Open Banking for Online Casinos: EU Deposits & Compliance

Licensed online casino operators lose players when deposits fail at the card gateway and when withdrawals sit in manual review. Open banking casino flows — pay by bank for deposits, bank rails for payouts, account data for verification — give EU teams a regulated alternative with a different cost and dispute profile than cards alone. This article focuses on casino operators specifically; for the wider iGaming playbook (sportsbook, betting, eight use cases), see open banking for gaming.

Open banking casino payment: An account-to-account deposit or payout initiated or verified through a licensed third-party provider, with the player consenting in their banking app — used by regulated EU casino operators to fund wallets, pay winnings, and support KYC without card details on the merchant site.

Why do online casinos evaluate open banking?

Open banking for gaming and casino brands share the same pressure: deposit conversion during short sessions, withdrawal speed players treat as product quality, and payment ops cost that scales with volume. Casinos often see higher card scrutiny and chargeback exposure than general e-commerce.

Open banking helps when:

- Deposits — players complete payment in a familiar banking app instead of typing card numbers on a gambling site

- Verification — account ownership checks before first withdrawal reduce wrong-IBAN payouts

- Economics — successful account-to-account flows can beat card interchange on eligible traffic (your mix and provider pricing still matter)

It does not remove licence obligations, AML programmes, or responsible-gambling tooling — it changes how money and identity signals move.

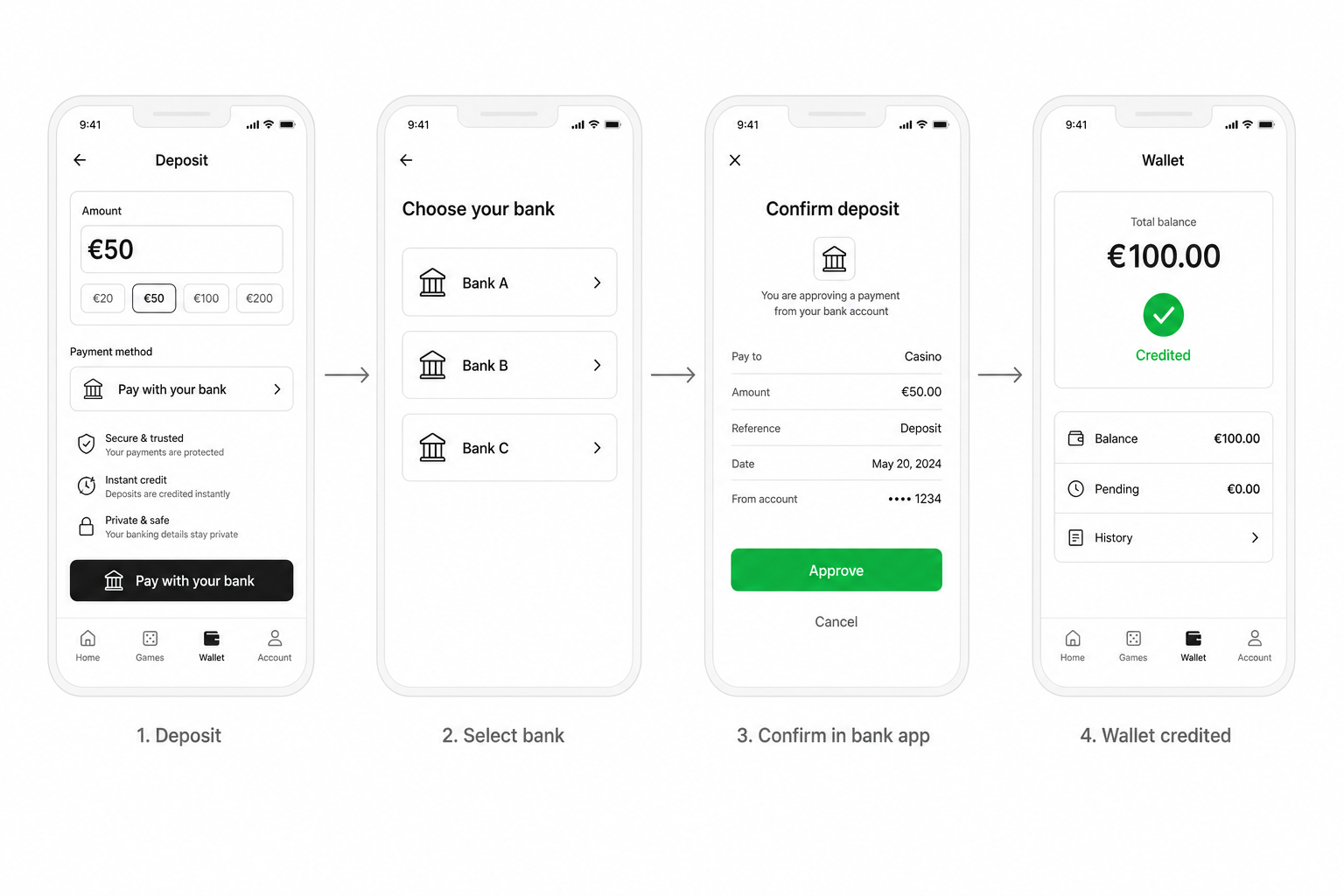

How do casino deposits work with open banking vs cards?

Casino payment open banking usually means payment initiation: the player selects a bank, authenticates with SCA, and authorises a transfer to the operator’s settlement account; the wallet credits when the provider confirms success.

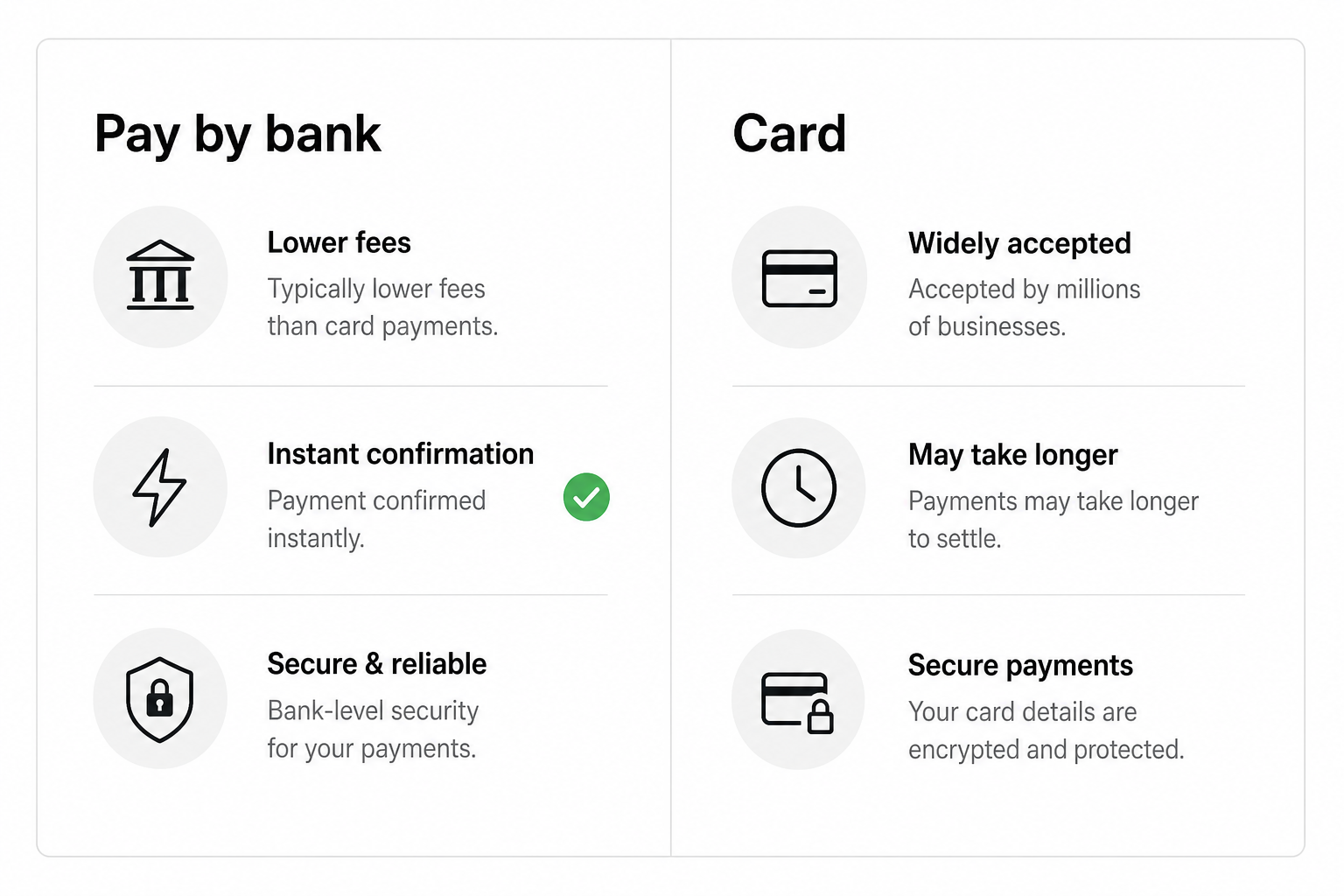

| Dimension | Pay by bank (open banking) | Card deposit |

|---|---|---|

| Customer UX | Redirect to banking app | Card fields on site |

| Dispute profile | Different from card chargebacks | Chargeback exposure |

| Conversion risk | Bank list and mobile UX | Issuer declines, 3DS friction |

| Ops signal | Bank-level success rates | Scheme and acquirer codes |

For rail-level checkout comparison, see pay by bank vs cards at checkout. For how pay by bank works end to end, see pay by bank.

What about compliance and licensing for EU casino payments?

Open banking gambling payments EU teams must treat compliance as a joint exercise between payments, legal, and AML — this section is not legal advice.

Operators typically align:

- Gambling licence in each market where you accept players — payment method availability follows licence geography

- AML and KYC — open banking data and verification feeds source-of-funds and identity workflows; they do not replace policy

- Player consent — each deposit and data access needs clear consent aligned with your privacy notices

- Prohibited flows — some banks or providers restrict gambling MCCs; validate coverage before marketing pay by bank

Document which countries and player banks you support before launch. A method that works in one licence market may be unavailable in another.

What should be on your open banking provider checklist?

Use the same bank-level discipline as any high-risk vertical:

- Coverage — institution list for your top player banks per licence country (initiation and verification separately)

- Deposit conversion — mobile redirect UX, error messaging, retry behaviour

- Withdrawals — payout initiation or verification-only; SEPA vs Instant where you promise speed

- Reconciliation — webhooks, stable payment IDs, finance export formats

- Incident support — named contacts; status by ASPSP not generic “API down”

Cross-check open banking provider comparison dimensions before you run sandboxes. For API evaluation, see how to shortlist open banking providers.

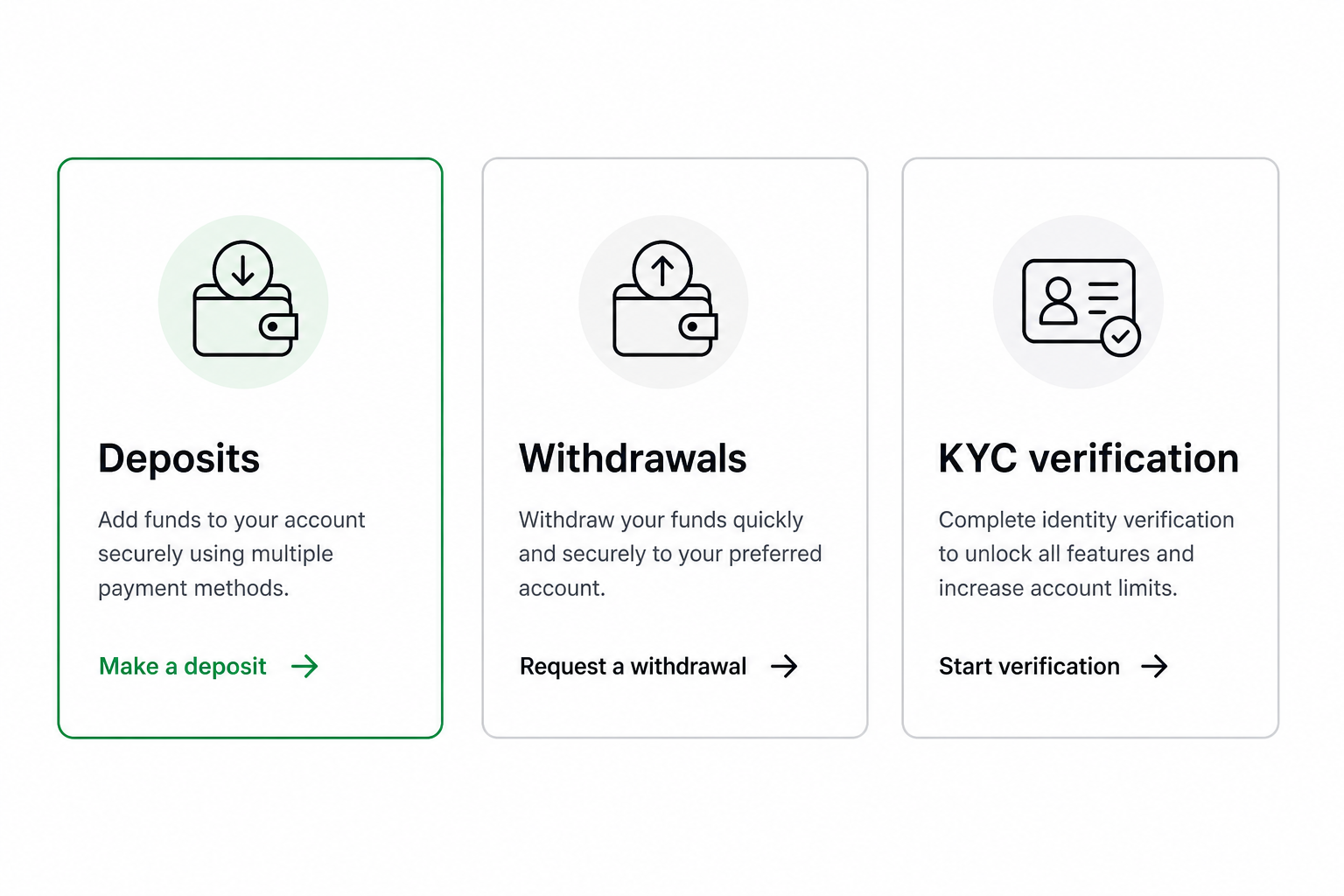

Which casino use cases fit open banking best?

Deposits remain the primary entry point: wallet credit after bank confirmation, especially on mobile. Withdrawals often combine verified IBAN (from account data) with SEPA or Instant payout rails — promise only what your bank mix supports. KYC and AML support use account information and name-IBAN match to reduce manual doc upload — see instant account verification quality by bank.

Sequence matters: prove deposit conversion on mandatory banks before you market withdrawals as “instant.” Parent topic coverage: open banking for gaming.

Frequently Asked Questions

What is open banking casino integration?

It is connecting a licensed open banking provider so players can deposit (and sometimes withdraw) via their bank app, with consent, instead of using card details on the casino site.

Is open banking igaming the same as open banking for online casinos?

Open banking igaming is the broader category (sportsbook, betting, casino). This article focuses on online casino deposit, payout, and verification patterns; the gaming hub covers eight use cases across verticals.

Are open banking gambling payments legal in the EU?

Legality depends on your gambling licence, market rules, and how you implement AML — not on the payment rail alone. Open banking is a regulated way to move money with consent; your compliance team must approve each market.

How does open banking reduce chargeback risk for casinos?

Account-to-account deposits are not card chargebacks. You still face operational disputes, reversals, and fraud — but the dispute mechanics differ from card schemes. Model risk with finance, not only payments.

Can players withdraw casino winnings via open banking?

Many operators use open banking for verification and SEPA or Instant payouts to a pre-matched IBAN. Whether initiation is in scope depends on provider and bank coverage — validate in sandbox before UX promises.

How do I choose a provider for casino payments in the EU?

Start from player bank lists per licence country, test deposit success rates on mobile, then evaluate webhooks, payout SLAs, and commercial model. Use the provider directory after your checklist is defined.

Conclusion

Open banking casino adoption is a coverage and conversion problem first: the banks your players use, on mobile, with reconciliation your finance team can trust. Pair deposits with realistic withdrawal SLAs, keep AML and licensing central, and treat open banking for gaming as the broader playbook while this page stays casino-specific.

Related articles

- Open Banking for Accounting: 6 Use Cases for Finance Teams

Small businesses and their accountants lose hours every month to the same friction: customers pay invoices by card and eat margin on fees, or they pay by manua…

- Open Banking Utility Payments: How Suppliers Collect Bills

Utility billing teams lose margin on three predictable leaks: card interchange on high-volume inbound payments, failed direct debits that trigger dunning and c…

- Open Banking for Payroll: Disbursement & Verification

Payroll platforms lose trust when salaries land late or on the wrong account. Open banking for payroll providers connects verification and disbursement to regu…