Best Open Banking Providers for Recurring Transactions

Recurring revenue breaks when collection depends on the wrong rail for the country you are billing in. A provider strong for one-off Pay by Bank in Germany is not automatically the right fit for pull-based renewals in the UK, the euro area, or the Nordics — and US customers run on ACH, not SEPA. The best open banking providers for recurring transactions are the ones that cover your customer banks, support the mandate or consent model your market uses, and hand your billing system reliable status events. This guide maps regional rails first, then what to compare before you commit — without treating “recurring” as a single global product.

Recurring transactions via open banking: Collecting repeat charges from a customer's bank account after they consent — using pay-by-bank setup, direct debit–style mandates, or variable recurring payment agreements, depending on country — usually through one licensed provider integration instead of wiring every bank yourself.

Why “recurring” is not one product globally

Recurring collection is a business outcome; the underlying rail is always local. Open banking providers aggregate bank connections and consent flows, but they still plug into scheme rules defined per country — SEPA Direct Debit in the euro area, Bacs Direct Debit in the UK, ACH debits in the US, and national batch schemes in Sweden, Norway, and Denmark. If your customers span multiple regions, you are choosing a provider stack (or a partner model), not a single API feature flag called “recurring.”

That is why a commercial search for the best open banking providers for recurring transactions should start with where your payers bank, not with a leaderboard. Coverage, mandate types, retry behaviour, and settlement timing all change when you cross a border — even inside Europe.

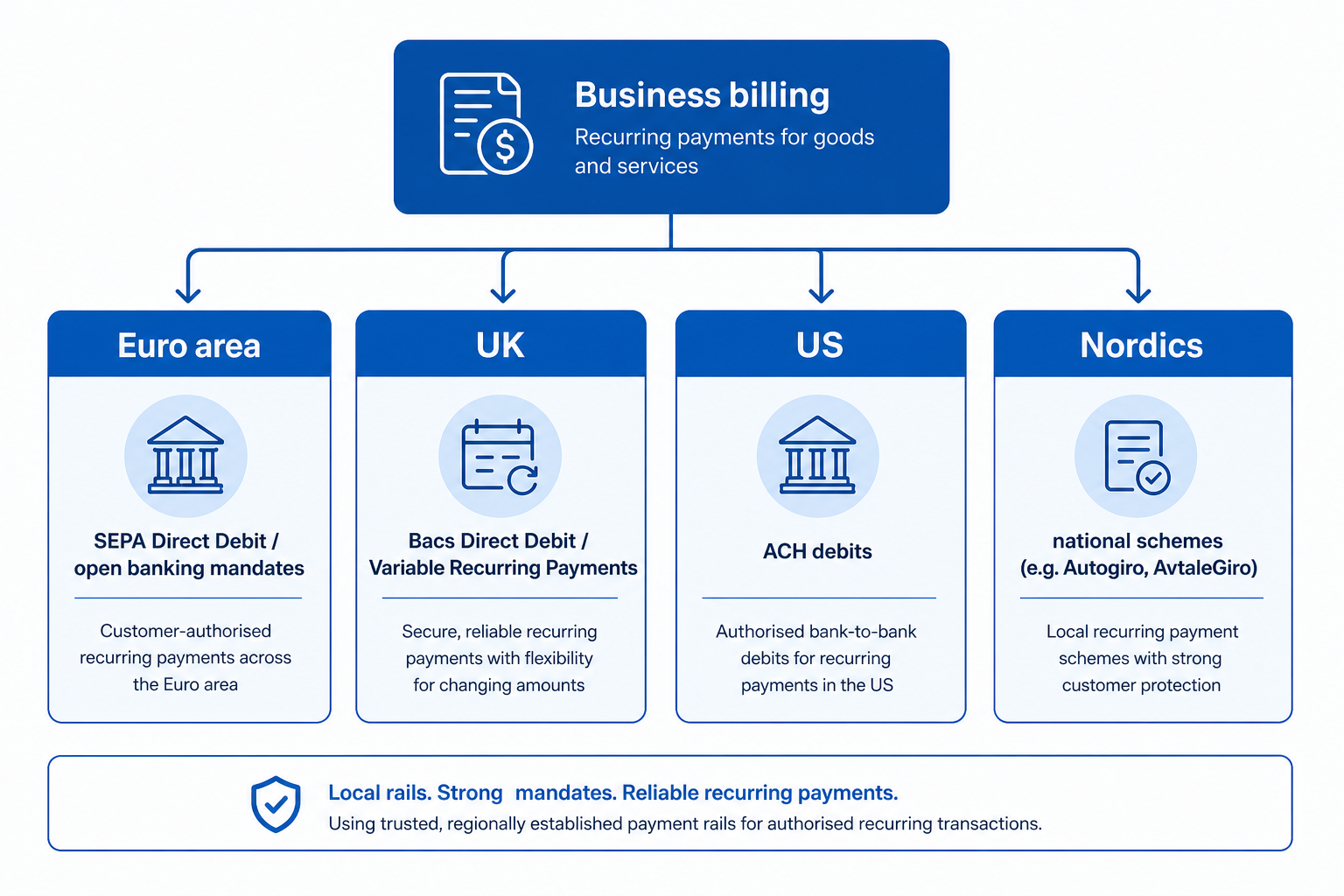

Regional rails to map before you shortlist providers

Match each customer segment to the rail their bank actually supports. Open banking sits on top of these schemes; it does not replace them.

Euro area — SEPA and open banking mandates

In SEPA countries, many businesses combine an initial Pay by Bank authorisation with a SEPA Direct Debit mandate for renewals. Open banking providers differ in whether they manage mandate creation, creditor identifiers, and pre-notification rules — or only the first payment and account verification. For subscription and invoice businesses in the EU, confirm SEPA Core (and Core1 if you need it) plus honest bank-level mandate support, not just payment initiation for one-off amounts.

United Kingdom — Bacs and Variable Recurring Payments

UK recurring collection often runs on Bacs Direct Debit for fixed schedules. Variable Recurring Payments (VRP) — a UK open-banking pattern for consent-based repeat pulls within agreed limits — matters when amounts change each period (usage billing, insurance premiums, variable subscriptions). Not every UK-connected bank supports VRP for your use case; ask for a filtered institution list, not a headline bank count.

United States — ACH

US recurring debits typically run on ACH (with Nacha scheme rules), not PSD2-style open banking. If you operate in the US, evaluate providers with ACH debit credentials and return-code handling; a EU-focused open banking aggregator may route you to a different partner or tell you to integrate ACH separately. Treat US and EU as separate acceptance tests.

Nordics — national schemes alongside SEPA

Sweden, Norway, and Denmark participate in SEPA for many euro-denominated flows, but domestic recurring collection often uses national schemes — for example Autogiro in Sweden, AvtaleGiro in Norway, and Betalingsservice-style pull payments in Denmark. Adoption of pure open-banking recurring varies by bank and use case. If the Nordics are a meaningful share of revenue, validate domestic scheme support and not only “SEPA + open banking” marketing copy.

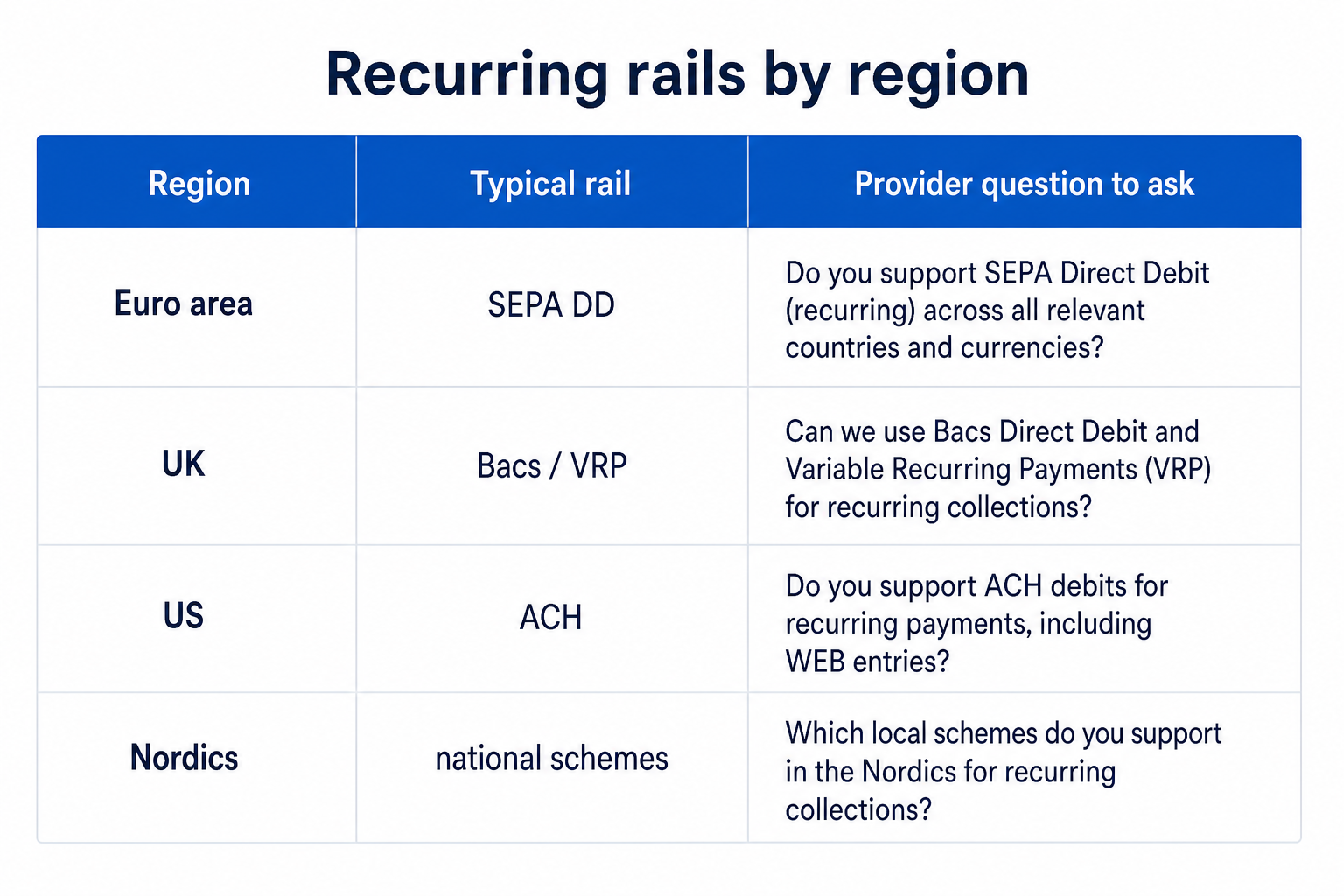

| Region | Typical recurring rail | What to ask providers |

|---|---|---|

| Euro area | SEPA Direct Debit + Pay by Bank setup | Mandate management, creditor ID, pre-notification, bank coverage |

| UK | Bacs DD; VRP for variable amounts | VRP-capable banks for your segment; Bacs sponsor if needed |

| US | ACH debits | ACH origination, returns, Nacha compliance path |

| Nordics | National schemes + SEPA where relevant | Per-country Autogiro / AvtaleGiro / domestic pull support |

What open banking providers actually deliver for recurring

Providers are not interchangeable “recurring APIs.” Most help you with some combination of:

- Account verification — confirm the payer owns the IBAN or account before you store it for collection.

- First payment / consent — customer authorises in the banking app; you get a token or mandate starting point.

- Repeat collection — direct debit file, VRP sweep, or scheme-specific pull, depending on market.

- Status and reconciliation — webhooks, references, and failure codes your billing system can act on.

A pattern that works across many EU businesses: verify the account, take the first charge via Pay by Bank, then activate SEPA Direct Debit for the subscription amount. UK variable businesses often pilot VRP where banks support it. US flows parallel this with ACH verification and debit scheduling — through a different vendor skill set.

Trade-offs are consistent everywhere: first payment still needs customer action; mandates can fail for insufficient funds; cross-border billing may need separate creditor arrangements. The provider’s job is to make those flows operable from one integration contract where possible — not to promise one global “subscribe” button.

For vertical-specific rollout (SaaS renewals, usage true-ups, dunning), see open banking for SaaS. For sandbox and bank-directory depth, see best open banking API providers for developers.

Criteria to compare providers (without picking a single winner)

No single vendor wins every corridor. Use a checklist aligned to your countries and billing model.

| Criterion | Why it matters for recurring |

|---|---|

| Bank coverage per country | A mandate is useless if your customer’s bank is unsupported |

| Recurring product fit | SEPA DD, VRP, ACH, or Nordic scheme — which are first-class, not roadmap |

| Variable vs fixed amounts | Usage billing needs VRP or one-off authorisations; fixed subs need DD |

| Mandate lifecycle | Create, amend, cancel, and dispute handling exposed to your app |

| Webhooks and references | Billing IDs must survive retries and finance reconciliation |

| Retry and dunning hooks | Failed pulls should map to your subscription logic cleanly |

| Settlement and reporting | When cash hits your account vs when the customer was debited |

| Multi-entity / multi-currency | Separate creditor IDs or entities per market |

| Data residency and contracts | EU hosting, sector acceptance (insurance, lending, platforms) |

Run the same flows in sandbox that you expect in production: consent, first payment, a repeat pull (or simulated mandate event), revocation, and a failure path. A provider that demos well on one German bank is not validated for UK VRP or Nordic Autogiro until you test those corridors.

Sensible rollout order

Most teams reduce risk by sequencing markets instead of flipping a global switch:

- Map payers — top countries by revenue and failed-payment pain.

- Pick one rail per country — SEPA DD, Bacs, VRP, ACH, or Nordic scheme; avoid mixing models in v1.

- Pilot one segment — e.g. annual B2B renewals or one subscription tier.

- Prove reconciliation — payment status lands in billing with stable references.

- Expand — add countries only after mandate and webhook behaviour is signed off.

Insurance, utilities, memberships, and open banking for fintech products all reuse this sequence; only the compliance packaging and amount variability differ.

How to narrow your shortlist fairly

“Best” in search results usually means “best for someone else’s country mix.” Your shortlist should be built from:

- Corridor fit — do they cover the banks where your customers actually pay?

- Recurring mechanics — mandates, VRP, or ACH debits as shipped products, not slides

- Billing integration cost — webhooks, idempotency, and reference fields your stack needs

- Operational evidence — SLAs, incident history, and sandbox parity with production markets

Comparing twelve vendors from marketing PDFs burns weeks. A structured match on use case, countries, and technical requirements gets you to two or three sandbox candidates faster — then engineering time goes on validation, not discovery.

Frequently Asked Questions

What are the best open banking providers for recurring transactions?

There is no universal winner — the right providers depend on where your customers bank and which recurring rail applies (SEPA Direct Debit in the euro area, Bacs or VRP in the UK, ACH in the US, national schemes in the Nordics). Shortlist vendors that support your countries, mandate or consent model, and billing webhooks, then validate in sandbox on your top banks.

How is recurring collection different from one-off Pay by Bank?

One-off Pay by Bank authorises a single payment in the banking app. Recurring collection stores a consent or mandate so future charges can be pulled without the customer approving every time, within scheme rules. Many businesses use Pay by Bank for the first payment and a direct debit or VRP agreement for renewals.

Do I need separate providers for the UK, EU, US, and Nordics?

Sometimes one group covers UK and EU open banking with strong SEPA and Bacs support; US ACH often comes from a different specialist. Nordics may need explicit domestic scheme support beyond a generic “EU” label. Plan integrations per corridor rather than assuming one contract covers every recurring model.

What is Variable Recurring Payments (VRP) and when do I need it?

VRP is a UK open-banking pattern for repeat collections within customer-agreed limits — useful when the amount changes each cycle. Fixed subscriptions may use Bacs Direct Debit instead. Ask for bank-level VRP support for your customer segment; it is not available at every UK institution.

Can open banking replace card-on-file for subscriptions?

It can reduce card expiry churn where bank mandates or VRP work well, especially for B2B and markets with strong banking-app adoption. Cards still matter for global coverage and consumer habit. Many operators offer bank pay alongside card and measure involuntary churn per segment.

How do we evaluate providers without a months-long bake-off?

Define countries, recurring rail, and billing integration requirements first. Run sandbox tests on your top three to five customer banks per market. Compare webhook quality, mandate lifecycle, and failure handling — not headline bank counts alone.

Conclusion

The best open banking providers for recurring transactions are the ones aligned to your customers’ countries and schemes — SEPA, Bacs, VRP, ACH, or Nordic national rails — with mandate or consent flows your billing system can operate day to day. Start with a regional map, compare coverage and recurring products honestly, and prove reconciliation before you scale. Recurring revenue is operational; provider choice should be too.

Related articles

- cVRP Explained: Commercial Variable Recurring Payments

cVRP stands for Commercial Variable Recurring Payments — a UK way to collect repeat payments straight from a customer’s bank account after they approve once in…

- Bank on File vs Card on File: EU & UK Recurring Billing

Recurring revenue depends on a stored funding method you can charge again without asking the customer to re-enter details every cycle. Card on file is the defa…

- Variable Recurring Payments (VRP) for EU and UK Teams

Subscription and usage billing breaks when every renewal needs a new card authorisation or a fixed direct debit that cannot match the invoice. Variable recurri…