Open Banking Insurance Use Cases: 8 Examples for EU Insurers

European insurers sit on one of the most payment-heavy operations in financial services — recurring premiums, irregular claims payouts, refunds, broker commissions, and reinsurance flows — yet most of those movements still run on cards or direct debits that were designed before the regulated open banking framework existed. Open banking insurance use cases are not theoretical anymore: under PSD2 (Payment Services Directive 2), licensed TPPs (Third Party Providers) can initiate payments and read account data with explicit customer consent, and insurers across the EU are already running this in production. This article walks through eight use cases that European insurance carriers, MGAs, and brokers are deploying today, plus the regulatory context, trade-offs, and the operational signals that decide whether each one fits your book.

Open banking for insurance: The use of regulated APIs — covering PIS (Payment Initiation Service) and AIS (Account Information Service) — by insurers, brokers, and insurtechs to move money in and out of policyholder bank accounts and to access account data for underwriting, verification, and risk decisions, with explicit customer consent under PSD2.

Why open banking matters for insurance specifically

Insurance economics are dominated by two things card and direct debit rails handle badly: irregular high-value outbound payments (claims) and recurring inbound payments where failure costs you the customer (premiums). Open banking changes the unit economics on both sides — payment initiation is typically a single-digit-cent fee versus interchange on cards, and account information lets you verify income, ownership, and risk in seconds instead of asking the customer to upload bank statements.

The European Insurance and Occupational Pensions Authority (EIOPA) has flagged open finance as a priority for the insurance sector, and the upcoming Financial Data Access (FIDA) regulation will extend the open banking model to a much wider set of financial data — including, in time, insurance product data itself.

A few patterns to keep in mind as you read the use cases below:

- PIS is for moving money; AIS is for reading data. Most insurance use cases combine both.

- SCA (Strong Customer Authentication) is required on every initiated payment and on every fresh account data consent, with the now-standard 180-day re-consent rule for ongoing AIS.

- You don't need to be a licensed TPP yourself. Most insurers integrate through a regulated open banking provider that holds the AISP/PISP licence on their behalf.

1. Pay by Bank for premium collection

The most adopted open banking insurance use case is replacing or supplementing card and SEPA Direct Debit on the inbound side. Instead of asking the customer to type a card number at policy purchase, the insurer initiates an account-to-account payment that the customer authorises in their own banking app via SCA.

The benefit pattern is consistent across motor, home, travel, and SME lines:

- Lower cost per transaction versus card interchange, especially on high-value annual premiums

- Higher first-payment success rate versus stored cards that expire or get blocked

- Reduced chargeback exposure because account-to-account payments are pull-authorised, not card-disputed

- Cleaner reconciliation — the IBAN and reference come back deterministically

The trade-off is that one-off Pay by Bank still requires the customer to authorise in their bank app every time, so for monthly premiums most insurers combine open banking for the first payment (and any change of payment method) with SEPA Direct Debit for the recurring schedule, using the verified IBAN from the open banking flow to set up the mandate.

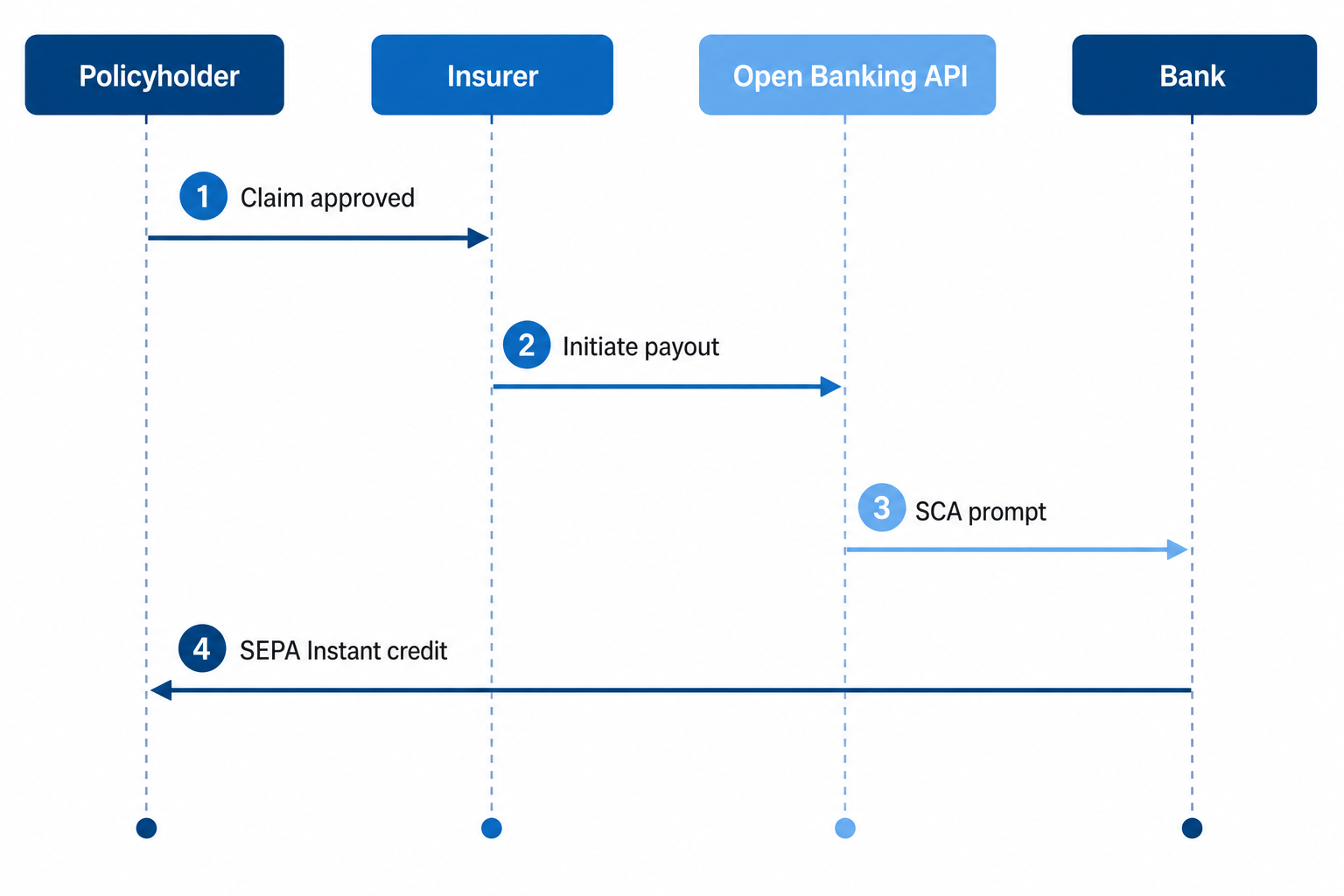

2. Instant claims payouts via payment initiation

On the outbound side, the highest-impact use case is paying claims into the policyholder's bank account in seconds rather than days. Traditionally insurers send a card refund, a cheque, or a SEPA Credit Transfer that takes one business day; with payment initiation against a verified IBAN, the funds can land within seconds where the receiving bank supports SEPA Instant Credit Transfer.

The customer experience advantage is significant — claim NPS is one of the few moments an insurer can decisively beat its competitors — and the operational case is real too:

- No bounced payouts from outdated card details

- No cheque issuance or postage cost

- Cryptographic proof of who authorised the receiving account

- Audit trail tied to the same identity used at policy inception

This use case works best for low- and mid-value claims (travel medical reimbursements, contents claims, small motor repairs, gadget replacements) where instant settlement removes a friction point. For complex bodily injury or property claims with multiple beneficiaries, the bottleneck is adjudication, not the payment rail.

3. Income and affordability verification for life and protection underwriting

Income evidence is one of the slowest steps in life, income protection, and critical illness underwriting. The traditional path — payslips or accountant letters — adds days and a meaningful drop-off in application completion. AIS pulls categorised salary and self-employment income directly from the applicant's accounts with their consent, typically over a 12- to 24-month lookback.

For underwriters the value is structured, source-verified data:

- Confirmed employer name and consistent net salary pattern

- Self-employed revenue and seasonal volatility

- Existing financial commitments visible as outgoing payments

- A real income figure rather than a self-declared one

This is also a fraud control. Self-reported income is one of the most common application misrepresentations across European life markets, and source-of-funds verification at policy inception reduces both adverse selection and post-claim disputes.

4. Account verification at policy purchase

Before either of the payment use cases above can work cleanly, the insurer needs to know the bank account belongs to the policyholder. Open banking account verification (sometimes called Confirmation of Payee, though the UK and EU implementations differ) returns a verified account holder name and IBAN match in a single SCA-authenticated step.

This kills three problems at once:

- Application fraud — using someone else's account details for payouts

- Wrong-IBAN refunds — a top operations cost for any high-volume insurer

- AML smurfing — multiple policies funded from the same source account

It also unblocks the next use case: once you have a verified account, you can layer in source-of-funds analysis without asking the customer for another document.

5. KYC and AML — source of funds, source of wealth

For life, single-premium investment products, and high-value commercial lines, insurers are obligated under the EU Anti-Money Laundering directives to evidence source of funds and, for higher-risk customers, source of wealth. AIS-backed transaction history gives compliance teams an evidenced view that is harder to fake than a self-declared form and faster to review than a stack of statements.

Done well, this looks like:

| Compliance signal | Traditional method | Open banking method |

|---|---|---|

| Identity confirmation | Document upload + selfie | Bank-verified account holder name |

| Source of premium funds | Manual statement review | Categorised inbound transactions |

| Account ownership | IBAN typed by customer | API-confirmed account match |

| Wealth pattern | Customer-supplied | 12–24 month aggregated income |

The compliance team still owns the decision — open banking just gives them better evidence faster.

6. SME and commercial underwriting from cash flow data

For commercial lines — business interruption, cyber, credit insurance, surety, embedded SME products — the underwriter cares about the financial health of the insured business. Filed accounts are often a year out of date and reveal little about current cash position. AIS access to the business's operating accounts, with explicit director consent, gives underwriters a near-real-time view of:

- Turnover trend over the last 12–24 months

- Cash on hand and average end-of-month balance

- Concentration risk in receivables

- Recurring obligations that signal operational fragility

This is particularly valuable for embedded SME insurance distributed through accounting software or banking platforms, where the underwriting signal is already available and the customer has already authorised it for another purpose. Pricing models can shift from sparse application data to continuous portfolio monitoring of risks already on the book.

7. Refund and reimbursement automation

Insurers process a surprising volume of small refunds — overpaid premiums, mid-term cancellations, double payments, broker chargebacks. The legacy path either reverses the original card transaction (subject to scheme rules and chargeback timing limits) or sends a SEPA Credit Transfer based on a customer-typed IBAN, with the usual error rate.

Payment initiation against a pre-verified account turns this into a one-click operation. The cost saving is small per transaction but compounds — refund handling is a meaningful slice of contact-centre volume for any retail insurer, and most of it is preventable.

8. Premium financing and affordability decisioning

Premium financing — letting a customer pay an annual premium in monthly instalments via a credit line — is competitive and tightly regulated for affordability. Open banking AIS gives the financing arm (whether the insurer itself, a captive financier, or a third party) a real-time affordability check at the point of sale: confirmed income, existing commitments, and balance volatility.

The downstream effect is fewer declined applications among genuinely affordable customers, fewer arrears on accepted ones, and a defensible audit trail when the regulator asks how the affordability decision was made. For insurers expanding into instalment-pay segments — especially for SME, motor fleet, and high-value home — this is increasingly table stakes.

How to choose which use cases to start with

Most insurers don't deploy all eight at once. The sequencing that works tends to be:

- Start with account verification. It's the lowest-risk, lowest-integration use case and it unlocks everything else.

- Layer Pay by Bank on top for new business premiums, where the conversion lift is measurable and the failure mode is just a fallback to card.

- Add instant claims payouts for low-value, high-frequency claim types where NPS uplift is visible.

- Then introduce AIS-backed underwriting and KYC where the legal team has had time to sign off the consent architecture.

The integration choice matters as much as the use case choice. A single regulated open banking provider with broad EU bank coverage, support for both PIS and AIS, and an SLA on bank API uptime is usually easier to operate than stitching together specialist vendors per use case.

See also: /blog/open-banking-psd2-explained and /blog/pay-by-bank-vs-cards-for-checkout.

Frequently Asked Questions

What is open banking in the insurance industry?

Open banking in insurance is the use of regulated PSD2 APIs by insurers, brokers, and insurtechs to initiate payments to and from policyholder bank accounts and to access account information with the customer's explicit consent. It covers premium collection, claims payouts, account verification, underwriting data, and KYC evidence. The insurer either holds a TPP licence itself or integrates through a licensed open banking provider.

Is open banking legal for insurers to use in the EU?

Yes. PSD2 came into force across the EU in 2018 and explicitly permits regulated third parties — and any company integrating with one — to initiate payments and access account data with customer consent. Insurers are regulated under Solvency II and the IDD, but using open banking services for the use cases described above does not require a payment institution licence as long as you partner with a licensed AISP or PISP.

What is the difference between AIS and PIS for insurance use cases?

AIS (Account Information Service) lets the insurer read account data — balances, transactions, account holder name — with customer consent, and is used for underwriting, KYC, income verification, and account ownership checks. PIS (Payment Initiation Service) lets the insurer initiate a payment from the customer's account, and is used for premium collection and outbound claims payouts. Most insurance use cases combine both — for example, verifying the account via AIS and then collecting the premium via PIS.

How is open banking different from SEPA Direct Debit for premium collection?

SEPA Direct Debit is a pull mechanism authorised once by a signed mandate, with bounce risk and a refund window of up to eight weeks for authorised payments. Open banking payment initiation is a push payment authorised by the customer in their bank app at the moment of payment, with no chargeback right once authorised and immediate confirmation of success. Many insurers use open banking for the first premium and to verify the IBAN, then continue recurring collection on SEPA Direct Debit.

Will FIDA replace PSD2 for insurance open banking?

No — FIDA (Financial Data Access) extends the open finance framework beyond bank accounts to a wider set of financial products, including insurance product data, pensions, and savings. PSD2 (and its successor PSD3) continues to govern payment initiation and bank account information access. For insurers, FIDA is more likely to affect how their own policy and claims data is shared with third parties than to change how they consume open banking services.

How do I evaluate open banking providers for insurance use cases?

Look for: full PSD2 licensing (AISP and PISP) in your operating markets, breadth and uptime of bank API coverage across the EU, support for SEPA Instant Credit Transfer on payouts, account verification with name match, transaction categorisation suitable for income and KYC use cases, and a contractual SLA. Compliance, data residency in the EU, and a clean ISO 27001 / SOC 2 posture matter for any insurer's vendor due diligence.

Closing thought

Open banking isn't a single product for insurers — it's a set of building blocks that map directly onto the existing pain points in premium collection, claims handling, underwriting, and compliance. The carriers winning with it tend to start narrow, measure rigorously, and expand once the operational pattern is proven. Every insurance book is different — matching depends on your markets, volumes, and which use cases you prioritise first.

Related articles

- Open Banking Utility Payments: How Suppliers Collect Bills

Utility billing teams lose margin on three predictable leaks: card interchange on high-volume inbound payments, failed direct debits that trigger dunning and c…

- Open Banking for Online Casinos: EU Deposits & Compliance

Licensed online casino operators lose players when deposits fail at the card gateway and when withdrawals sit in manual review. Open banking casino flows — pay…

- Open Banking for Payroll: Disbursement & Verification

Payroll platforms lose trust when salaries land late or on the wrong account. Open banking for payroll providers connects verification and disbursement to regu…