Open Banking for Accounting: 6 Use Cases for Finance Teams

Small businesses and their accountants lose hours every month to the same friction: customers pay invoices by card and eat margin on fees, or they pay by manual bank transfer with references finance cannot match. Open banking for accounting embeds pay-by-bank flows inside accounting software — invoice creation, bank-app approval, and ledger updates in one loop — so teams collect faster, reconcile automatically, and keep card costs on optional rails only. On 14 July 2026, GoCardless and Sage announced Pay by Bank inside Sage Business Cloud Accounting for UK and Ireland users, pairing instant account-to-account payments with existing Direct Debit collection. This playbook maps six use cases finance and product teams at accounting platforms can ship, how they differ from generic pay by bank invoice payment flows, and what to validate with providers before rollout.

Open banking for accounting: Embedding regulated bank-payment flows — usually pay by bank initiation and account verification — inside accounting or practice-management software so SMBs and their accountants collect invoices, sync payment status to the general ledger, and reduce manual bank-statement matching. Customers consent in their banking app; funds move account-to-account.

Why are accounting platforms adding open banking now?

Accounting platforms add open banking because card fees on one-off invoices and manual reconciliation still cost SMBs more than a bank-app redirect. Practice accountants and in-house finance teams issue ad-hoc charges — setup fees, project top-ups, catch-up bills — that sit outside recurring Direct Debit schedules. Cards work but interchange on each payment hurts tight-margin businesses; manual transfers create "paid but not matched" tickets.

The GoCardless–Sage expansion (14 July 2026) shows the product shape: Pay by Bank on the invoice, payment status flowing back to Sage Business Cloud Accounting, and Direct Debit retained for subscriptions and retainers. That multi-rail pattern — bank initiation for variable one-offs, mandate-based collection for predictable cycles — is what other accounting vendors are evaluating across the UK and EU.

Outcomes teams measure:

- Lower cost per collected invoice when payers choose bank rails instead of cards

- Hours back for bookkeepers when payment confirmation auto-closes open balances

- Fewer failed first attempts when payers authorise in their own bank app with pre-filled amount and reference

- Cleaner audit trails when every payment ties to an invoice ID in the ledger

You integrate through a licensed open banking or bank-payment provider; the accounting platform stays software, not a bank.

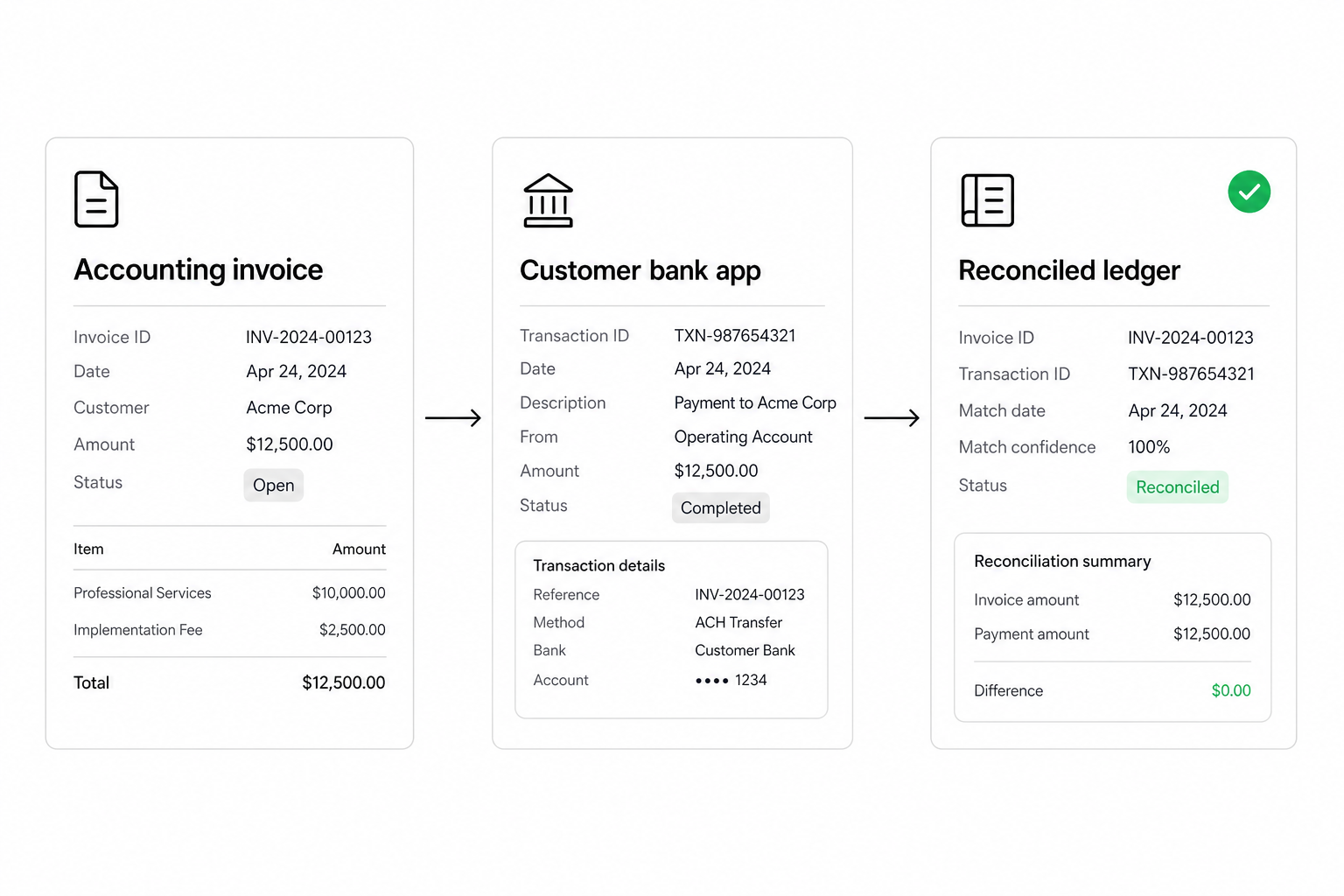

1. Embedded Pay by Bank on invoices

Embed Pay by Bank on invoices when customers routinely pay one-off or variable amounts outside a Direct Debit mandate — setup fees, extra services, or catch-up balances.

The payer opens the invoice in email or the client portal, clicks pay from bank, selects their institution, and approves the exact amount with a structured reference. Your accounting module receives confirmation and marks the invoice paid without someone downloading CSV bank lines.

According to the GoCardless–Sage announcement, Sage users in the UK and Ireland can now offer that card-free path alongside existing GoCardless Direct Debit — a template other vendors are copying for embedded collections.

Trade-off: every one-off payment needs payer action in the bank app unless you also hold a recurring mandate. Keep cards as fallback for payers who expect rewards or lack bank-app payment initiation in their market.

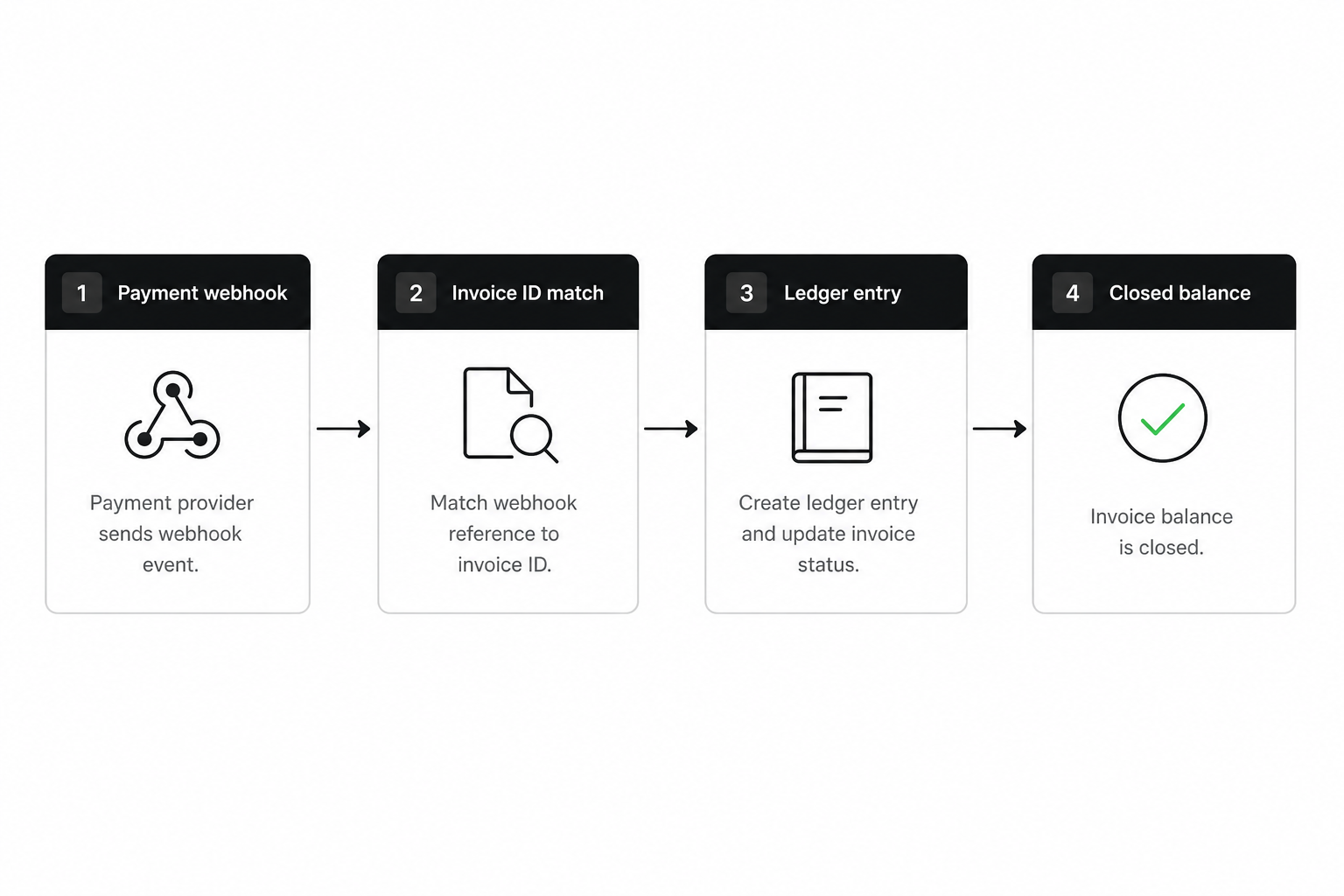

2. Automatic invoice-to-ledger reconciliation

Automatic reconciliation closes the loop between "customer paid" and "books updated" — the main ops win accounting teams cite after embedding bank payments.

When payment status syncs from the provider webhook into the accounting dashboard, finance avoids matching paper statements, chasing "we already paid" emails, and re-keying amounts. The reference on the bank payment should equal the invoice number or internal ID your GL already uses.

Done well, month-end close starts with fewer unmatched lines. Done poorly, you add another disconnected feed. Require idempotent webhooks, stable reference schemas, and clear failed-payment states before you market auto-reconciliation to practice clients.

3. Variable client billing for practices and agencies

Variable client billing — project milestones, usage true-ups, or seasonal spikes — fits pay-by-bank initiation better than forcing a new card charge each time.

Accountants and agencies billing clients monthly retainers plus ad-hoc work hit this constantly: the retainer runs on Direct Debit or SEPA DD, but the extra £2,400 for tax work needs a separate collection path. Open banking lets you invoice the exact amount and collect in one session.

GoCardless also launched Recurring Pay by Bank in its July 2026 product updates for businesses with flexible billing (utilities, telecoms, financial services) — a signal that variable recurring bank collection is moving from pilot to production, not only one-off invoice links. Practice platforms should watch whether their payment partner supports variable recurring within agreed caps, not only single-shot initiation.

4. Multi-rail collection inside one accounting stack

Run multiple collection rails from one accounting stack — Direct Debit or SEPA DD for retainers, Pay by Bank for exceptions, cards where bank redirect is unfamiliar — instead of forcing every invoice through one method.

| Job | Typical rail | Why |

|---|---|---|

| Monthly retainer | SEPA Direct Debit / UK Direct Debit | Predictable amount; mandate already active |

| One-off project fee | Pay by Bank (PIS) | Exact amount; lower fees than cards on many flows |

| Failed DD recovery | Pay by Bank link in dunning email | Instant authorisation without new mandate |

| Consumer-facing micro-invoices | Card optional | Familiar UX where bank pay is still emerging |

This mirrors patterns in open banking for SaaS platforms and open banking utility payments — stable cycles on mandate rails, exceptions on initiation — but the buyer here is the accounting product or practice, not a utility billing engine.

5. Account verification before you store client bank details

Verify client bank accounts at onboarding before you store details for payouts, refunds, or mandate setup — wrong-IBAN errors are expensive in professional services.

Open banking verification confirms the account holder name matches the client record in one consent step. Practices use it when:

- Setting up client Direct Debit for the first time

- Paying VAT refunds or credit notes to a client-supplied IBAN

- Onboarding contractors where payroll or open banking for payroll providers flows need a verified destination account

Verification does not replace KYC on the client relationship — it reduces payment-rail mistakes that show up as failed payouts and support tickets.

6. UK and EU rollout criteria for accounting vendors

Roll out bank payments market-by-market: UK and Ireland lead on embedded accounting integrations today; EU mainland needs per-country institution coverage and SEPA reference discipline.

Checklist for product and partnerships teams:

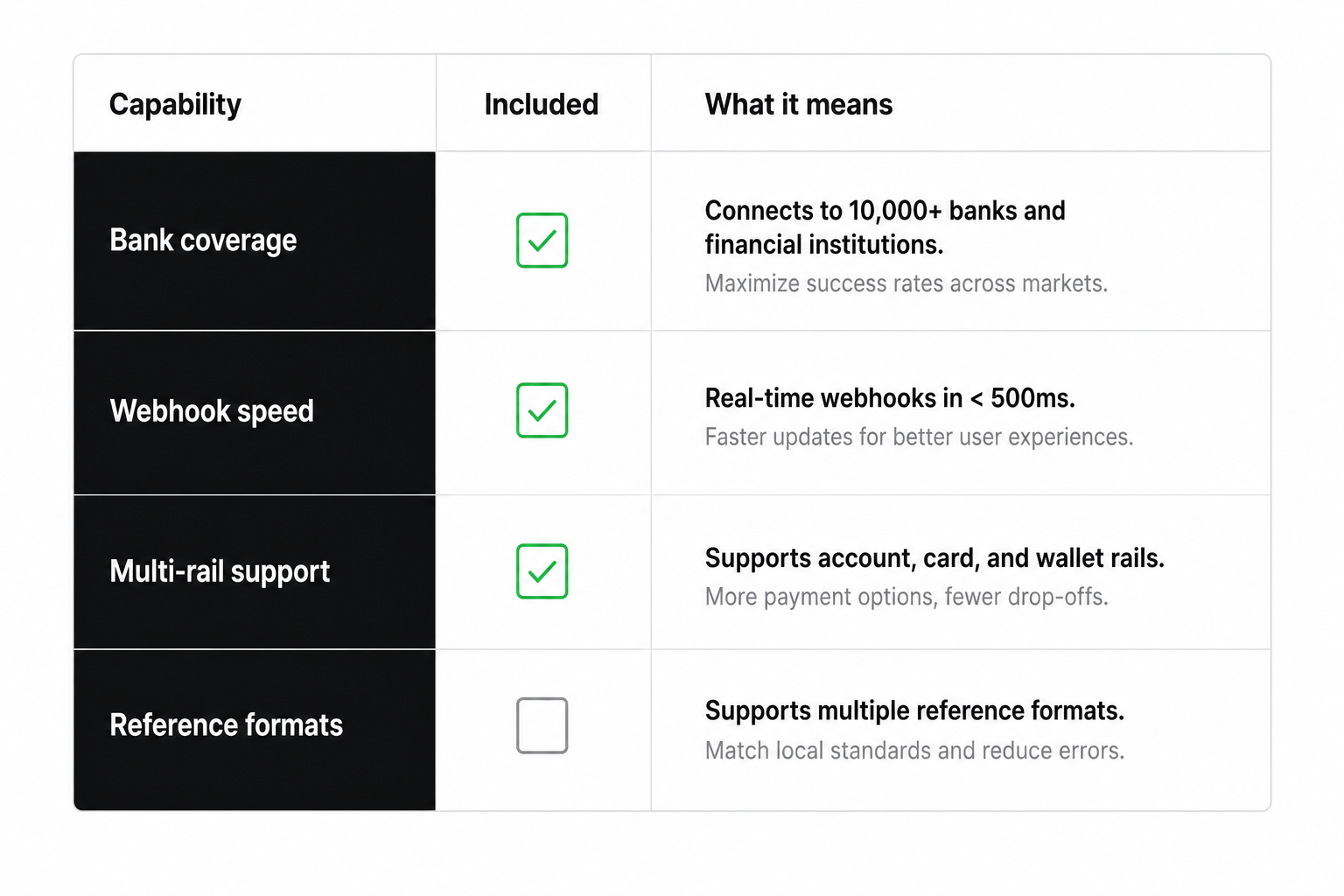

- Institution coverage in your core customer countries — sandbox lists must match production

- Invoice reference format compatible with SEPA and Faster Payments schemes

- Webhook latency acceptable for real-time ledger sync (sub-minute for SMB UX)

- Direct Debit + PIS from one partner to avoid duplicate onboarding for practices

- Data residency and DPA aligned with how you store client financial data

For a deeper comparison of UK scheme rules versus EU PSD2 access, see open banking UK vs EU. When you are ready to compare providers on coverage and commercial models, use our provider matching tool to shortlist options against your markets and use cases — neutral criteria, no single-vendor claims.

How to evaluate open banking providers for accounting software

Prioritise partners that already integrate with accounting ecosystems or expose clean APIs your platform team can embed: coverage in UK and EU markets where your customers file, reliable payment initiation and Direct Debit in one contract, webhooks your invoice module can consume, sandbox parity with production banks, and references that map to invoice IDs without manual transformation.

Confirm commercial acceptance of accounting and practice-management business models — some providers optimise for e-commerce checkout and treat ledger sync as out of scope. Ask for live examples of invoice-status sync, not only payment links.

Frequently Asked Questions

What is open banking for accounting?

Open banking for accounting means accounting or practice-management software uses regulated bank APIs — typically payment initiation and account verification — so businesses collect invoice payments from customer bank accounts, confirm account details, and sync payment status to the general ledger without relying only on cards or manual transfers.

How is open banking for accounting different from pay by bank on a standalone invoice?

Standalone pay by bank invoice payment focuses on the payer journey and B2B collection mechanics. Open banking for accounting adds the software context: invoice creation inside the ledger, automatic balance updates, and multi-rail collection (Direct Debit plus Pay by Bank) managed from the same platform practices already use daily.

Did Sage add Pay by Bank to its accounting product?

Yes. GoCardless and Sage announced on 14 July 2026 that Pay by Bank is embedded in Sage Business Cloud Accounting for UK and Ireland, adding instant account-to-account payments alongside existing GoCardless Direct Debit, with payment status syncing back to Sage for reconciliation.

Can accounting firms use open banking for recurring client fees?

Yes. Retainers and fixed monthly fees often stay on Direct Debit or SEPA Direct Debit mandates. Open banking also supports variable recurring collection where schemes and providers allow — for example UK commercial variable recurring payments in regulated sectors, or hybrid models with pay-by-bank true-ups on top of a DD base.

What are the main trade-offs versus card payments on invoices?

Bank payments typically reduce per-transaction fees and chargeback exposure because the payer authorises in their own bank. Trade-offs include payer familiarity (some expect cards), need for strong bank coverage in each market, and the fact that one-off pay-by-bank flows require customer action unless a separate recurring mandate exists.

How do we choose an open banking provider for an accounting integration?

Compare institution coverage in your customer countries, whether one partner delivers both initiation and Direct Debit, webhook reliability for ledger sync, sandbox quality, reference-field compatibility with your invoice IDs, and contractual acceptance of accounting or practice-management use cases. Route detailed shortlisting through a structured provider comparison rather than picking from marketing claims alone.

Does open banking replace accountants' bank reconciliation work entirely?

No. Open banking automates matching for payments that flow through integrated rails with correct references. Accountants still reconcile external transfers, multi-currency edge cases, and legacy channels — but embedded pay by bank shrinks the manual pile when adoption is strong.

Conclusion

Open banking for accounting is moving from standalone payment links into the ledger: invoice out, bank-app approval, balance closed — with Direct Debit retained for predictable cycles. The GoCardless–Sage launch is the latest proof point for UK and Ireland SMBs; EU platforms should map the same jobs — embedded initiation, auto-reconciliation, verification — against their markets before promising a card-free default. Start with one-off and variable invoices where card fees hurt most, then expand recurring bank rails where schemes allow.

Related articles

- Open Banking Utility Payments: How Suppliers Collect Bills

Utility billing teams lose margin on three predictable leaks: card interchange on high-volume inbound payments, failed direct debits that trigger dunning and c…

- Open Banking for Online Casinos: EU Deposits & Compliance

Licensed online casino operators lose players when deposits fail at the card gateway and when withdrawals sit in manual review. Open banking casino flows — pay…

- Open Banking for Payroll: Disbursement & Verification

Payroll platforms lose trust when salaries land late or on the wrong account. Open banking for payroll providers connects verification and disbursement to regu…