Open Banking Utility Payments: How Suppliers Collect Bills

Utility billing teams lose margin on three predictable leaks: card interchange on high-volume inbound payments, failed direct debits that trigger dunning and churn, and manual reconciliation when customers pay from the wrong account. Open banking utility payments let regulated suppliers collect variable bills, verify accounts at new connections, and — where schemes allow — run recurring bank-rail authorisations with lower cost and clearer audit trails than card-on-file alone. This playbook maps six use cases energy, water, gas, and telecom billing leads can pilot first, plus provider criteria and trade-offs before you commit.

Open banking utility payments: Using regulated bank APIs — typically payment initiation and account verification — so energy, water, gas, and telecom suppliers collect inbound bills, confirm customer accounts, and reconcile payments without relying solely on cards or legacy direct debit files. Customer consent is granted in their banking app; funds move account-to-account.

Why are utilities adopting open banking for bill collection?

Utilities adopt open banking because variable bills and high churn make card and direct-debit-only stacks expensive. A typical energy or telecom supplier sees seasonal usage swings, mid-contract tariff changes, and a steady stream of failed collections that each cost contact-centre time and sometimes the customer entirely. Pay by bank on a one-off or first bill gives instant confirmation and a verified IBAN you can reuse; recurring bank rails (including commercial variable recurring payments in the UK) reduce interchange on repeat cycles where schemes permit.

The pattern differs by market:

- EU mainland — pay by bank initiation for ad-hoc and first payments; SEPA Direct Debit for stable schedules; account verification to cut wrong-IBAN refunds

- UK — UK Payments Initiative (UKPI) Wave 1 (from June 2026) covers regulated utilities and telecoms for commercial variable recurring payments (cVRP), per the FCA's welcome of the scheme launch

Open banking does not replace every rail. Direct debit remains strong for flat monthly amounts; cards still matter for prepay top-ups and channels where bank redirect is unfamiliar. The win is mixing rails by job: bank initiation where cost and confirmation speed matter, verification before you store any payment credential.

How does pay by bank work for one-off and variable utility bills?

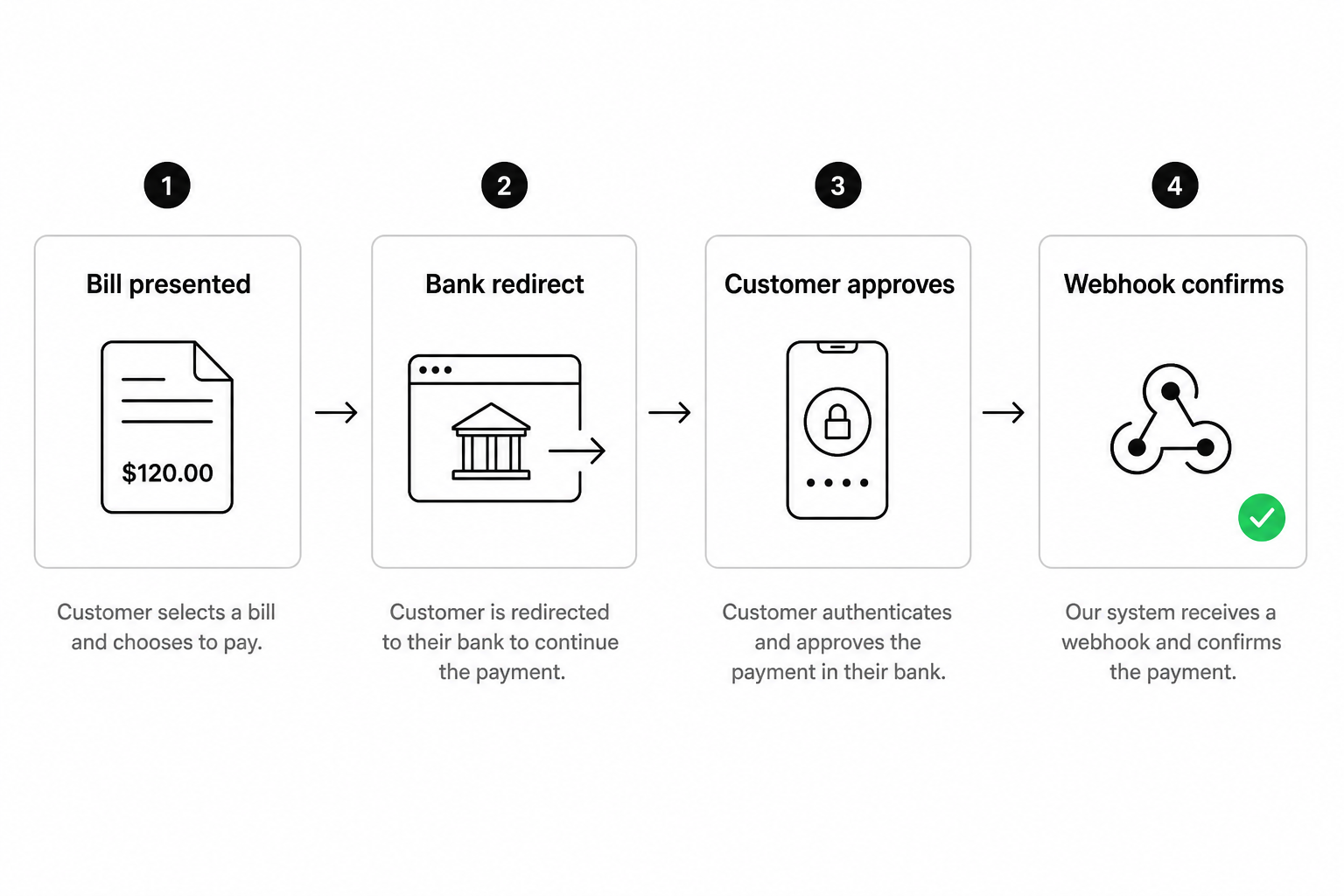

Pay by bank lets a customer authorise a specific bill amount from their banking app — you receive confirmation and reference data in seconds, often at lower cost than card. For utilities, the highest-value one-off flows are final bills at move-out, catch-up payments after failed collection, and first payments when a customer switches supplier.

A practical flow:

- Customer opens your portal or app and sees the amount due (usage-based or estimated)

- They choose pay by bank; your provider redirects to their bank with the amount and creditor reference

- Customer approves in the banking app; funds settle via account-to-account transfer

- Webhook confirms success; your billing system marks the invoice paid and stores the verified IBAN

Compared with card checkout, you avoid interchange on that transaction and reduce chargeback exposure because the customer authorises in their own bank. Compared with asking customers to set up a new direct debit for a single payment, pay by bank completes in one session.

Trade-offs: every one-off payment needs customer action in the bank app unless you hold a separate recurring mandate. For highly variable winter gas bills, many teams use pay by bank for exception payments and direct debit or bank-rail recurring for the normal cycle.

What recurring bank rails can replace card-on-file for utilities?

Recurring bank rails — SEPA Direct Debit, standing orders, or scheme-based variable recurring payments — cut card costs and expiry-driven churn when the bill amount changes predictably within agreed limits. Utilities with monthly estimates and quarterly true-ups need a rail that tolerates amount variation without re-keying card details.

| Rail | Best for | Main trade-off |

|---|---|---|

| SEPA Direct Debit | Stable or slowly changing monthly amounts | Mandate setup friction; chargeback windows under SDD rules |

| Pay by bank + stored verified IBAN | First payment + manual top-ups | Not automatic without a mandate or VRP consent |

| UK cVRP (UKPI Wave 1) | UK utilities and telecoms with variable recurring bills | Scheme eligibility and Wave 2 timing for broader retail |

| Card on file | Channels where bank redirect is unfamiliar | Interchange, expiry, dispute cost |

In the UK, Open Banking Limited describes UKPI as the first commercial open banking scheme; Wave 1 sectors include regulated utilities and telecoms. EU suppliers should map their own recurring strategy to bank on file vs card on file patterns and evaluate providers against recurring transaction criteria — coverage, consent UX, amount caps, and webhook granularity matter more than headline API pricing.

How do you verify accounts when customers switch supplier or move home?

Account verification at onboarding stops wrong-IBAN payouts, speeds up switching, and reduces fraud on final-bill credits. When a customer switches energy supplier or opens a new broadband account, they often type an IBAN from memory. Mismatch rates drive refund failures and ops tickets.

Open banking verification returns a bank-confirmed account holder name and IBAN match in one consent step. Billing teams use it to:

- Pre-fill direct debit or recurring mandate setup with a verified account

- Block payouts to accounts that do not match the named customer

- Shorten income or affordability checks for payment-plan offers without manual statement uploads

This mirrors patterns in open banking insurance use cases — verify first, then collect — but utilities add move-in/move-out timing: verification at switch-in prevents chasing the wrong account for a final credit months later.

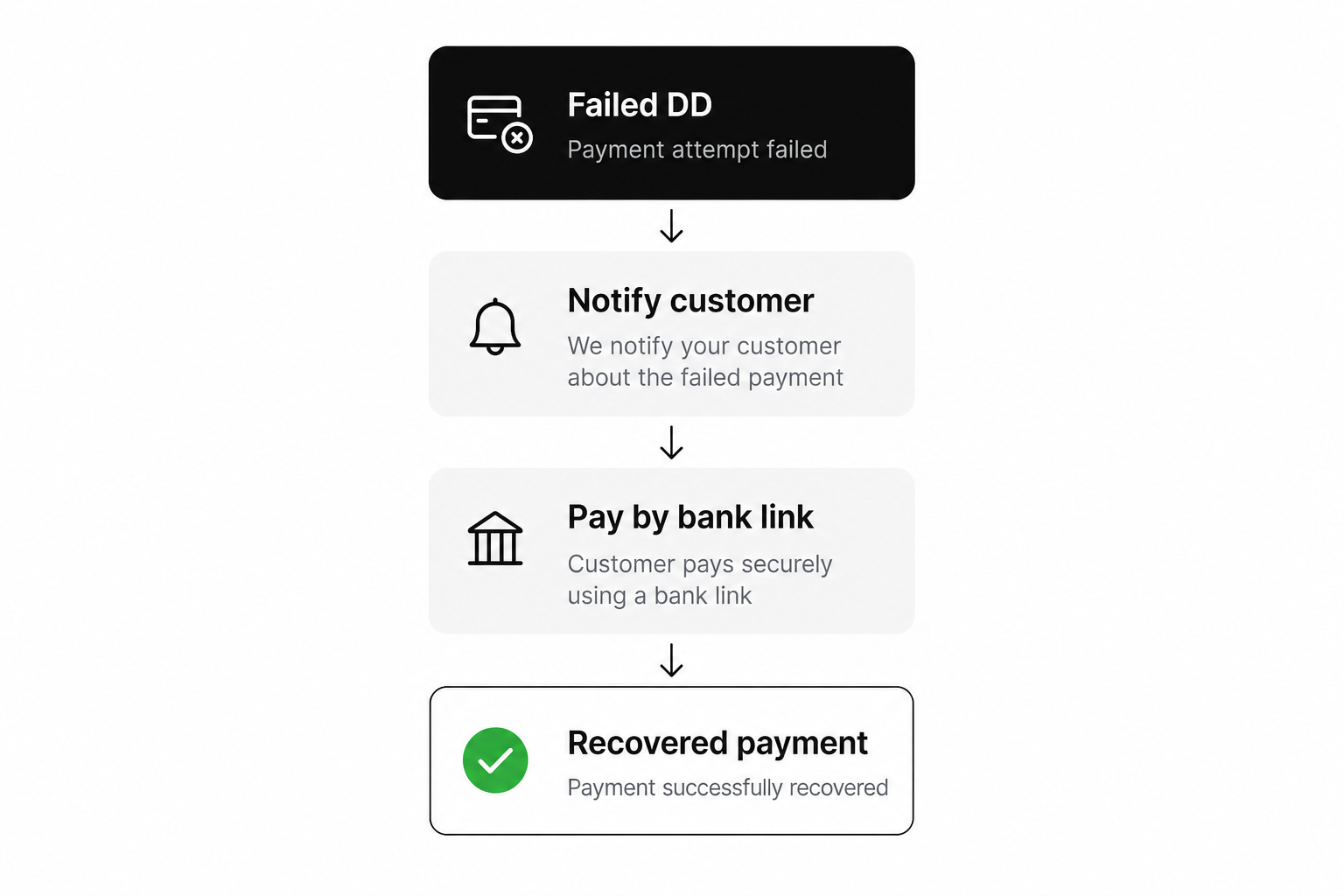

How can open banking reduce failed collections and dunning cost?

Failed collections often trace to expired cards, closed accounts, or insufficient balance on the retry date — open banking improves recovery by offering instant pay-by-bank links and verified retry paths. Dunning sequences that only offer "update your card" miss customers who prefer bank payment or whose failure was a timing issue, not willingness to pay.

Operational patterns that work:

- Smart retry link — SMS or email with a pay-by-bank deep link for the exact arrears amount

- Verified IBAN retry — after first successful bank payment, retry future failures against the same account where regulations allow

- Instant credit for overpayments — where outbound SEPA Instant Credit Transfer is supported, refund credits land same day instead of waiting for card reversal windows

Measure recovery rate and cost per successful collection, not just authorization rate on the first attempt. A rail that looks cheaper per call but fails more often on certain banks can increase dunning FTE.

What should utility billing teams evaluate in an open banking provider?

Shortlist providers on coverage in your billing countries, recurring consent support, webhook reliability, and reconciliation fields — not API marketing alone. Utility programmes span residential and SME accounts across many banks; a gap in one major ASPSP shows up as conversion loss on switcher campaigns.

Validation checklist before production:

| Criterion | Why it matters for utilities |

|---|---|

| Bank coverage per market | Switchers bank with national champions; gaps block completion |

| Variable amount / recurring consent | Seasonal bills need rails that accept changing amounts within caps |

| Creditor reference in webhook | Finance matches millions of rows; references must be deterministic |

| Sandbox parity | Test winter bill spikes and failure paths before marketing switch |

| Incident comms | Billing peaks (January gas, quarterly true-ups) cannot wait on opaque status pages |

Run sandbox tests with your statement descriptors and amount patterns. For a neutral comparison framework across vendors, see how to choose an open banking provider in the EU. When you are ready to match requirements to live coverage, use the provider-matching form to compare bank coverage, recurring support, and webhook quality against your billing markets — or start from the provider comparison guide for evaluation dimensions.

Frequently Asked Questions

What are open banking utility payments?

Open banking utility payments use regulated bank APIs so energy, water, gas, and telecom suppliers collect bills, verify customer accounts, and reconcile inbound funds through account-to-account transfers with customer consent in the banking app — instead of relying only on cards or manual bank transfers.

Can utilities use open banking for variable monthly bills?

Yes. Pay by bank handles one-off and variable amounts when the customer authorises each payment or when a recurring bank mandate (such as SEPA Direct Debit or UK commercial variable recurring payments where eligible) allows amount changes within agreed limits. Many suppliers combine verified first payment with a recurring rail for the normal billing cycle.

How does open banking compare to direct debit for utility billing?

Direct debit suits stable schedules and batch collection; open banking adds instant confirmation on ad-hoc payments, lower card interchange when used instead of card-on-file, and account verification before mandates are set. Most mature stacks use both — direct debit or VRP for the cycle, pay by bank for exceptions and switchers.

Is UKPI relevant for energy and telecom suppliers?

Yes, if you bill UK customers. The UK Payments Initiative launched in June 2026 with Wave 1 covering regulated utilities and telecoms for commercial variable recurring payments, as confirmed by the FCA. Broader e-commerce and subscription retail scopes are expected in later waves — check scheme rules before assuming eligibility.

Do open banking utility payments work across the EU?

Pay by bank and account verification work in EU markets where your provider has bank coverage and the customer’s bank supports initiation. Recurring rules differ by country and scheme; there is no single EU equivalent to UKPI yet. Pilot in your top two billing countries before rolling out a group-wide switch campaign.

How do I choose a provider for utility bill payments?

Compare bank coverage in each billing country, support for your recurring model (fixed vs variable), webhook fields for reconciliation, sandbox quality, and incident response — then run production-shaped tests on switcher and dunning flows. Use a structured shortlist process rather than picking on price alone.

Conclusion

Open banking utility payments address real billing economics: lower cost on inbound collection, faster recovery when direct debits fail, verified accounts at switch-in, and — in the UK — a path to variable recurring bank rails under UKPI. The implementation lesson from other vertical playbooks is the same: match the rail to the job, measure recovery and reconciliation time, and validate sandbox behaviour before peak season. When your checklist is clear, compare providers on coverage and ops fit for your markets.

Related articles

- Open Banking for Payroll: Disbursement & Verification

Payroll platforms lose trust when salaries land late or on the wrong account. Open banking for payroll providers connects verification and disbursement to regu…

- Open Banking for Online Casinos: EU Deposits & Compliance

Licensed online casino operators lose players when deposits fail at the card gateway and when withdrawals sit in manual review. Open banking casino flows — pay…

- Open Banking for Marketplaces: 8 Use Cases for EU Platforms

Two-sided platforms live on money moving twice: collect from buyers, hold or route platform fees, pay sellers on time. Cards work until interchange, chargeback…