Open Banking for iGaming: 8 Use Cases for EU Operators

Licensed EU iGaming operators live and die on two payment moments: getting money in fast when a player wants to bet, and getting winnings out without a support ticket. Open banking for gaming — in practice, iGaming and online gambling (sportsbook, casino, betting), not video-game studios — is how many operators wire those moments through regulated bank rails instead of fighting card acquirer limits alone. Under PSD2 (Payment Services Directive 2), licensed TPPs (Third Party Providers) can initiate payments and read account data with explicit player consent. This article maps eight use cases payments and compliance teams at licensed EU operators deploy today, plus trade-offs, sequencing, and what to ask providers before you integrate.

Open banking for iGaming: The use of regulated PSD2 APIs — PIS (Payment Initiation Service) for deposits and withdrawals, AIS (Account Information Service) for account data, and verification services for onboarding — by licensed online gambling operators to fund player accounts, pay winnings, and support KYC and AML workflows, with explicit customer consent under PSD2.

Why open banking matters for iGaming specifically

iGaming economics are unusually payment-intensive: high deposit frequency, sharp peaks around events, and withdrawal speed that players treat as a product feature. Card acquiring for gambling merchants often carries higher scrutiny, scheme friction, and chargeback exposure than mainstream retail. Account-to-account flows via open banking can offer a different cost and dispute profile — but only where bank UX converts and your provider covers the banks your players actually use.

According to the European Banking Authority, PSD2 governs third-party access to payment accounts; operators still hold gambling licences and AML obligations in each market — open banking feeds those stacks, it does not replace them.

Patterns to keep in mind:

- Deposits and withdrawals are separate product problems — conversion on pay-in, SLA and fraud controls on pay-out.

- SCA (Strong Customer Authentication) applies on initiated payments and fresh AIS consent.

- Coverage is per country and per bank — critical when you hold licences in multiple EU markets.

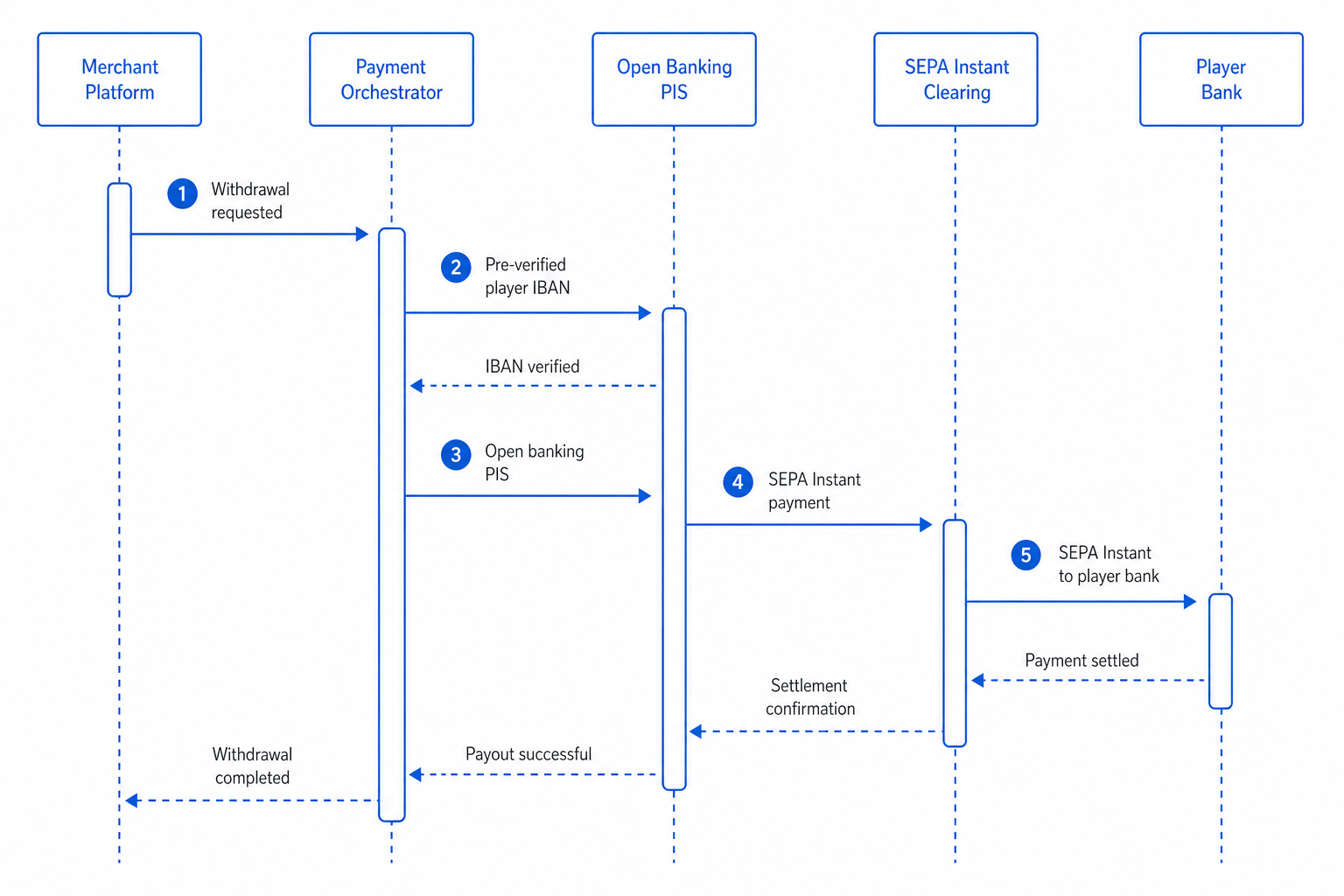

Open banking casino deposits and withdrawals (EU)

Search and product teams often label this open banking casino or open banking gambling — meaning licensed online casino and sportsbook operators, not video-game platforms. The two moments that matter are the same as elsewhere in iGaming: deposit when the player wants to play (Pay by Bank via PIS, wallet credited on bank confirmation) and withdrawal when they cash out (PIS or SEPA to a pre-verified IBAN, with Instant where banks support it).

Operators add bank rails to reduce card acquirer friction and chargeback exposure, but conversion still depends on listing the banks players actually use per licence country. Pair deposit UX with withdrawal SLAs you can meet — promising “instant” payouts where only standard SEPA is available creates more support load than card delays. For rail-level economics and checkout UX, see pay by bank; for engineering vendor selection, see open banking API providers for developers.

1. Instant player deposits with Pay by Bank

The highest-impact open banking for gaming use case is funding the player wallet through Pay by Bank: the player selects their bank, authenticates in the mobile banking app, and authorises an account-to-account deposit via PIS.

Operators typically see:

- Immediate confirmation when the bank returns success — wallet credit without card auth delays

- Variable cost structure versus card interchange on eligible flows

- A payment experience native to mobile — where most iGaming sessions already live

The trade-off is funnel conversion: bank redirects fail silently when bank lists are wrong, desktop flows feel clunky, or fallback rails are hidden. Measure deposit attempt → success by country and device before you scale traffic. For generic checkout rail comparisons (fees, chargebacks, UX), see pay by bank vs cards at checkout — the mechanics overlap even though iGaming compliance context differs.

2. Fast player withdrawals and payouts

Withdrawals are where operators win or lose trust. Payment initiation to a pre-verified player IBAN — often the same account used for deposits — can shorten ops handling versus manual bank-detail entry. Where receiving banks support SEPA Instant Credit Transfer, winnings can land in seconds rather than the next business day.

Instant payout is not universal: bank participation varies, providers route to standard SEPA when Instant is unavailable, and your licence conditions may impose holding periods or manual review thresholds. Product copy should promise what your rail actually delivers per market.

3. Reducing drop-off at the payment step

Homepage promises — instant deposits, less friction — fail when the payment UI does. Open banking drop-off usually clusters around bank selection (too many banks, wrong country default), SCA abandonment, and missing wallet/card fallback for players who will not use a bank redirect.

Treat the deposit step as a owned product surface: clear amounts, operator branding that matches the licence jurisdiction, error messages that suggest the next action, and analytics on bank-level failure rates. Small UX fixes often move conversion more than switching acquirers.

4. Account verification and player KYC at onboarding

Before first deposit or first withdrawal, regulators and operators need confidence the account belongs to the player. AIS-backed verification returns account holder name and IBAN match in an SCA-authenticated step — faster than document upload loops for many players, and a stronger signal than typed bank details alone.

This pairs with identity document checks your compliance team already runs; open banking adds bank-authenticated evidence. For marketplace-style verification patterns, see open banking for e-commerce — the primitive is the same, the licence context is not.

5. AML and source-of-funds checks

Licensed operators must evidence AML and, in many jurisdictions, monitor for unusual patterns consistent with their policies. AIS transaction history — with explicit consent and purpose limitation — gives compliance analysts categorised inflows and outflows to review alongside player behaviour signals.

Open banking does not automate licence obligations or responsible-gambling interventions; it supplies auditable data faster than PDF statement chasing. Legal must sign off consent scope, retention, and whether AIS feeds automated rules or human review queues.

6. Multi-market EU bank coverage

An operator licensed in Malta, with players in Germany, Spain, and Finland, needs banks in each market — not a single “EU” checkbox. One provider integration can aggregate many ASPSPs, but your expansion plan should map licensed territories → supported banks → deposit and withdrawal success rates.

UK open banking and EU PSD2 remain separate stacks post-Brexit; dual-market operators should not assume identical behaviour. Multi-market API strategy for fintech-shaped roadmaps is covered in open banking for fintech; iGaming adds gambling-regulator constraints on top.

7. Cost and dispute profile versus cards

Card deposits on gambling merchants can face interchange premiums, acquirer risk policies, and chargeback/friendly-fraud costs. Authorised open banking push payments follow a different dispute path — no card chargeback scheme once the player completes SCA — which changes ops playbooks, not risk to zero.

Operators still need clear refund policies, self-exclusion integration, and fraud monitoring. The business case is usually blended rails: open banking where it converts, cards or alternative methods where players demand them, with unit economics measured per segment.

8. Reconciliation at high transaction volume

iGaming can generate very high micro-transaction counts per player per month. PIS webhooks plus AIS feeds help finance match internal ledger entries to bank movements without waiting for batched card settlement files. That matters when you reconcile player wallets, bonus wallets, and tax reporting lines across entities.

This use case is operational insurance — it pays off when volume scales and manual matching becomes a headcount problem.

How to choose which use cases to start with

Most licensed operators sequence like this:

- Deposit Pay by Bank in one licensed market with full funnel metrics and card fallback.

- Verification on the same flow so withdrawals reuse a confirmed IBAN.

- Withdrawals with realistic SLA copy and compliance holds documented.

- AIS for AML/compliance once consent architecture is approved.

See also: /blog/open-banking-psd2-explained and /blog/pay-by-bank-vs-cards-for-checkout.

How to evaluate open banking providers for iGaming

Prioritise: PSD2 licensing in every country you accept players from, PIS quality for deposits (redirect, deep link, mobile), payout and SEPA Instant coverage for withdrawals, account verification match rates, webhook reliability, documented bank uptime, EU data residency, and evidence your provider accepts iGaming sector risk on contract. Sandbox parity with production and idempotent payout APIs matter as much as marketing bank counts.

No provider wins every licence footprint — matching depends on player geographies, deposit versus withdrawal mix, and compliance workflow maturity.

Frequently Asked Questions

What is open banking for gaming — and does that mean video games?

In this context, open banking for gaming means iGaming: licensed online betting, casino, and sportsbook operators using PSD2 APIs for player deposits, withdrawals, and compliance-related account data — not video-game platforms or in-game item purchases. The keyword “gaming” is industry shorthand; product and compliance work target regulated gambling operators.

Is open banking legal for licensed iGaming operators in the EU?

Yes, when used through licensed TPPs with player consent for defined purposes. PSD2 governs payment initiation and account access; gambling remains regulated separately in each EU member state. Operators must hold appropriate gambling licences and meet AML requirements — open banking is a technical and data channel, not a substitute for licensing.

What is the difference between AIS and PIS for iGaming?

PIS moves money — player deposits and withdrawals initiated from their bank account. AIS reads account data — balances, transactions, and verified account holder details — for KYC, AML review, and reconciliation. Most operators use both: verify and understand via AIS, fund and pay out via PIS.

Can open banking improve withdrawal speed for players?

It can, when payouts run to a pre-verified IBAN over SEPA Instant-capable banks and your provider routes Instant successfully. Speed still depends on compliance review queues, licence rules on holding periods, and receiving-bank participation — not on open banking alone.

How does open banking compare to cards for casino deposits?

Cards remain familiar to many players; open banking can reduce certain costs and change dispute dynamics on authorised account-to-account deposits. Conversion varies by market and device; most operators offer multiple rails and optimise by segment rather than forcing one method.

How do I evaluate open banking providers for an iGaming platform?

Map your licensed player countries to bank coverage, test deposit conversion and withdrawal success in sandbox and pilot, review contract acceptance of gambling sector activity, and validate verification, Instant payout, webhook, and SLA terms. Align commercial pricing with projected deposit and withdrawal volumes before full rollout.

Closing thought

Open banking for iGaming is a regulated toolkit for the moments players care about most — funding the account and cashing out winnings — plus the compliance evidence your licence expects. Licensed operators that win treat deposits, withdrawals, and KYC as one connected flow, measure bank-level performance honestly, and expand markets only where connectivity and regulation align. Your licence footprint, player geographies, and risk appetite determine which of these eight use cases to ship first.

Related articles

- Open Banking for Payroll: Disbursement & Verification

Payroll platforms lose trust when salaries land late or on the wrong account. Open banking for payroll providers connects verification and disbursement to regu…

- Open Banking for Online Casinos: EU Deposits & Compliance

Licensed online casino operators lose players when deposits fail at the card gateway and when withdrawals sit in manual review. Open banking casino flows — pay…

- Open Banking for Marketplaces: 8 Use Cases for EU Platforms

Two-sided platforms live on money moving twice: collect from buyers, hold or route platform fees, pay sellers on time. Cards work until interchange, chargeback…