Pay by Bank Payment Resilience: When Card Rails Fail

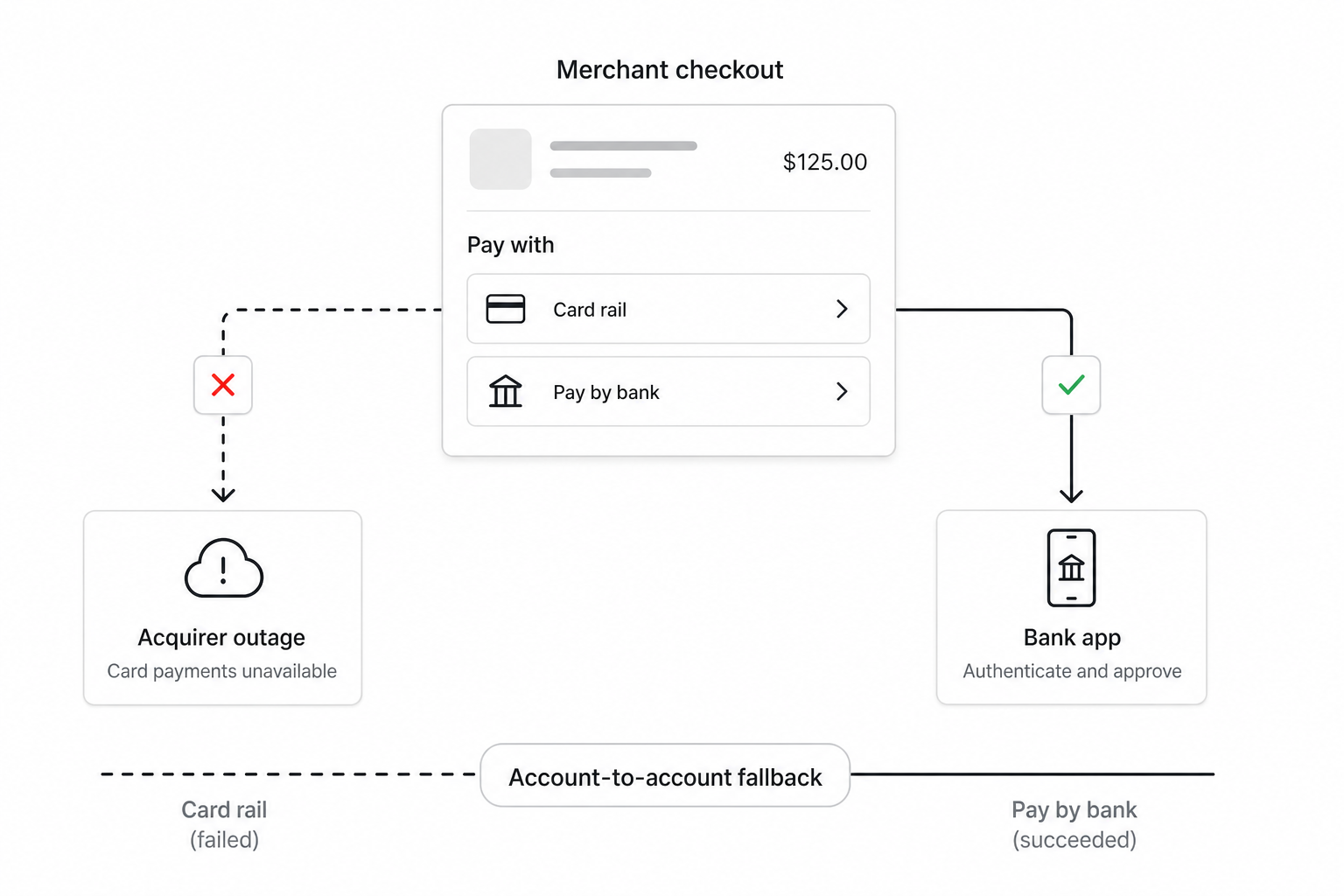

When card acquirers go down, pay by bank payment resilience is the difference between a brief slowdown and a night of lost sales. On 23 June 2026, a power disruption hit Worldpay authorisation platforms across the UK — supermarkets, pubs, and restaurants reported card and contactless failures during England's World Cup match against Ghana. Merchants with only card rails had no digital fallback; teams that already offered account-to-account pay from banking apps kept a second path open. This guide explains how EU checkout teams design dual-rail resilience without betting everything on one processor.

Pay by bank payment resilience: A checkout architecture where customers can pay from their banking app on separate infrastructure from card acquiring — so an acquirer or scheme outage does not remove every way to complete a purchase. Resilience comes from dual rails, visible fallbacks, webhook confirmation, and ops playbooks tested before incidents.

For fees and day-to-day economics, see pay by bank vs cards at checkout. For conversion patterns once bank pay is live, see pay by bank checkout conversion.

Why did the June 2026 Worldpay outage matter for checkout teams?

Card-only checkout is a single point of failure. When authorisation platforms fail, every terminal, hosted page, and wallet pass-through on that stack stops — regardless of how healthy your website or inventory systems are.

Worldpay reported on its status page that a third-party power outage affected transaction authorisations on multiple platforms, with some transactions declined or returning errors while technical teams recovered service. UK press including the Manchester Evening News documented card failures at major supermarkets and hospitality venues on the evening of 23 June 2026.

The lesson for product and payments leads is structural, not vendor-specific:

- Acquirer outages are rare but high-impact — they cluster around peak demand (match nights, pay-day weekends, sales events).

- Contactless and card-not-present share infrastructure — an in-store terminal failure often mirrors e-commerce authorisation problems on the same processor.

- Cash-only fallback is not a digital strategy — it helps physical stores temporarily but does not rescue online checkout or app orders.

Teams evaluating pay by bank payment resilience treat the incident as a stress test: if your card stack disappeared for two hours tonight, would any customer still pay you?

How does pay by bank reduce dependency on card acquirers?

Pay by bank moves money account-to-account after the customer approves in their banking app — on rails separate from card schemes and acquirer authorisation.

That separation is the resilience mechanism. Card payments flow through acquirers, schemes, and issuer authorisation engines. Pay by bank via regulated payment initiation uses bank APIs and SEPA (or domestic instant) settlement paths managed by payment initiation providers. A Worldpay-style outage does not automatically disable every bank's mobile app.

What pay by bank does not guarantee:

- Zero downtime — individual banks, PIS providers, and directory services have their own incidents.

- Identical UX — customers must select a bank and approve in-app; it is not a tap-to-pay card experience.

- Instant recovery for every basket — cross-border tourists without eligible accounts may still need cards when bank lists are domestic.

What it does provide:

- Independent failure domain — card acquirer down ≠ all bank apps down.

- Lower marginal cost per success on many EU flows — useful when you steer overflow traffic during card incidents without destroying margin.

- Deterministic references — IBAN, amount, and end-to-end IDs simplify reconciliation when volume spikes on the fallback rail.

Pair pay by bank with cards as complementary rails, not a replacement you only remember during outages. Customers who never see bank pay in normal weeks will not discover it during a crisis.

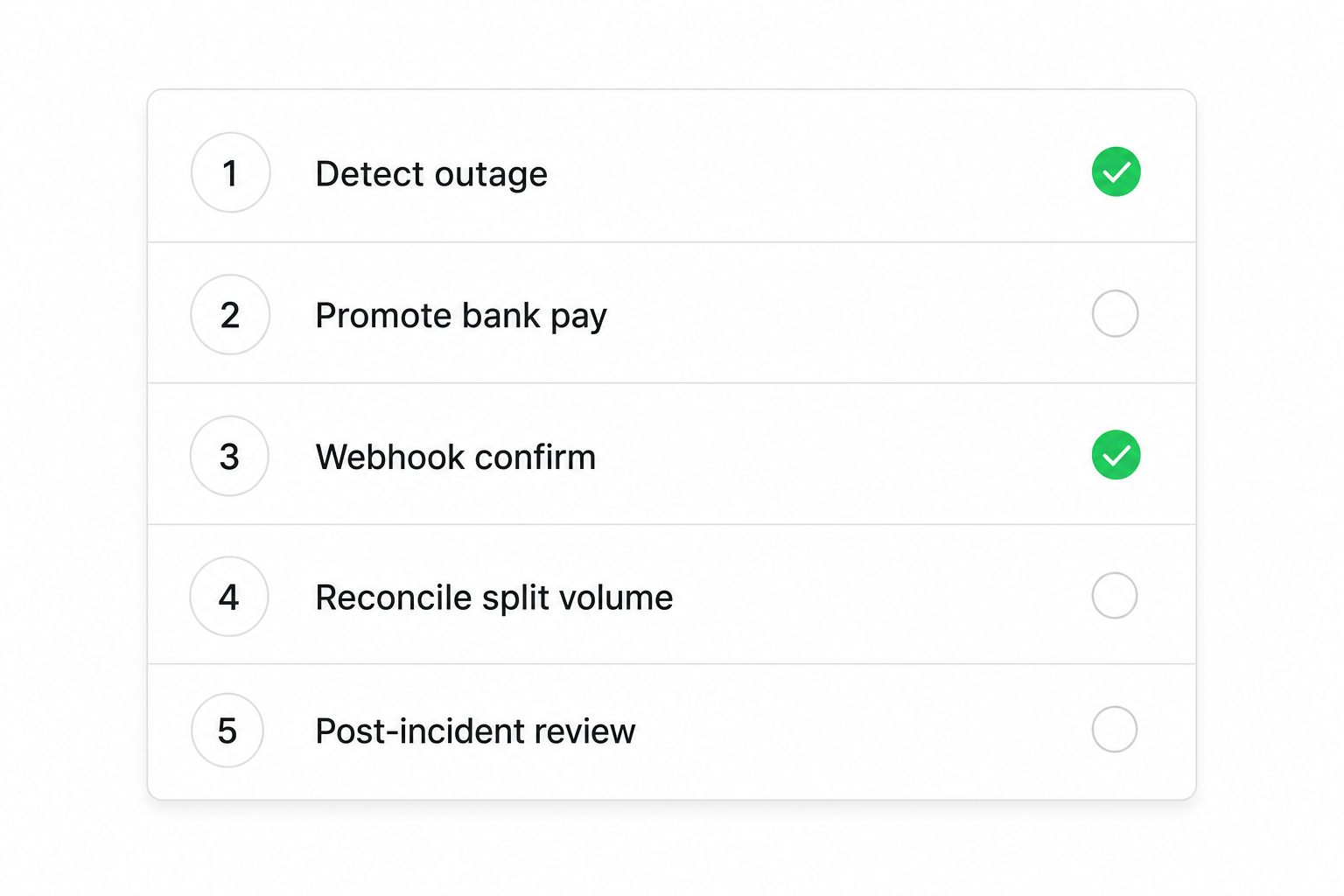

What should a dual-rail resilience playbook include?

Document who does what when authorisations fail — before social media tells you.

1. Detection and comms

- Monitor acquirer status pages and your own authorisation error rate (HTTP 5xx, timeout spikes, decline code clusters).

- Pre-write status banner copy for checkout and confirmation emails: "Card payments temporarily unavailable — pay from your bank app."

- Assign a single incident owner with authority to enable fallback routing without a committee call.

2. Checkout behaviour

- Always show both rails in non-incident weeks so customers know bank pay exists.

- During incidents, promote pay by bank to primary position — do not bury it behind "More options."

- Keep card visible but labelled honestly if you know authorisations are failing ("Cards may be slow — bank pay recommended").

- Never remove card entirely unless you have confirmed hard failure — some issuers still authorise.

3. Technical routing

- Route by health checks on acquirer endpoints where your orchestration layer supports it.

- Fail open to bank pay when card tokenisation or auth endpoints exceed error thresholds.

- Confirm orders on webhooks, not browser return — customers close tabs after bank approval.

4. Ops and finance

- Run a reconciliation shift after incidents — split volume by rail, watch for duplicate captures, and match delayed card settlements against bank-pay spikes.

- Log incident window timestamps for chargeback and complaint analysis later.

5. Post-incident review

- Capture lost revenue estimate (sessions × abandonment delta) and bank-pay uplift.

- Update provider RFP questions — see open banking RFP checklist — with uptime and failover evidence.

Which provider and architecture choices improve resilience?

Resilience is a property of your whole stack — not one checkbox on a feature list.

| Criteria | What to validate | Why it matters for resilience |

|---|---|---|

| Rail independence | PIS provider ≠ card acquirer | Shared vendor means shared outage |

| Bank coverage | Initiation works for top traffic banks per country | Fallback fails if listed banks cannot pay |

| Status transparency | Provider status page + webhook latency SLAs | You cannot promote a rail you cannot see |

| Orchestration | Smart routing rules and health probes | Manual banner flips are too slow at scale |

| Redundancy | Secondary PIS or multi-aggregator option | Provider-side incidents happen too |

| Settlement clarity | Instant vs standard SCT messaging | Ops load spikes when traffic shifts |

Ask providers for historical uptime on initiation APIs and mean time to detect their own incidents — not marketing availability percentages without definitions.

If you operate across UK and EU, remember regulatory and scheme context differs. UK open banking coverage and EU PSD2-style initiation are related but not identical products — validate per market rather than assuming one integration covers every fallback scenario. For market-specific coverage questions, see open banking in Germany as a template for how to test bank lists before you rely on them in production.

When shortlisting vendors, use open banking provider comparison dimensions — coverage, webhooks, sandbox fidelity — and stress-test failover in sandbox before Black Friday, not after the next acquirer incident.

How do you test payment resilience before an outage hits?

Run game days that simulate acquirer failure — not only happy-path checkout QA.

Recommended exercises:

- Kill card in staging — force all sessions to bank pay; measure completion rate and support ticket templates.

- Degraded card mode — inject 50% auth failures; verify orchestration promotes bank pay within one page load.

- Bank-side failure — disable one major bank in sandbox; confirm graceful message and card fallback.

- Webhook-only success — complete bank pay with browser closed; order must still confirm.

- Peak load — replay 2× normal sessions; watch PIS latency under overflow.

Record baseline conversion by rail from pay by bank conversion metrics before the exercise so you can quantify incident impact.

Limitations to accept honestly:

- Game days do not replicate issuer behaviour during real scheme stress.

- Staff training lag — store teams may not know bank pay exists unless you train them.

- Customer habit — first-time bank pay during panic converts worse than familiar repeat use.

What are the trade-offs of promoting pay by bank during card outages?

You gain revenue continuity at the cost of support load and uneven customer experience.

Benefits during incidents:

- Recover some abandoned sessions that would otherwise exit entirely.

- Reduce chargeback exposure on shifted volume — bank-initiated payments follow different dispute paths than cards.

- Demonstrate operational maturity to enterprise buyers auditing your BCP.

Costs and risks:

- Support tickets — "I paid in my bank app but no confirmation" if webhooks lag.

- Partial coverage — customers whose bank is not on your list still cannot pay.

- Reconciliation complexity — finance sees atypical rail mix in one settlement window.

- False confidence — dual rail helps checkout but does not fix in-store terminals on the same acquirer unless POS supports A2A.

Balance promotion with clarity. Overclaiming "always works" during incidents destroys trust faster than honest "cards temporarily down — try bank pay."

Frequently Asked Questions

What is pay by bank payment resilience?

Pay by bank payment resilience means designing checkout so customers can pay from their banking app on infrastructure separate from card acquiring. When acquirers or card schemes fail, a second rail stays available — reducing the chance that every payment method fails at once.

Did pay by bank keep working during the June 2026 Worldpay outage?

Card authorisations on affected Worldpay platforms failed or errored while Worldpay recovered from a third-party power disruption, according to Worldpay's status communications and UK press reports on 23 June 2026. Pay by bank uses different rails — bank apps and payment initiation APIs — so merchants with live bank pay could offer a fallback unrelated to card acquirer recovery timelines.

Should merchants remove cards when the acquirer is down?

No — keep cards visible unless you have confirmed hard failure across all card products. Some authorisations may still succeed on unaffected paths. Promote pay by bank to primary position and label card availability honestly rather than hiding options customers expect.

How is payment resilience different from pay by bank vs card economics?

Economics compares fees, chargebacks, and conversion in normal conditions. Resilience compares what happens when one rail fails — uptime, failover routing, and ops playbooks. You need both analyses: everyday routing rules and incident-mode behaviour.

Can one provider deliver both card acquiring and resilient pay by bank?

Yes, but shared infrastructure reduces independence. Ask whether initiation APIs, acquirer auth, and tokenisation share the same backend. True resilience often means separate PIS and acquirer relationships, or provably isolated failure domains within one group.

How often do card acquirer outages happen?

Major multi-hour outages are infrequent but high visibility — the June 2026 Worldpay incident affected UK retail and hospitality during peak evening traffic. Smaller partial degradations happen more often. Treat resilience as insurance, not daily routing logic.

What is the fastest win for checkout resilience this quarter?

Enable pay by bank alongside cards in your top market, confirm orders via webhooks, and write a one-page incident playbook with pre-approved banner copy. Test once in staging by disabling card auth. That delivers more than adding a third card acquirer nobody switches to automatically.

Conclusion

Pay by bank payment resilience turns card acquirer outages from a hard zero to a managed partial recovery — if you build dual rails before the incident, not during it. The June 2026 Worldpay disruption showed UK merchants how quickly card-only strategies fail under stress; account-to-account pay offers a separate path when banking apps stay online. Invest in visible bank pay, webhook confirmation, orchestration health checks, and game-day tests — then compare providers on coverage and uptime evidence when you expand markets.

Related articles

- Pay by Bank vs Cards at Checkout: Fees & Conversion

Checkout teams in the EU rarely choose a single rail forever. Pay by bank vs card is a trade-off between familiar card UX, interchange economics, dispute workf…

- Pay by Bank Checkout Conversion: EU Patterns That Work

Pay by bank conversion at checkout is the share of buyers who select bank pay and complete authorisation in their banking app. EU teams add pay by bank for low…

- Pay by Bank Explained: How It Works in the EU and UK

Pay by bank is a checkout and payment method where the customer authorises money to move directly from their bank account to yours — usually by logging into th…