ASPSP Definition: What It Means in Open Banking (PSD2)

If your customers pay from a bank account or you verify IBANs before payout, you depend on ASPSPs — the institutions that actually hold those accounts. ASPSP definition work is not academic: when your open banking provider’s bank list misses a major savings bank, checkout fails and finance chases manual fixes. This guide explains ASPSP meaning in plain language, how the role fits open banking and PSD2, how ASPSPs differ from TPPs, AISPs, and PISPs, and what to ask vendors about coverage.

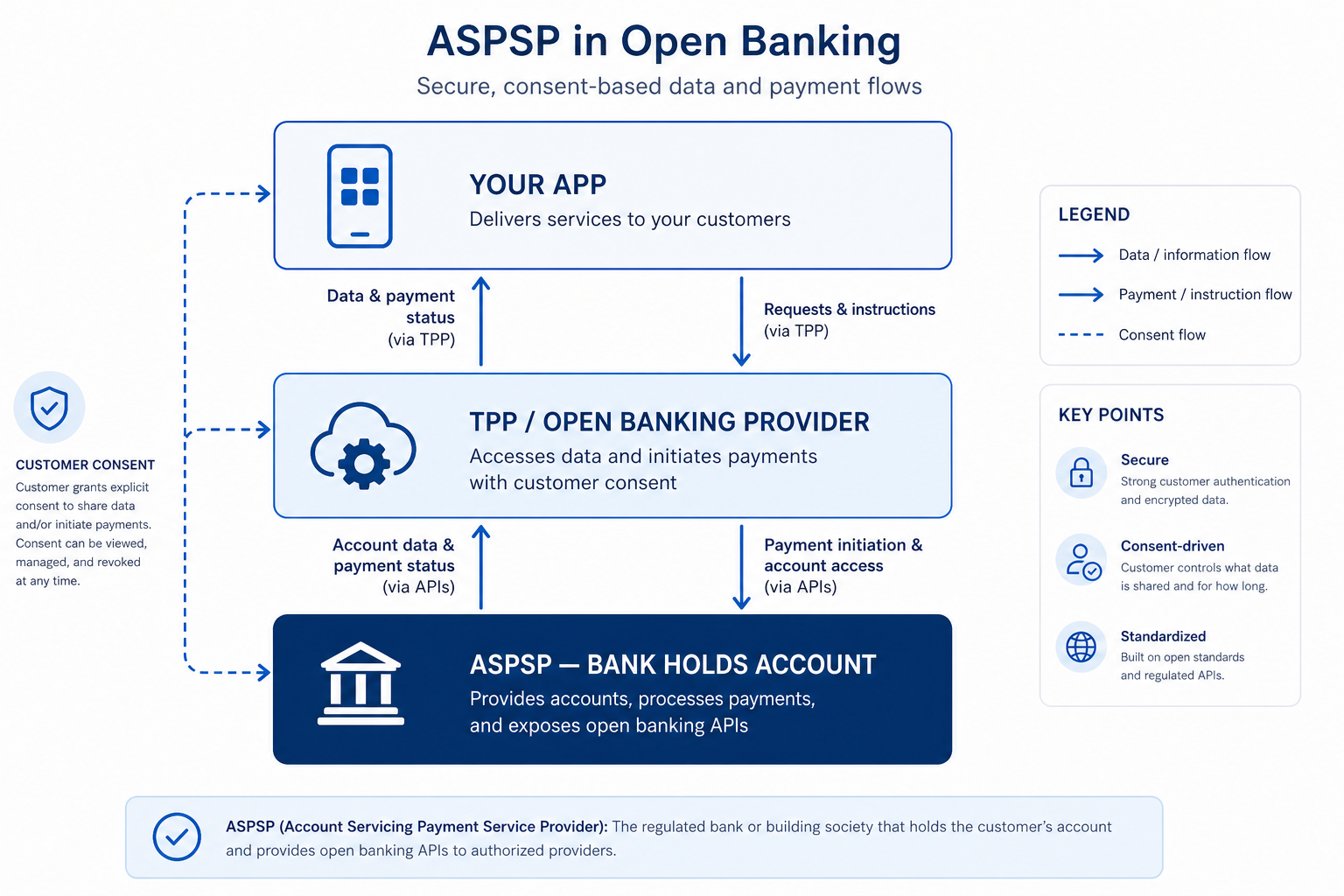

ASPSP (Account Servicing Payment Service Provider): The regulated institution that holds the customer’s payment account — usually a bank — and allows access for payments or account data when the customer consents. Your product typically integrates a licensed third party that connects to many ASPSPs, not each bank directly.

What is an ASPSP?

An ASPSP is where the customer’s money lives: current accounts, many business accounts, and some payment-institution accounts. When someone uses pay by bank, shares transaction history for verification, or authorises a recurring collection, the ASPSP executes or exposes that account — with the customer’s consent.

ASPSP meaning in one operational sentence: the bank (or licensed account host) on the other side of the redirect or app approval your customer completes. Everyone else — aggregators, payment initiation providers, account information providers — connects to ASPSPs.

You rarely sign 400 bank contracts. You sign with a TPP or open banking provider whose value is reaching the ASPSPs your users actually bank with. For how initiation and data rails differ, see AIS vs PIS in open banking. For evaluating those providers, see open banking provider comparison.

What is an ASPSP in open banking and PSD2?

In ASPSP open banking and ASPSP PSD2 contexts, regulators split roles so customers can use third-party apps with accounts they already hold. The ASPSP must offer secure interfaces; licensed third parties access them only after consent.

That matters for product teams in practical terms:

| Role | Who | What changes for your business |

|---|---|---|

| ASPSP | Bank, building society, many neobanks | Holds the account; redirect and settlement behaviour vary by institution |

| AISP | Licensed third party | Reads balances and transactions for verification or insights |

| PISP | Licensed third party | Initiates payments from the account (pay by bank, collections) |

| TPP | Umbrella | Any licensed third party — often your integration partner |

Your company is usually neither an ASPSP nor a TPP unless you hold a payment or banking licence. You integrate a provider that already connects to ASPSPs in each country.

One regulatory reference is enough for due diligence: the European Banking Authority overview of payment services. Day-to-day delivery still comes down to which banks work on your mandatory list.

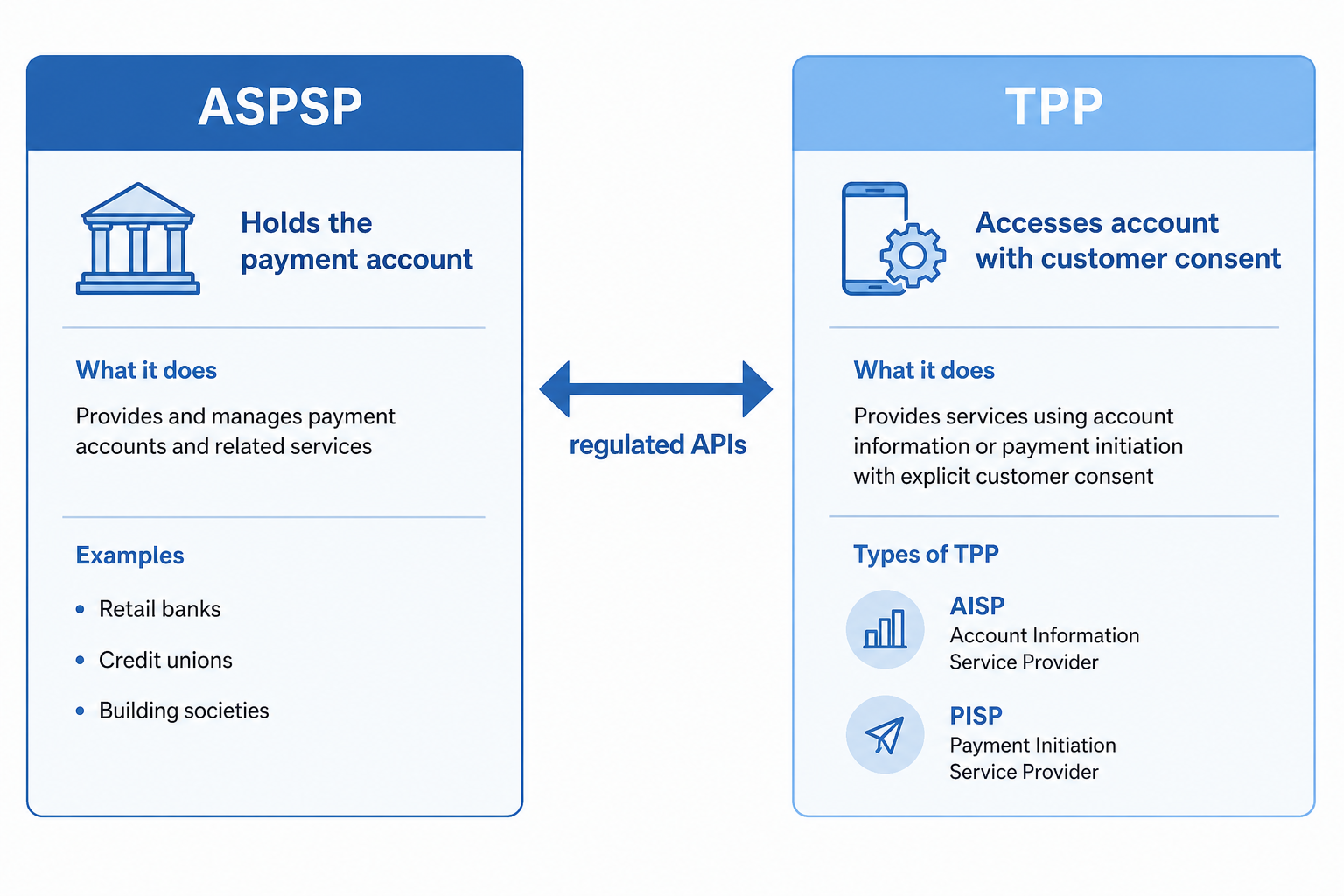

ASPSP vs TPP vs AISP vs PISP — how the roles differ

ASPSPs are thousands of institutions per country. TPPs aggregate access behind one API. Confusing the two causes bad RFPs (“we need open banking in Europe”) instead of bank-level requirements (“we need initiation on Bank X and verification on Bank Y”).

Customer → consents in banking app (ASPSP)

→ ASPSP interface

→ TPP / aggregator (licensed)

→ Your product (payments, verification, data)

| Comparison | ASPSP | TPP (incl. AISP / PISP) |

|---|---|---|

| Holds customer account | Yes | No |

| What you contract | Rarely direct | Yes — your open banking provider |

| Coverage question | Per bank, per rail | “Which ASPSPs do you reach?” |

| Failure mode | “Bank X degraded” | Provider routes, retries, support |

ASPSP vs AISP: the ASPSP hosts the account; the AISP reads information with consent. ASPSP vs PISP: the ASPSP still moves the money; the PISP starts the payment instruction. For developer-oriented provider selection, see best open banking API providers for developers (2026).

What are examples of ASPSPs customers recognise?

Any licensed institution that provides payment accounts can be an ASPSP, including:

- Retail and business banks — salary accounts, invoice collection, card-linked current accounts

- Neobanks with banking licences — they host accounts even when the brand feels app-only

- Some payment institutions — where regulation treats them as account servicers for specific products

Usually not ASPSPs on their own: merchants, pure card networks, or your SaaS — unless you operate licensed customer accounts.

Neobanks are ASPSPs when they hold the account. They act as TPPs when they connect into other banks’ accounts. Many do both.

Why does ASPSP coverage matter when you choose a provider?

You will not negotiate separately with every ASPSP. You will miss revenue if coverage skips the banks your customers use.

- Onboarding and verification — name-and-IBAN match quality varies by ASPSP (instant account verification is bank-specific).

- Payments — pay by bank conversion and settlement speed are ASPSP-specific.

- Incidents — status pages should name institutions, not generic “open banking.”

- Expansion — entering a new country is a new ASPSP mix, not a checkbox on a map.

Ask finalists for an institution export filtered by country and product (initiation, data, verification). Match it to your analytics before you sign. Use how to shortlist open banking providers once your bank list is fixed.

Is ASPSP only a European term?

As a formal label, yes — ASPSP comes from EU and UK open banking rules. Globally, someone still hosts the payment account; API docs may say “ASPSP” for any connected bank. Legal obligations in the ASPSP definition itself are tied to European payment services law.

Frequently Asked Questions

What is the ASPSP definition in open banking?

An ASPSP is a payment service provider that provides and maintains a payment account for a customer — usually a bank — and allows regulated third parties to access that account for payments or account information when the customer consents.

What is ASPSP meaning in plain English?

ASPSP meaning: the customer’s bank (or account host) in a pay-by-bank or account-data flow. Your software talks to a TPP; the TPP talks to the ASPSP after the customer approves access.

What is the difference between ASPSP and TPP?

The ASPSP holds the account. A TPP is a licensed third party that accesses that account on the customer’s behalf. Businesses integrate a TPP that connects to many ASPSPs.

What is the difference between ASPSP and AISP?

The ASPSP hosts the account. An AISP is a type of TPP licensed to read account information with consent. The AISP connects to ASPSPs; it does not replace them.

What is the difference between ASPSP and PISP?

The ASPSP holds the account and executes the payment. A PISP is a TPP licensed to initiate payment instructions with consent.

Is a neobank an ASPSP or a TPP?

It can be either or both. If it holds customer accounts under a banking licence, it is an ASPSP for those accounts. If it also connects to other banks’ accounts, it acts as a TPP for those flows.

Why do provider websites list “ASPSP coverage”?

It means how many account-holding institutions they reach per country for payments, data, or verification — and which products work per bank. Match that list to where your customers bank, not to a global headline count.

Conclusion

ASPSP definition in one line: the regulated institution that hosts the customer’s payment account. TPPs and aggregators connect to ASPSPs so your product can pay, verify, or read data without building hundreds of bank integrations. Move from glossary to vendor choice by filtering providers on your ASPSPs — your users’ banks — using a structured open banking provider comparison and the provider directory.

Related articles

- Build vs Buy Open Banking: When to Partner or Build In-House

Build vs buy open banking is the decision that determines whether your first live bank payment ships in weeks or years. Most EU B2B teams should buy — integrat…

- Open Banking Aggregator Comparison 2026: EU TSP Evaluation

Open banking aggregator comparison 2026 matters when your team needs many EU banks without building dozens of direct integrations. Aggregators — licensed third…

- Open Banking RFP Checklist: What to Include

Procurement teams issue an open banking RFP when multiple business units, legal, or group policy require three comparable bids before signing. Without a tight…