cVRP Explained: Commercial Variable Recurring Payments

cVRP stands for Commercial Variable Recurring Payments — a UK way to collect repeat payments straight from a customer’s bank account after they approve once in their banking app. Think of it as standing permission to pull money when a bill is due, within limits the customer sets, without sending them back to checkout every month.

It went live in the UK in June 2026 under UKPI (UK Payments Initiative), backed by major banks and payment firms. If you bill customers on a cycle — utilities, insurance, council tax, donations, loan repayments — and you have only used Direct Debit or cards until now, this is the bank-rail option to understand. (In logistics, cVRP means vehicle routing — different topic entirely.)

cVRP (Commercial Variable Recurring Payments): Your business collects repeat payments from a UK customer’s bank account after one approval in their banking app. Each charge can be a different amount, as long as it stays within caps the customer agreed. It pays you — it does not move money between the customer’s own accounts.

What is cVRP, in plain English?

Your customer opens their bank app, confirms who you are and how much you are allowed to take (per payment and per month), and authorises future pulls. After that, when a bill is due, your payment provider requests the amount from their bank. If it succeeds, the money reaches you on Faster Payments — typically within seconds.

You do not store their card number. You do not send them a new checkout link every month. The permission lives at their bank until they revoke it or you hit the agreed limits.

That is the whole idea: repeat bank collections with one upfront consent, built for businesses that invoice or bill on a cycle.

Why does cVRP exist?

UK open banking could already move money between a customer’s own accounts automatically — savings sweeps, that kind of thing. What was missing was the same mechanic for paying a company: your energy supplier, your council, your insurer.

Direct Debit solved recurring collection decades ago and still works at massive scale. Cards on file solved it for online businesses. But both come with trade-offs:

- Direct Debit can take days to settle, and you often find out a payment failed days after you tried.

- Cards charge interchange, cards expire, and chargebacks eat ops time.

cVRP uses open banking so the customer authorises you in their bank app, you can check if they have enough money before you pull, and successful payments land fast. UK industry built UKPI to run it properly — with rules on who can use it, how disputes work, and how banks get paid.

It exists to give UK billers a modern bank rail for recurring revenue, not to delete Direct Debit overnight.

What issues does cVRP solve for your business?

These are the practical reasons finance and product teams care about — not marketing fluff.

You get paid faster. Direct Debit runs on Bacs. Even when a collection works, cash can take two or three working days to arrive. cVRP runs on Faster Payments. Success usually means money moving the same day, often in seconds. That matters when you are forecasting cash or funding working capital off monthly billing.

You see failures earlier. With Direct Debit, insufficient funds often surface only when return reports land days later — then collections chases the customer. cVRP can ask the bank “is there enough in the account?” before attempting the pull. If not, you do not fire a payment that was doomed to fail. Fewer blind failures, less arrears admin. (Balance checks depend on your provider and bank — they are not guaranteed on every flow.)

You bill the real amount with less paperwork. If your invoice changes every month — meter readings, usage, premiums — cVRP pulls the actual figure within the customer’s agreed caps. Direct Debit can do variable amounts too, but often with amendment notices and back-office steps. cVRP is designed for “this month’s bill is £143.27” without a separate customer action.

You can onboard new customers on bank rails. Someone signing up today can approve you in their banking app instead of completing a full Direct Debit mandate journey or handing over a card — useful when you want bank pay from day one.

You avoid card-specific pain on flows you move. Cards already handle different amounts each month. What hurts is interchange on every payment, cards expiring and breaking renewals, and dispute handling. cVRP is account-to-account: no card on file, no expiry date.

How could your business use cVRP?

Whether you can adopt it today depends on your sector (see Wave 1 below). These are the patterns UK providers highlight:

| Your business | Typical use | What cVRP gives you |

|---|---|---|

| Energy, water, gas, broadband, mobile | Monthly usage bills | Collect what the customer actually owes; cash in faster than Bacs; fewer failed pulls when balances are checked first |

| Insurance | Premiums that change with risk or usage | Pull the right amount within agreed limits when the policy adjusts |

| Mortgages, pensions, savings, investments | Regular or top-up contributions | Instant settlement on repayments or contributions |

| Council, government agency, public body | Tax, fines, fees, instalment plans | Bank-authorised payments without storing card details |

| Charity | Recurring donations | Lower collection cost than cards on some flows; donors manage giving in their banking app |

| Rail and travel operators | Season tickets, fare capping | Account-to-account settlement for caps and renewals |

If you run a general online shop, SaaS product, or streaming service, you are probably in the Wave 2 queue — expected later in 2026 — not Wave 1.

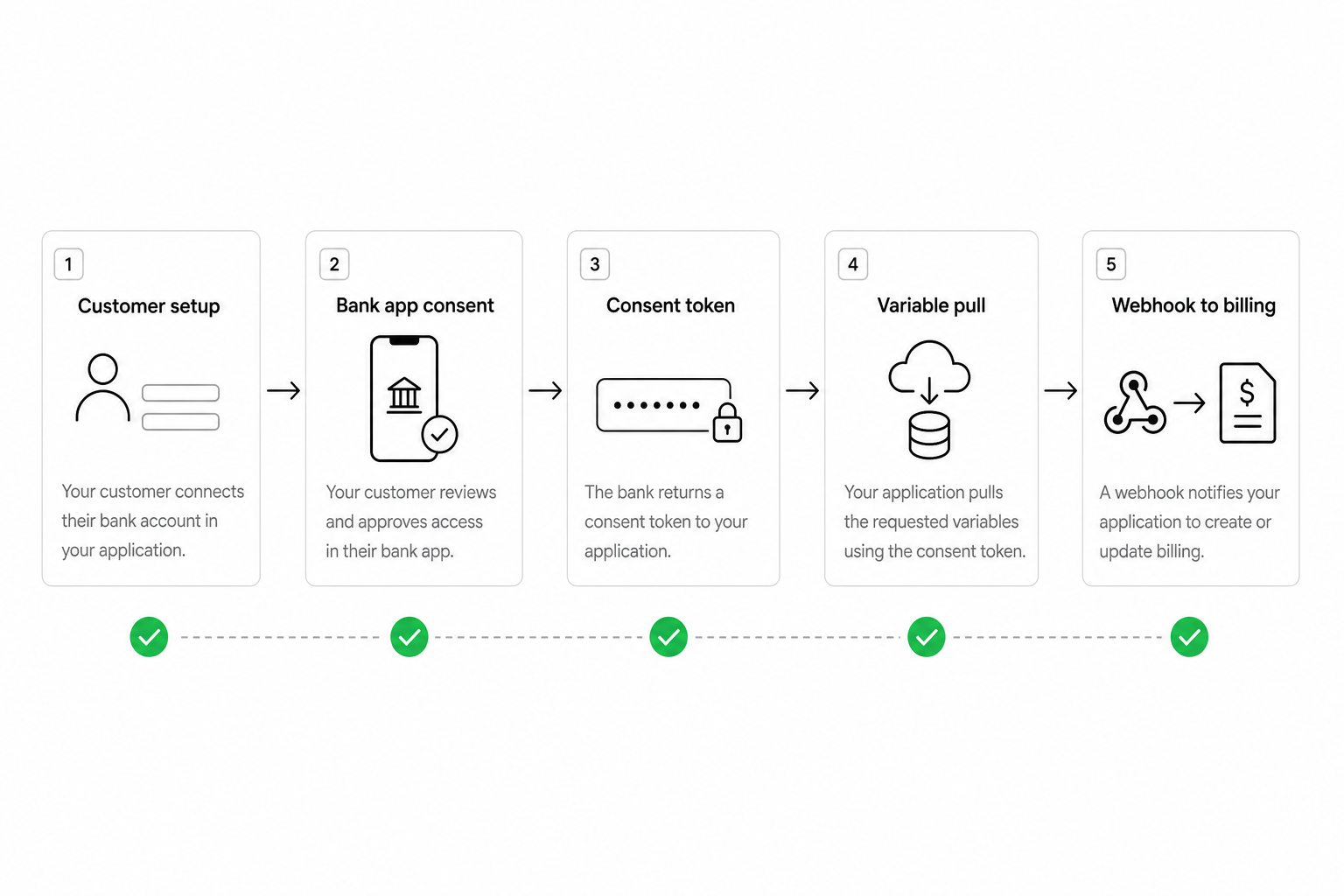

How cVRP works, step by step

- Customer starts — from your website, app, or billing portal.

- They log into their bank — mobile or online banking.

- They approve you — maximum per payment, monthly cap, how long the permission lasts.

- Your provider stores that approval — you integrate via a licensed payment partner; you do not wire every bank yourself.

- Billing runs — you request a pull for this period’s amount, within the caps.

- Optional balance check — your provider asks the bank if funds are available.

- Payment executes — on success, Faster Payments moves the money and your system gets a clear result.

The customer does not approve each individual charge. They approved the framework once. They can still open their banking app and cancel permission anytime.

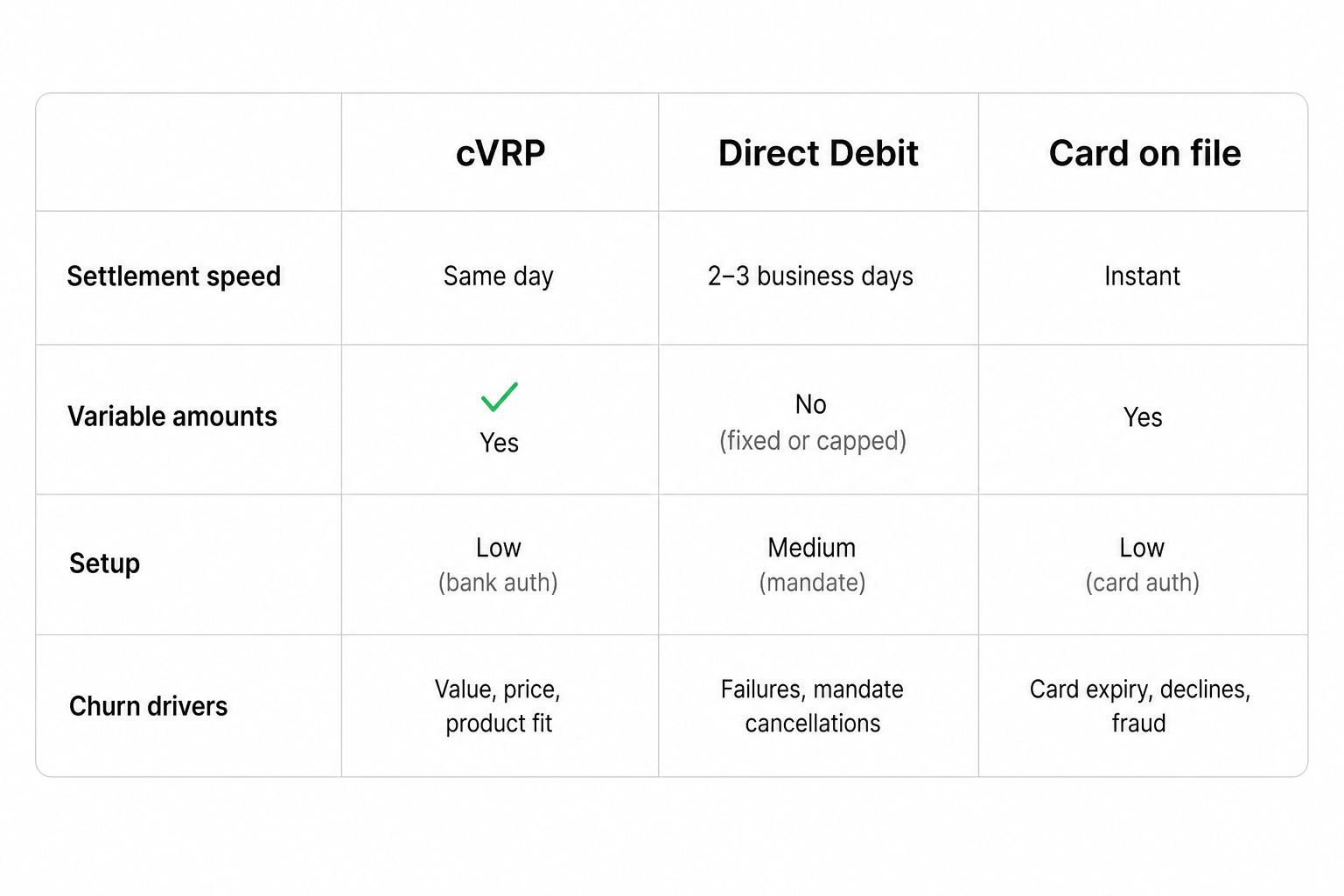

cVRP vs Direct Debit

Most UK billers know Direct Debit. Here is how cVRP differs in practice.

| cVRP | Direct Debit | |

|---|---|---|

| How the customer signs up | Approves in banking app | Mandate (paper or digital) |

| When money arrives | Usually seconds | Often 2–3+ working days |

| When you learn it failed | Often before or at the attempt | Often days later via Bacs returns |

| Variable monthly amounts | Built for pulls within consent caps | Supported, often with amendment admin |

| Cost at scale | New scheme — pricing varies | Very low per payment at volume |

| Coverage | Growing; not every bank yet | Universal UK mandate reach |

Direct Debit is still the backbone for millions of UK mandates. cVRP fits where speed, earlier failure visibility, or a smoother bank signup matter — often alongside DD, not instead of the whole book. Many payment platforms route automatically: cVRP when the customer and bank support it, Direct Debit when they do not.

cVRP vs card on file

| cVRP | Card on file | |

|---|---|---|

| Variable amounts | Yes, within caps | Yes — cards already do this |

| Customer signup | Bank app approval | Card number or wallet |

| What breaks renewals | Consent cancelled, account closed | Expired or replaced cards |

| Fees | Bank-rail pricing | Interchange and scheme fees |

| Disputes | Bank and scheme rules | Chargebacks |

| Customer habit | Growing with pay-by-bank | Deeply familiar |

cVRP is not “variable billing invented.” Cards already charge different amounts. The case for cVRP vs cards is cost, renewal reliability, and bank-authorised payments in sectors that prefer not to store card details — traded against conversion, because some customers still reach for a card field faster than a bank redirect.

More on stored payment methods: bank on file vs card on file.

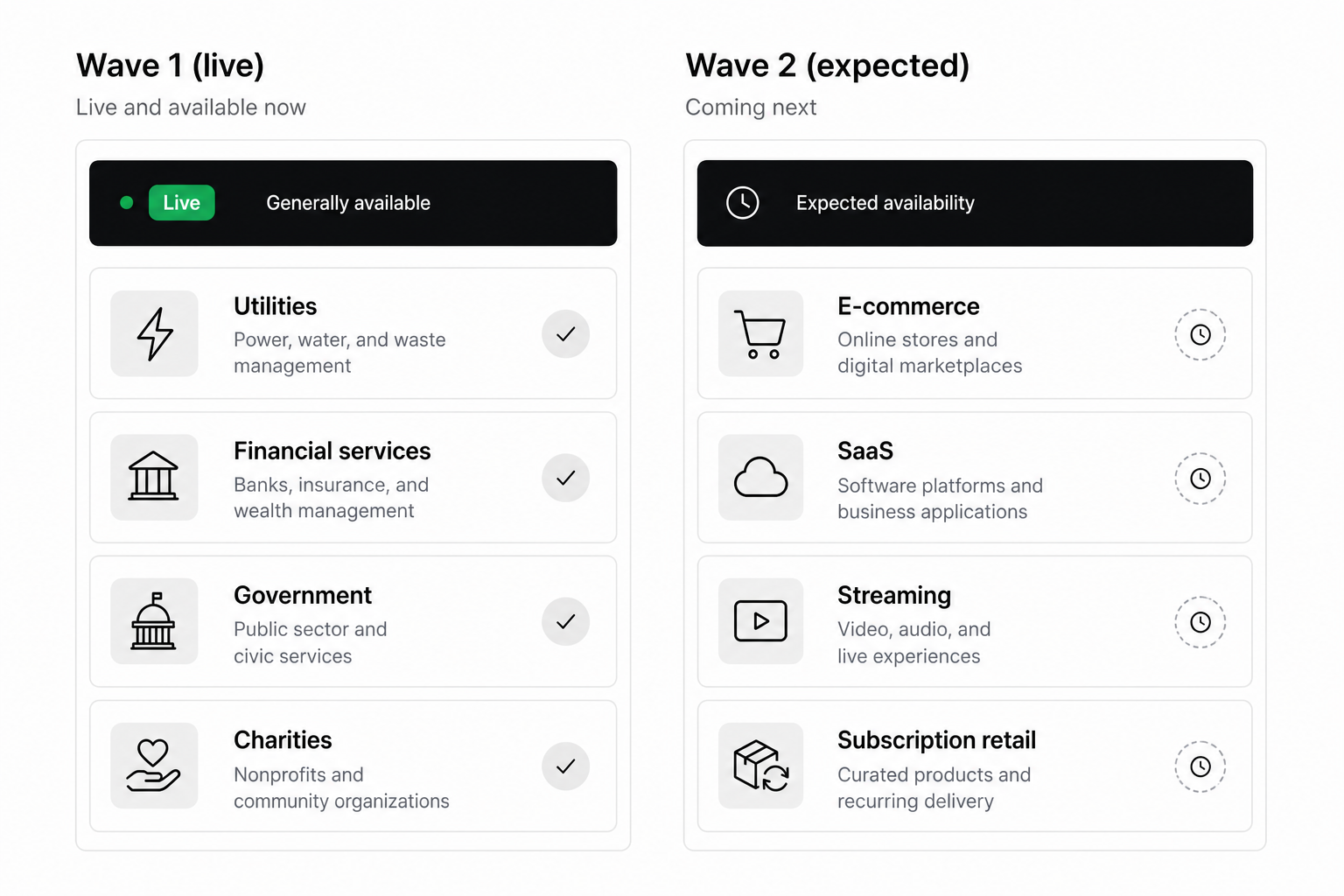

Can your business use cVRP today? Wave 1 vs Wave 2

UKPI rolled out in phases. Sector rules matter as much as technology.

Wave 1 (live from June 2026) includes:

- Regulated utilities and telecoms (energy, water, gas, broadband, mobile)

- Regulated financial services and e-money

- Local and central government

- Registered charities

- Rail-related use cases in scheme materials

Wave 2 (expected late 2026) should broaden to general e-commerce, SaaS, streaming, and subscription retail.

| Question | Wave 1 | Wave 2 |

|---|---|---|

| Can I use cVRP now? | Yes, if your sector is in scope | Not yet |

| Who is waiting? | General online retail, SaaS, BNPL, most B2B trade | — |

If you are a utility, insurer, council, charity, or financial services firm billing UK customers, check whether your use case fits Wave 1. If you are a SaaS startup, plan ahead — build consent flows and talk to providers, but scheme eligibility may not be open yet.

cVRP vs “sweeping” — a common confusion

Banks talk about VRP in two ways. Sweeping moves money between a customer’s own accounts. Commercial VRP (cVRP) pays your business. If a provider says “VRP enabled,” ask which one they mean. You need commercial collection for billing. Deeper background: variable recurring payments.

How to get started

You integrate through a payment provider — GoCardless, Modulr, TrueLayer, and others participate in UKPI. You rarely connect to each bank yourself.

Before you commit, test on the banks your customers actually use:

- Commercial cVRP for your sector (not sweeping-only)

- A real bank list for retail vs business accounts

- Direct Debit fallback when cVRP is not available

- Balance check before pull, if that matters to you

- Clear success and failure signals for your billing system

- What happens when the customer revokes consent in the bank app

Run one pilot: one bank, one product, one billing path in sandbox. Then compare providers on the same test — see how to shortlist open banking providers and recurring payment criteria.

Frequently Asked Questions

What does cVRP stand for?

Commercial Variable Recurring Payments — repeat collections from a customer’s UK bank account after they approve once in their banking app, with each payment able to vary within limits they set.

What is cVRP in open banking?

It is a UK payment scheme (UKPI) that lets licensed providers initiate repeat bank pulls on your behalf after customer consent. It uses open-banking APIs and settles on Faster Payments.

Who can use cVRP in the UK?

Wave 1 (from June 2026) covers regulated utilities and telecoms, financial services, e-money, government, and charities. Wave 2 is expected to add broader e-commerce and subscriptions. Your sector must fit the scheme rules — not just your tech stack.

How is cVRP different from Direct Debit?

Direct Debit settles over working days and often reports failures days after the attempt. cVRP typically settles in seconds and can check account balance before pulling. Direct Debit remains cheaper at scale for large existing mandate books. Many businesses use both.

How is cVRP different from card on file?

Cards already support variable amounts. cVRP differs on fees, card expiry churn, and dispute handling — customers authorise in their bank app instead of giving you a card number. Conversion trade-offs apply.

What problems does cVRP solve?

Faster settlement, earlier visibility on failed collections, bank-authorised repeat billing without storing cards, and smoother handling of changing monthly amounts — not “variable billing” as a new concept.

How do I choose a cVRP provider?

Shortlist partners with commercial VRP for your Wave sector, a published UK bank list, Direct Debit fallback, and billing webhooks you can operate. Prove it in sandbox on your top customer banks before you go live.

Summary

cVRP is Commercial Variable Recurring Payments — standing bank-app consent so your business can collect repeat charges from UK customers, with money landing fast and optional balance checks before each pull. It exists because billers wanted a modern bank rail next to Direct Debit and cards: quicker cash, fewer late failure surprises, and bank-held permission customers can see and control.

Check Wave 1 eligibility for your sector, understand how it compares to Direct Debit and cards for your specific pain points, pilot with a provider on real banks, and scale what works. That is the path from “what is cVRP?” to using it in your business.

Related articles

- Bank on File vs Card on File: EU & UK Recurring Billing

Recurring revenue depends on a stored funding method you can charge again without asking the customer to re-enter details every cycle. Card on file is the defa…

- Variable Recurring Payments (VRP) for EU and UK Teams

Subscription and usage billing breaks when every renewal needs a new card authorisation or a fixed direct debit that cannot match the invoice. Variable recurri…

- Best Open Banking Providers for Recurring Transactions

Recurring revenue breaks when collection depends on the wrong rail for the country you are billing in. A provider strong for one-off Pay by Bank in Germany is…