Pay by Bank Invoice Payment: B2B Collection Without Card Fees

Finance teams add pay by bank invoice payment when card fees on large B2B invoices, slow manual transfers, and reconciliation gaps cost more than a short bank-app redirect. Instead of copying IBAN details into online banking, the payer opens a secure link, selects their bank, and approves the exact amount with a structured reference — you get confirmation and payer account data for matching. This guide covers when invoice pay-by-bank beats cards and manual transfer, how the payer journey works, reconciliation patterns, and what to validate with providers before rollout.

Pay by bank invoice payment: A B2B collection method where the customer pays an invoice by authorising an account-to-account transfer in their banking app — usually via a payment link with pre-filled amount and reference — instead of entering card details or manually typing IBAN and amount offline.

For the consumer checkout version of the same rail, start with pay by bank explained. For fees and chargeback trade-offs versus cards, see pay by bank vs cards at checkout.

When should B2B teams offer pay by bank on invoices?

Offer pay by bank on invoices when ticket sizes are high enough that card interchange hurts, payers already use bank transfer today, and you need structured references finance can match automatically.

Typical fits:

- Professional services and SaaS annual contracts — invoices above card comfort thresholds where payers prefer bank rails

- Wholesale and distribution — repeat buyers with approved vendor relationships and predictable IBAN payees

- Platforms billing business accounts — where the payer is a finance user, not a cardholder with loyalty points

- Cross-border EU B2B — SEPA credit transfer with end-to-end reference beats ad-hoc manual entry errors

Skip or deprioritise when:

- Payers are consumers expecting card rewards — B2C invoice flows often convert better with cards unless amounts are large

- Your buyers sit in markets with weak bank-app payment initiation — validate institution lists before promising the method

- You cannot confirm payment before shipping high-risk goods — bank rails may be pending; align release rules with webhooks

According to Open Banking Limited, more than 37 million open banking payments are processed monthly in the UK alone — most are still one-off payments rather than recurring relationships, which leaves room for B2B invoice collection to mature alongside checkout use cases.

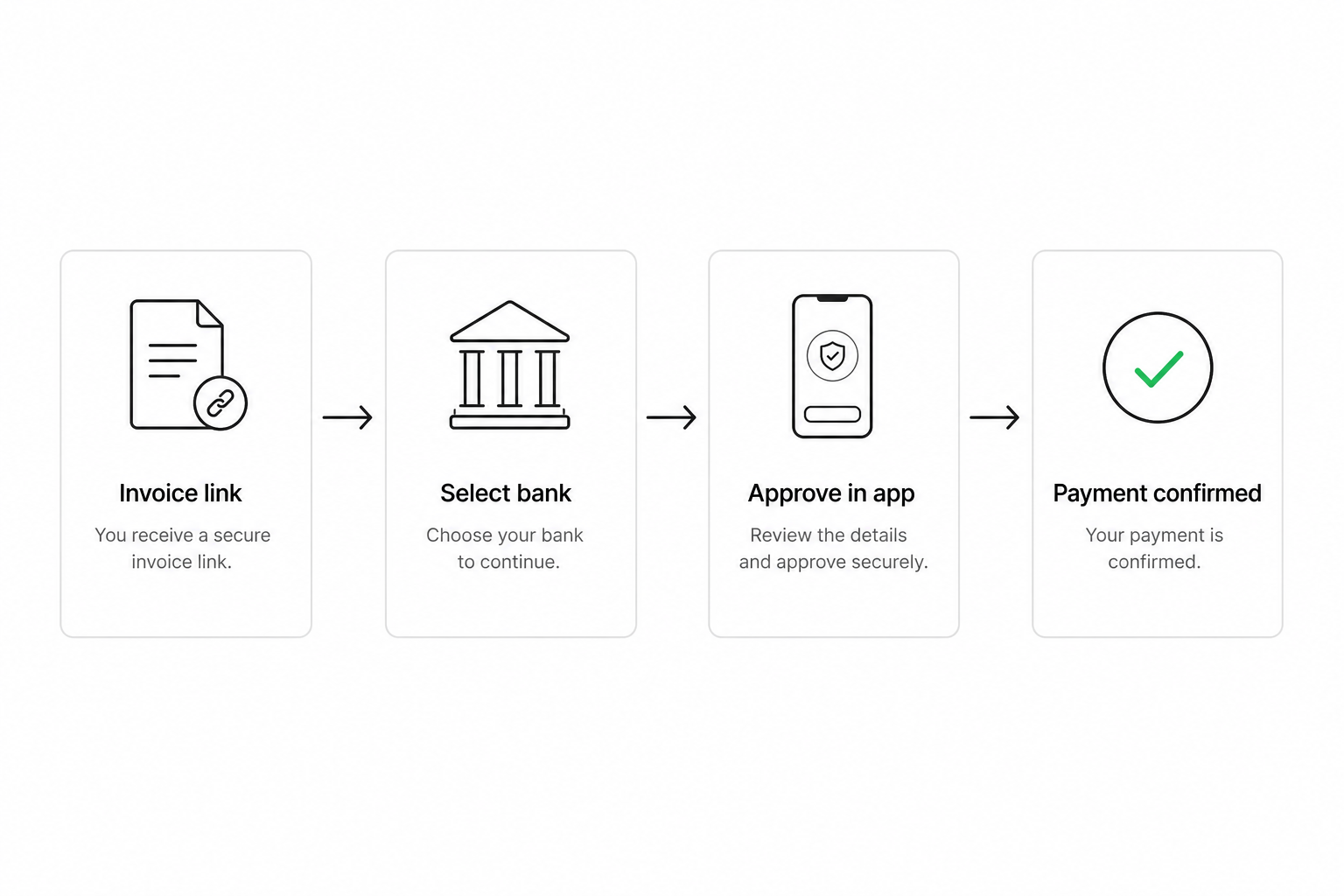

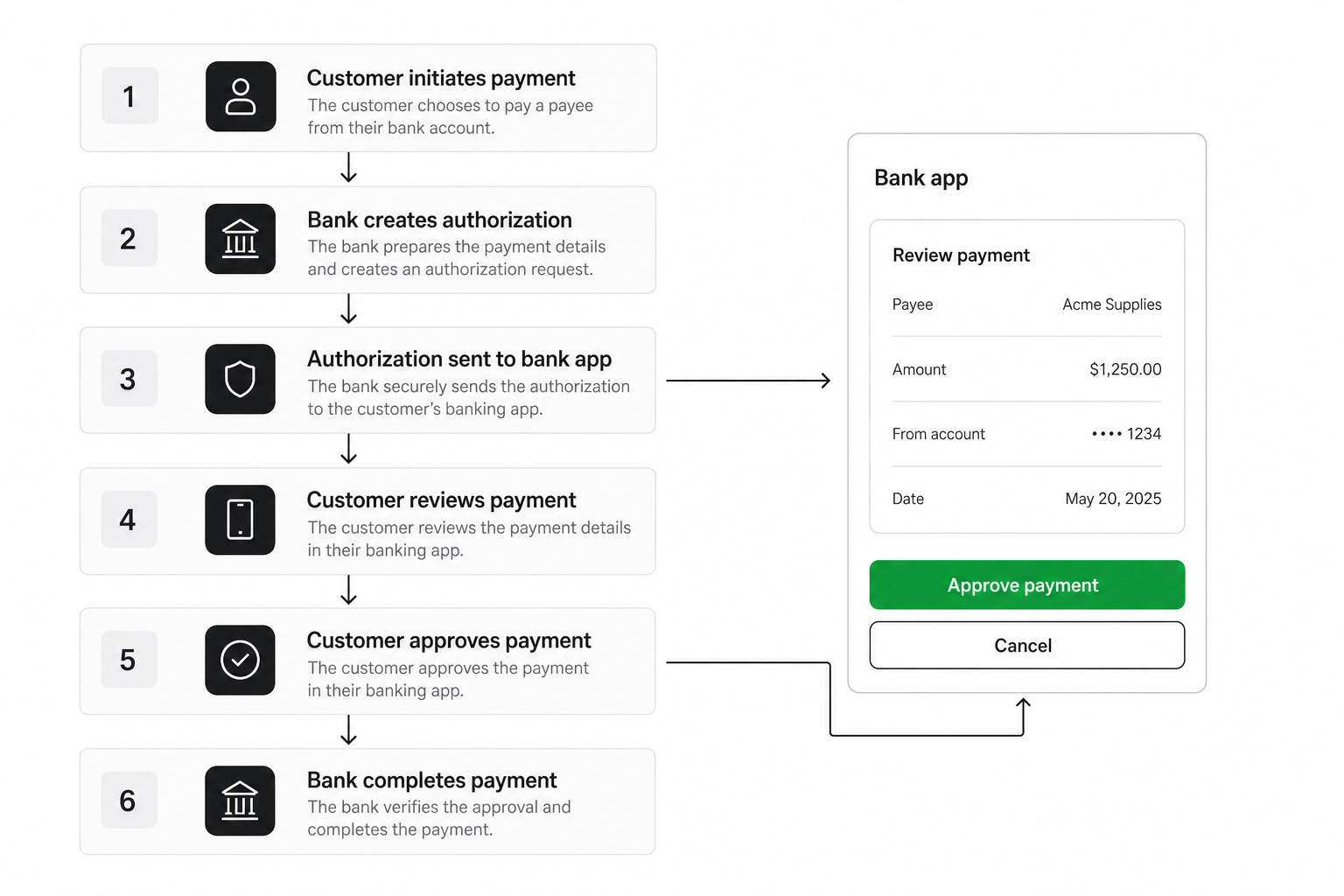

How does pay by bank invoice payment work for the payer?

The payer clicks a link on the invoice, selects their bank, authenticates in the mobile or online banking app, confirms amount and payee, and returns to a confirmation page while your system receives status via API.

Step by step:

- Invoice issued — PDF, email, or portal shows total, due date, and a "Pay from bank" button alongside card or manual transfer options.

- Secure payment session opens — amount and creditor reference are pre-filled; the payer does not re-type the invoice total.

- Bank selection — list filtered by country; domestic banks first for B2B payers.

- Strong authentication in bank channel — approval happens in the banking app, not on your domain.

- Status returned — accepted, pending, failed, or cancelled; your ERP or billing system updates via webhook.

- Receipt and reconciliation — payer gets confirmation; finance matches end-to-end ID or structured reference to the invoice line.

The experience differs from manual bank transfer because the payer cannot easily mistype the amount or reference. It differs from card on invoice because there is no card number entry and dispute economics follow bank rails, not card chargebacks.

For UX patterns that reduce drop-off once bank pay is visible, see pay by bank checkout conversion.

What changes for finance and reconciliation?

Pay by bank invoice payment gives finance structured identifiers — payer IBAN, amount, timestamp, and reference — that map to invoice numbers without manual statement hunting.

Reference discipline

- Pre-fill creditor reference on the bank screen (invoice ID, customer account code, or structured SEPA reference).

- Reject or flag partial payments unless your provider supports open-amount flows with explicit payer intent.

- Separate VAT lines in your ERP — the bank sees one total; your ledger still splits tax internally.

Matching rules

| Signal | Reconciliation use |

|---|---|

| End-to-end ID | Primary match key for SEPA flows |

| Payer IBAN | Validates expected buyer account; flags third-party payers |

| Amount + reference | Catches duplicates and rounding errors |

| Webhook timestamp | Drives dunning and credit-hold automation |

Settlement timing

Standard SEPA credit transfer may settle next business day; SEPA Instant where both banks support it can shorten cash application. Product copy on the invoice should state when funds arrive — do not promise instant settlement in every EU market. The European Payments Council continues to expand instant payment adoption across SEPA; availability still varies by bank pair.

Teams running open banking for SaaS platforms often combine first invoice pay-by-bank with direct debit or recurring bank mandates for renewals — invoice collection is the entry rail, not the only one.

Pay by bank vs card vs manual transfer on invoices

Cards win on payer habit for small amounts; manual transfer wins on zero redirect friction for expert treasury users; pay by bank wins when you need both lower variable cost and guided references on medium-to-large B2B invoices.

| Method | Payer effort | Typical B2B trade-off |

|---|---|---|

| Pay by bank (invoice link) | One redirect to bank app | Lower fees than many card flows; structured reference |

| Card on invoice | Enter card or use saved card | Familiar; interchange on large tickets |

| Manual bank transfer | Copy IBAN offline | Cheap but error-prone; slow application |

| Direct debit mandate | One-off mandate setup | Strong for repeat billing; weaker for one-off invoices |

Partial payments deserve explicit product design: either block amounts that do not match the open invoice total, or route underpayments to a controlled exception queue. Silent partials destroy DSO metrics.

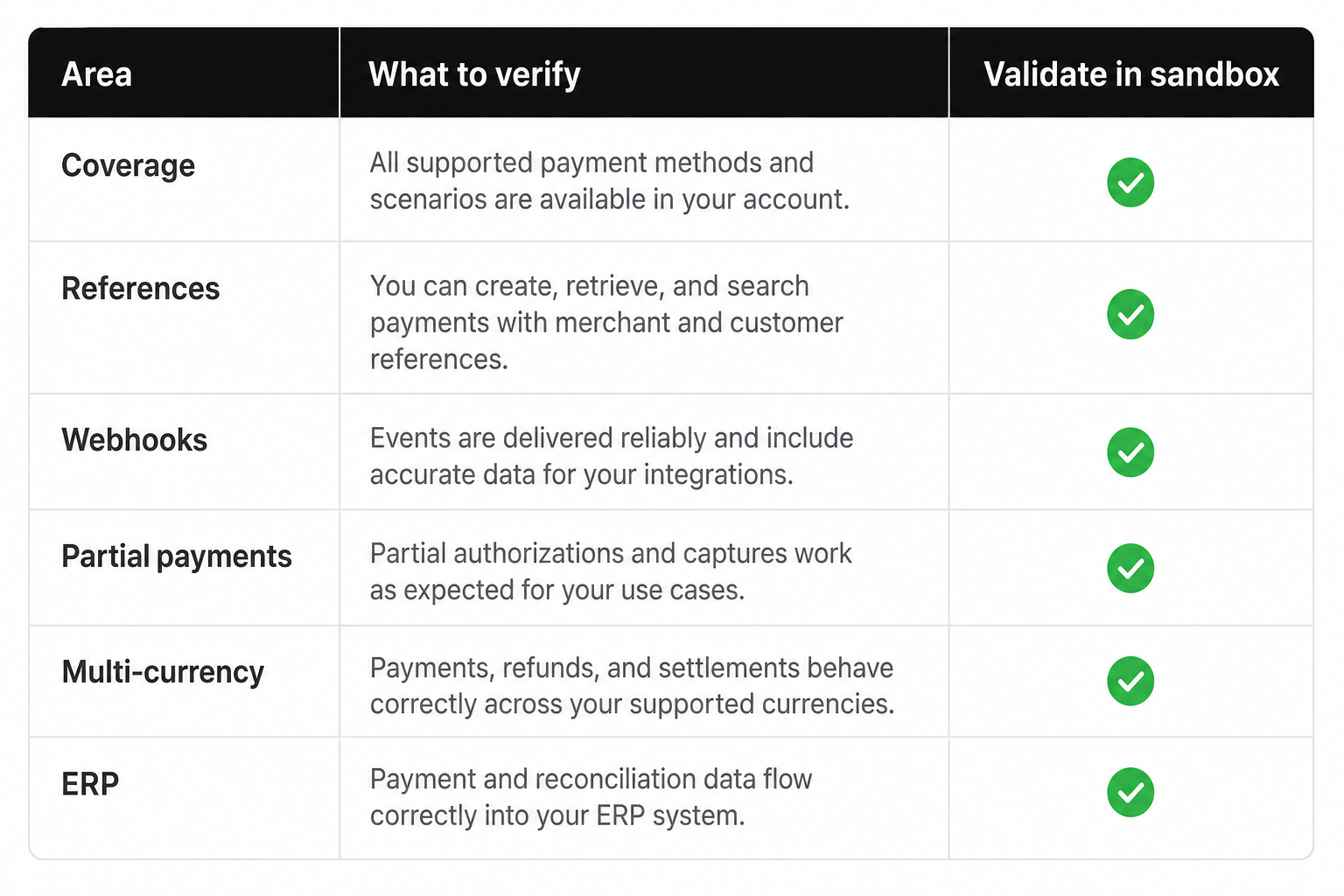

Which provider criteria matter for invoice pay-by-bank?

Shortlist providers on institution coverage for your buyers' countries, webhook reliability, reference field support, and sandbox fidelity to production bank lists — not headline "EU-wide" maps.

| Criterion | Invoice-specific question |

|---|---|

| Coverage | Do your top 20 buyer banks support payment initiation in each market? |

| Reference fields | Can you pass structured remittance data the bank displays verbatim? |

| Webhooks | Do you get final status without relying on browser return? |

| Partial / overpayment | How are mismatched amounts handled? |

| Multi-currency | Do you bill in GBP and EUR with separate bank lists? |

| ERP connectors | NetSuite, Xero, or custom API — what is actually shipped vs roadmap? |

Run sandbox tests with production-shaped invoice amounts and references. Fail paths matter: payer cancels in bank app, insufficient funds, or bank maintenance windows during month-end close.

When you are ready to compare live coverage against your buyer markets, use the provider-matching form to share countries, invoice volumes, and ERP constraints — or start from how to choose an open banking provider in the EU for evaluation dimensions.

How do you roll out pay by bank on invoices without hurting cash collection?

Pilot with one segment, measure time-to-pay and reconciliation hours, then expand — keep card and manual transfer visible until bank pay proves conversion.

- Segment — domestic B2B accounts above a fee threshold where bank pay economics are clearest.

- Copy — explain "Pay in your bank app" with expected settlement timing; link to support for first-time payers.

- Ops — train AR to read webhook statuses; define credit-release rules for pending vs settled.

- Measure — days sales outstanding, cost per collected euro, manual match hours, and payer support tickets.

- Expand — add markets as coverage proofs complete; do not global-launch from a UK-only sandbox.

The UK FCA statement on the UK Payments Initiative highlights industry momentum toward recurring and commercial open banking payments — invoice collection sits on the same infrastructure maturity curve, even when your first rollout is one-off initiation rather than variable recurring mandates.

Frequently Asked Questions

What is pay by bank invoice payment?

Pay by bank invoice payment is a B2B collection flow where the customer pays an invoice by approving an account-to-account transfer in their banking app, usually from a link with pre-filled amount and reference. It reduces manual IBAN entry errors and often lowers variable fees compared with card acceptance on large tickets.

How is pay by bank on invoices different from checkout pay by bank?

Checkout pay by bank completes a basket in an e-commerce session; invoice pay by bank ties to a specific invoice ID, due date, and open amount in accounts receivable. The technical rail is similar, but reference discipline, partial-payment rules, and ERP matching are more important on invoices.

Can customers pay an invoice partially via pay by bank?

Yes, if your provider and bank flow support open amounts and your policy allows partial settlement. Many B2B teams block partials by default and route exceptions manually to protect DSO reporting. Define the rule before launch.

Is pay by bank invoice payment cheaper than cards for B2B?

On many EU account-to-account flows, variable cost per successful payment is lower than card interchange on comparable invoice sizes, especially for large B2B tickets. Economics depend on provider pricing, market, and whether payers actually choose the rail — model both fee and conversion.

Do pay by bank invoice payments settle instantly?

Not always. Standard SEPA credit transfer may take a business day; SEPA Instant settles in seconds when both banks support it. State expected timing on the invoice and in confirmation emails rather than promising instant everywhere.

What reference data should appear on the bank screen?

At minimum: exact amount, payee name your buyer recognises, and a structured reference matching your invoice or customer account ID. Finance should match webhook payloads to the same keys in your ERP.

How do I choose a provider for invoice pay-by-bank?

Filter on institution coverage for your buyers' banks, webhook reliability, reference field support, and sandbox tests that mirror production. Compare finalists on reconciliation fit and ERP integration — use the provider-matching form when you have market and volume requirements ready.

Conclusion

Pay by bank invoice payment fits B2B teams when large tickets, manual transfer friction, or card fees push finance toward account-to-account collection with guided references. The payer journey is short; the operational win is reconciliation and cost per collected euro. Pilot with a defined segment, keep fallback rails visible, and validate bank coverage before you promise the method on every invoice.

Related articles

- Pay by Bank Payment Resilience: When Card Rails Fail

When card acquirers go down, pay by bank payment resilience is the difference between a brief slowdown and a night of lost sales. On 23 June 2026, a power disr…

- Pay by Bank vs Cards at Checkout: Fees & Conversion

Checkout teams in the EU rarely choose a single rail forever. Pay by bank vs card is a trade-off between familiar card UX, interchange economics, dispute workf…

- Pay by Bank Checkout Conversion: EU Patterns That Work

Pay by bank conversion at checkout is the share of buyers who select bank pay and complete authorisation in their banking app. EU teams add pay by bank for low…