Pay by Bank Explained: How It Works in the EU and UK

Pay by bank is a checkout and payment method where the customer authorises money to move directly from their bank account to yours — usually by logging into their banking app, confirming the amount, and approving the transfer in one session. There is no card number on your page. The payment runs on account-to-account rails, often powered by open banking APIs with the customer’s consent. Businesses offer it to reduce card fees on eligible flows, get faster confirmation on many EU transfers, and lower certain types of payment fraud and chargebacks.

Pay by bank: A payment method where the customer pays from their bank account by authorising a transfer in their banking app (or online banking), instead of entering card details — typically implemented through regulated open banking payment initiation with explicit consent.

What is pay by bank?

Pay by bank is checkout and billing where the customer approves an account-to-account payment in their banking app — no card number on your site. Businesses add it to cut card fees on eligible flows, improve reconciliation, and get strong payer authentication on the bank’s rails. It is usually delivered through a licensed payment initiation provider, not a direct contract with every bank.

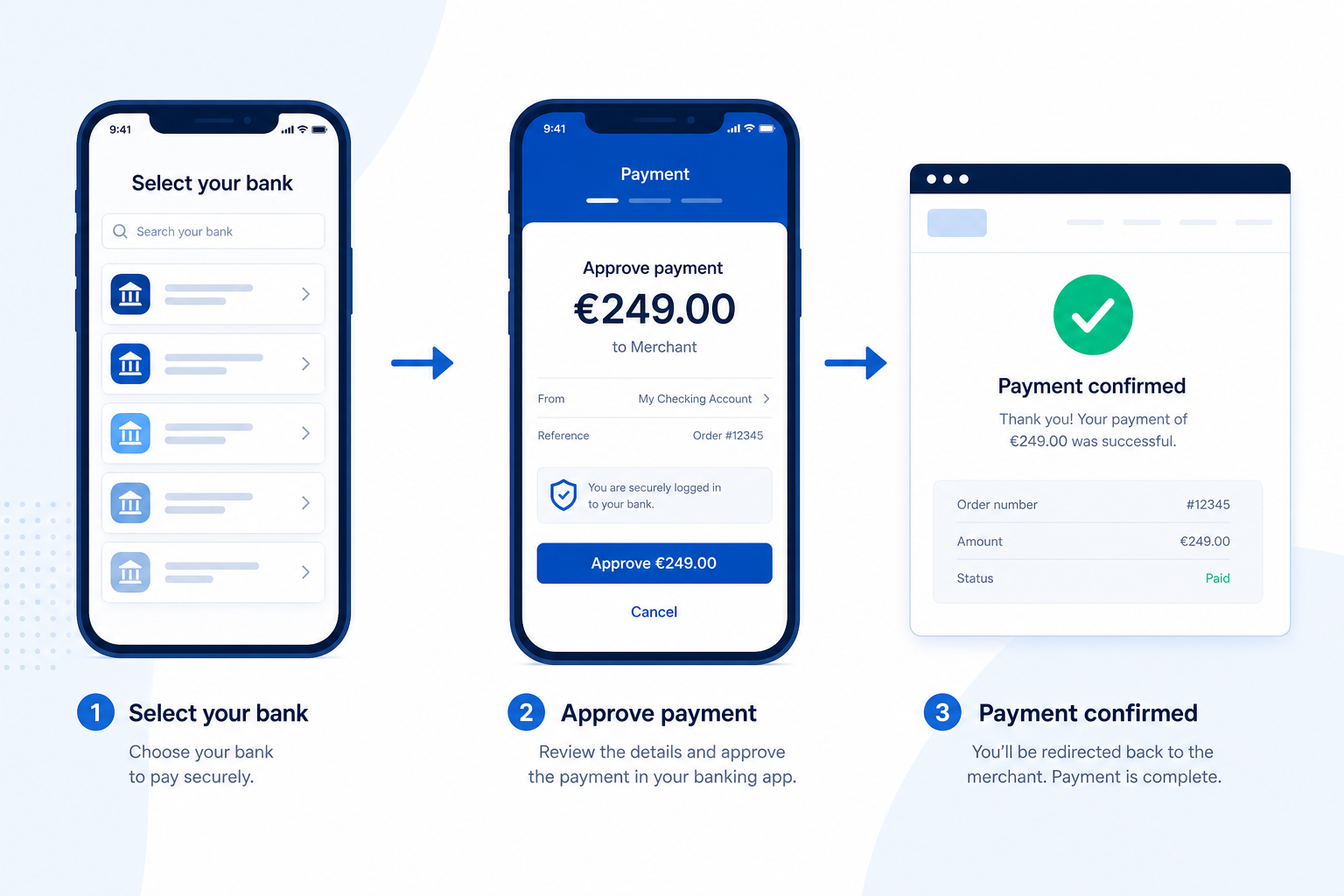

How pay by bank works (step by step)

Pay by bank feels like “choose your bank → approve → done.” Behind that is a regulated payment initiation flow.

- Customer chooses pay by bank at checkout, on an invoice, or in your app.

- They select their bank from a list (coverage depends on your provider and country).

- Redirect or app switch — they authenticate in the mobile banking app or online banking (strong customer authentication is handled by the bank).

- They review and confirm the amount, payee name, and reference shown on the bank screen.

- Payment status returns to you — success, pending, failed, or cancelled — via API and usually a webhook.

- You fulfil the order or release the service according to your risk rules and when funds are confirmed.

The customer never types card details on your site. You integrate a licensed payment initiation provider that connects to banks (ASPSPs) on your behalf — you do not need a direct contract with every bank. For how those roles fit together, see ASPSP definition.

What businesses gain from pay by bank

Merchants, platforms, and billers add pay by bank when the economics or operations of card rails hurt more than the UX cost of a bank redirect.

Lower cost per successful payment — On many EU account-to-account flows, variable fees are lower than card interchange on comparable ticket sizes, especially for B2B and high-value baskets.

Fewer card-style chargebacks — Disputes behave differently on bank rails; you still need clear refunds and customer service, but the chargeback profile is not identical to card networks.

Strong payer authentication — The customer approves in the bank app, which reduces certain fraud types tied to stolen card numbers on your checkout page.

Clearer reconciliation — Bank transfers can carry references and payer IBAN data your finance team can match to orders or invoices.

Verified account for later — The same flow can confirm which account paid, useful before recurring collection or B2B onboarding.

Trade-offs are real: some customers prefer cards for habit or loyalty points; bank redirects can drop off on desktop or if the wrong banks are listed; not every country or bank supports the same experience. Most teams run pay by bank alongside cards, not as a forced replacement on day one. For conversion benchmarks and UX levers, see pay by bank checkout conversion.

Pay by bank vs cards, wallets, and manual transfer

| Method | Customer experience | Typical business trade-off |

|---|---|---|

| Pay by bank | Bank app approval, no card on your site | Lower fees on eligible flows; redirect UX |

| Card | Familiar, fast on mobile wallets | Interchange, chargebacks, expiry |

| Manual bank transfer | Customer copies IBAN offline | Cheap but slow; poor conversion |

| Digital wallet | One-click if already enrolled | Scheme fees; not always available |

For a full comparison of fees, settlement, chargebacks, and conversion, see pay by bank vs cards at checkout. This article stays on what pay by bank is; that post helps you decide when to prefer it.

Where pay by bank is common in Europe

Pay by bank adoption is strongest where open banking coverage and mobile banking are mature — notably the UK, Germany, the Nordics, and growing use in France, Netherlands, and Spain. Checkout, invoicing, marketplaces, lending, insurance, and open banking for e-commerce teams ship it in production; SaaS billing uses it for first payment before direct debit mandates.

Coverage is always per bank and per country. A provider’s “EU support” label is not enough — validate the banks your customers actually use. Developers should request institution lists filtered by payment initiation, not headline maps alone (open banking API providers for developers).

Settlement speed varies: standard SEPA credit transfer may take longer than SEPA Instant where both banks support it. Product copy should set customer expectations on when money arrives, not promise instant everywhere.

Is pay by bank the same as open banking?

Pay by bank is what the customer sees. Open banking is often how it is delivered — regulated APIs that let a licensed third party initiate a payment from the customer’s account after consent.

Not every bank transfer is open banking (manual IBAN copy-paste is not). Not every open banking product is checkout pay by bank (account data for affordability checks is a different use case). When buyers evaluate providers, they usually need payment initiation capability with good bank coverage and webhooks — plus optional account verification on the same stack.

What you need to implement pay by bank

You typically do not need your own banking licence. You integrate a regulated provider and:

- Add pay by bank as a payment method in checkout or billing

- Handle redirect / deep link return URLs and mobile UX

- Process webhooks for final payment status (do not rely only on the customer returning to your site)

- Keep card or wallet fallback until conversion data supports scaling bank pay

- Map countries and banks to your provider’s coverage before marketing it widely

Legal and UX requirements include clear payee name on the bank screen, accurate amount, and consent wording your legal team approves. PCI scope is lower than card-on-page because you do not capture PANs — but you still secure your integration and customer data.

Frequently Asked Questions

What is pay by bank?

Pay by bank is a payment method where the customer authorises a transfer from their bank account to a business, usually through their banking app, instead of paying with a card. Businesses implement it via regulated payment initiation providers that connect to many banks.

How does pay by bank work at checkout?

The customer selects pay by bank, chooses their bank, authenticates in the bank’s app or online banking, confirms the amount and payee, and returns to the merchant. The merchant receives payment status through the provider’s API, often confirmed by webhooks.

Is pay by bank safe?

Customers authenticate with their bank, not by sharing card numbers on the merchant site. Security depends on correct implementation, HTTPS, webhook verification, and fraud monitoring — same discipline as any payment stack. The bank handles strong authentication for the authorisation step.

Is pay by bank the same as a bank transfer?

Pay by bank is a guided, in-session bank transfer initiated from checkout with immediate status back to the merchant. A manual transfer is when the customer copies an IBAN and pays later offline — slower and harder to reconcile.

Do customers need to install anything for pay by bank?

Usually no extra app beyond their existing mobile banking app. They need an account at a bank your provider supports in that country.

Which countries support pay by bank?

Support is bank-specific, not a single global switch. UK and many EU countries have broad coverage through open banking; depth varies by provider and institution. Always check coverage for your customer banks before launch.

How is pay by bank different from PayPal or cards?

Cards and wallets pull funds through card networks or stored balances. Pay by bank moves money account-to-account with authorisation in the customer’s banking channel — different fees, dispute paths, and UX.

Can pay by bank be used for subscriptions?

Often as the first payment or to verify an account, then recurring collection via direct debit or variable recurring payments where supported. See recurring transactions via open banking for mandate-style renewals.

Conclusion

Pay by bank lets customers pay from the account they already trust — through a banking app authorisation instead of card fields on your site. For businesses, it is a way to improve unit economics, reconciliation, and authentication on the right flows, with bank coverage and UX as the main constraints. Start with one market and measurable conversion against your card baseline, then expand as data supports it. When you are ready to compare who can deliver it for your countries, match on institutions, webhooks, and settlement — not slogans.

Related articles

- Pay by Bank Payment Resilience: When Card Rails Fail

When card acquirers go down, pay by bank payment resilience is the difference between a brief slowdown and a night of lost sales. On 23 June 2026, a power disr…

- Pay by Bank vs Cards at Checkout: Fees & Conversion

Checkout teams in the EU rarely choose a single rail forever. Pay by bank vs card is a trade-off between familiar card UX, interchange economics, dispute workf…

- Pay by Bank Checkout Conversion: EU Patterns That Work

Pay by bank conversion at checkout is the share of buyers who select bank pay and complete authorisation in their banking app. EU teams add pay by bank for low…