behaviour; plan a fallback.

Token.io — Enterprise PIS/VRP across Europe; certificate signing; reseller and TPP tooling.

GoCardless Bank Account Data — Existing customers only for AIS; mock SANDBOXFINANCE_SFIN0000 in docs remains useful for learning patterns, not for new production commitments.

Belvo — Mexico, Brazil, Colombia; self-serve sandbox with strong API reference UX.

Volt, Salt Edge, Trustly — A2A payments, global breadth, or merchant-scale Pay by Bank — confirm sector acceptance and country lists in sandbox.

Sandbox, signup, and free production tier (condensed)

| Provider | Region | Sandbox | Self-serve signup | Free prod tier | Typical fit |

|---|---|---|---|---|---|

| Plaid | US/CA/EU/UK | Free, unlimited | Yes (US); EU/UK prod sales | ~200 live calls/product | US startup → enterprise |

| TrueLayer | UK/EU | Free | Yes | No | UK/EU payments, VRP |

| Tink | EU/UK | Free | Dev account | No | EU data + large fintech |

| Yapily | EU/UK | Free | Yes | Starter/sandbox only | White-label EU infra |

| Enable Banking | EU | Free | Yes (email link) | Restricted prod (own accounts) | EU/UK indie, small teams |

| GoCardless BAD | EU/UK | Yes (legacy) | Closed to new | Legacy only | Existing integrations |

| Teller.io | US | Free | Yes | 100 live connections | US side projects |

| SimpleFIN | US | Demo token | Yes | $15/yr read-only | Self-hosted PFM |

| Akoya | US | Self-serve | Sandbox yes; prod vetted | No | US regulatory-clean stack |

| Belvo | LatAm | Free | Yes | Sales for prod | LatAm fintech |

| Token.io | EU/UK | Notional banks | TPP signup | No | Regulated TPP, VRP scale |

| Salt Edge | Global | Fake Banks | Yes | No | Global breadth |

| Volt | UK/EU/global | Free | Yes + KYC | No | International A2A |

| SnapTrade | Investments | Free | Yes | Free starter | Portfolio dashboards |

Once you have two or three contenders on paper, teams stuck on commercial fit, licensing, or sector acceptance after sandbox validation can use the provider directory to compare capability tags — then use our short matchmaking form to align requirements with vendors without a six-week RFP tour.

How to narrow the list without wasted cycles

You do not need a six-week bake-off or eight parallel vendor tours. Most teams already know their constraints — countries, banks, PIS vs AIS, sector — before they open a comparison spreadsheet. The work is matching those constraints to the right few names, not rediscovering basics from ten identical sales decks.

Filter on facts first. Geography and product fit eliminate a large share of the market: payments-only rails drop out if you need AIS; a UK-strong stack is a poor default if your volume is in Poland and Romania. Use the same rubric throughout this article (markets, sandbox, docs, API surface) so every name is scored consistently.

Compare in one place. Rebuilding capability matrices from PDFs and email threads is where weeks disappear. The provider directory maps markets, use cases, and engineering signals (sandbox, documentation, API quality) so you start from a short list aligned to your checklist — then confirm bank-level coverage in each vendor’s console or institution export.

Spend engineering time on validation, not discovery. Once two or three providers fit on paper, run sandbox flows on your corridors (consent, one PIS or AIS path, webhooks). That step separates contenders; it should not require evaluating a dozen aggregators from zero.

For pricing, licensing, and commercial fit alongside technical criteria, see how to shortlist open banking providers without a six-week bake-off and open banking provider comparison: what to evaluate before you shortlist.

Frequently Asked Questions

What are the best open banking API providers for developers in 2026?

There is no universal winner. The right provider is the one with reliable connections to your users’ banks, a sandbox that mirrors those markets, and documentation your team can integrate without constant escalations. Shortlist by country fit first, then engineering DX, then commercial terms.

How do I check if a provider covers my users’ banks?

Request a per-country institution list or use the vendor’s console (e.g. TrueLayer’s Supported Providers table). Match your top ten banks by customer volume. Marketing totals like “3,400 institutions” do not replace that check.

Is UK open banking the same API as EU PSD2?

Often one vendor covers both, but consent flows, directories, and settlement behaviour differ. If you operate in the UK and the EU, test both corridors in sandbox and confirm whether you need separate app registrations or redirect URLs.

Do developers need their own PSD2 licence?

Usually no for early stages. You integrate as a partner of a licensed AISP or PISP. If you hold end-user funds or present raw account data under your brand, legal review is mandatory — the licensed provider’s role in the chain must be explicit in contract.

What makes a good open banking sandbox for developers?

Test banks in each target country, realistic payment and consent statuses, webhooks matching production payloads, and documented error codes. A single global mock bank is fine for hello-world; it is not enough for go-live sign-off.

How long does it take to go from sandbox to production?

Typical ranges are four to twelve weeks after sandbox sign-off: security review, contract, bank certification, and your own QA. Parallelise legal and technical tracks; the critical path is often bank-specific certification, not your application code.

Is GoCardless Bank Account Data (Nordigen) still free for new projects?

No — not for new signups. Independent reports from mid-2025 indicate GoCardless stopped onboarding new Bank Account Data customers while existing integrations may continue. For new EU/UK AIS builds, spike Enable Banking or Yapily Connect instead, and verify status on GoCardless official channels if you already have credentials.

What is a practical free or low-cost open banking API for EU developers in 2026?

Enable Banking is the common path for new EU/UK indie work: self-serve signup, sandbox, and Restricted Production on your own accounts before paid scale. Yapily’s free starter via Yapily Connect suits teams that want hosted auth under the aggregator’s licence. Always validate your target banks in sandbox — free tiers do not fix coverage gaps.

What should US developers use for a side project instead of Plaid production?

Plaid Sandbox remains the standard way to learn Link and auth patterns at no cost; production access is sales-led with opaque pricing for many teams. Teller.io’s developer tier (100 free live connections, per its pricing page) is the mainstream indie alternative for live US traffic. SimpleFIN Bridge ($15/year) fits read-only personal finance tools with daily refresh limits — not card-style fintech products.

Conclusion

The best open banking API providers for developers in 2026 are the ones that pass your country and bank checklist, match your build stage (sandbox hobby vs production startup), and prove themselves in a sandbox that fails realistically. Compare coverage, free-tier reality, pricing friction, documentation, and API products in that order — narrow on constraints first, validate the final two or three in sandbox, then commit. This page was materially updated in June 2026 (GoCardless BAD closure, Enable Banking, US indie paths). A structured comparison beats an open-ended RFP when your markets and use cases are already defined.

Related articles

- PSD3 Open Banking: What EU Teams Should Plan Now

If you rely on bank APIs to collect payments, verify accounts, or pull transaction data, PSD3 open banking is the EU package that will reset your integration r…

- Open Banking Utility Payments: How Suppliers Collect Bills

Utility billing teams lose margin on three predictable leaks: card interchange on high-volume inbound payments, failed direct debits that trigger dunning and c…

- Build vs Buy Open Banking: When to Partner or Build In-House

Build vs buy open banking is the decision that determines whether your first live bank payment ships in weeks or years. Most EU B2B teams should buy — integrat…