Open Banking Providers Nordics: Coverage Guide (2026)

Open banking providers nordics buyers care about one thing first: whether pay by bank and account verification work on the banks their customers actually use in Denmark, Sweden, Norway, and Finland — not whether a vendor paints “Nordics” on a map. Nordic markets combine strong digital banking, local scheme habits, and coverage that diverges from “EU average” benchmarks. This guide explains why the region is different, what to validate per country, and how to evaluate providers without naming a default winner.

Open banking coverage nordics: The set of banks and payment rails your provider reaches in Denmark, Sweden, Norway, and Finland for payment initiation, account information, and verification — validated per institution, not per region label.

Why do the Nordics differ from EU-wide open banking averages?

Nordic consumers already bank on mobile. That raises the bar for redirect UX, app deep links, and business-account behaviour — flows that look fine in a continental sandbox may fail on a Swedish savings bank or a Danish business account.

Country-specific factors:

- Denmark — high digital adoption; validate both retail and business accounts your B2B traffic uses

- Sweden — large institution diversity; mobile-first authentication patterns dominate

- Norway — strong local banks; coverage lists rarely match generic “EU” exports

- Finland — often bundled in Nordic RFPs but with its own institution mix

A provider strong in Germany is not automatically strong in open banking Sweden or open banking Denmark — test each market you sell into. For Germany-specific evaluation patterns, see open banking in Germany as a contrast, not a substitute.

What coverage dimensions should you compare per country?

Which open banking providers offer the best coverage in the nordics is the wrong first question. Ask: best for my bank list and use case.

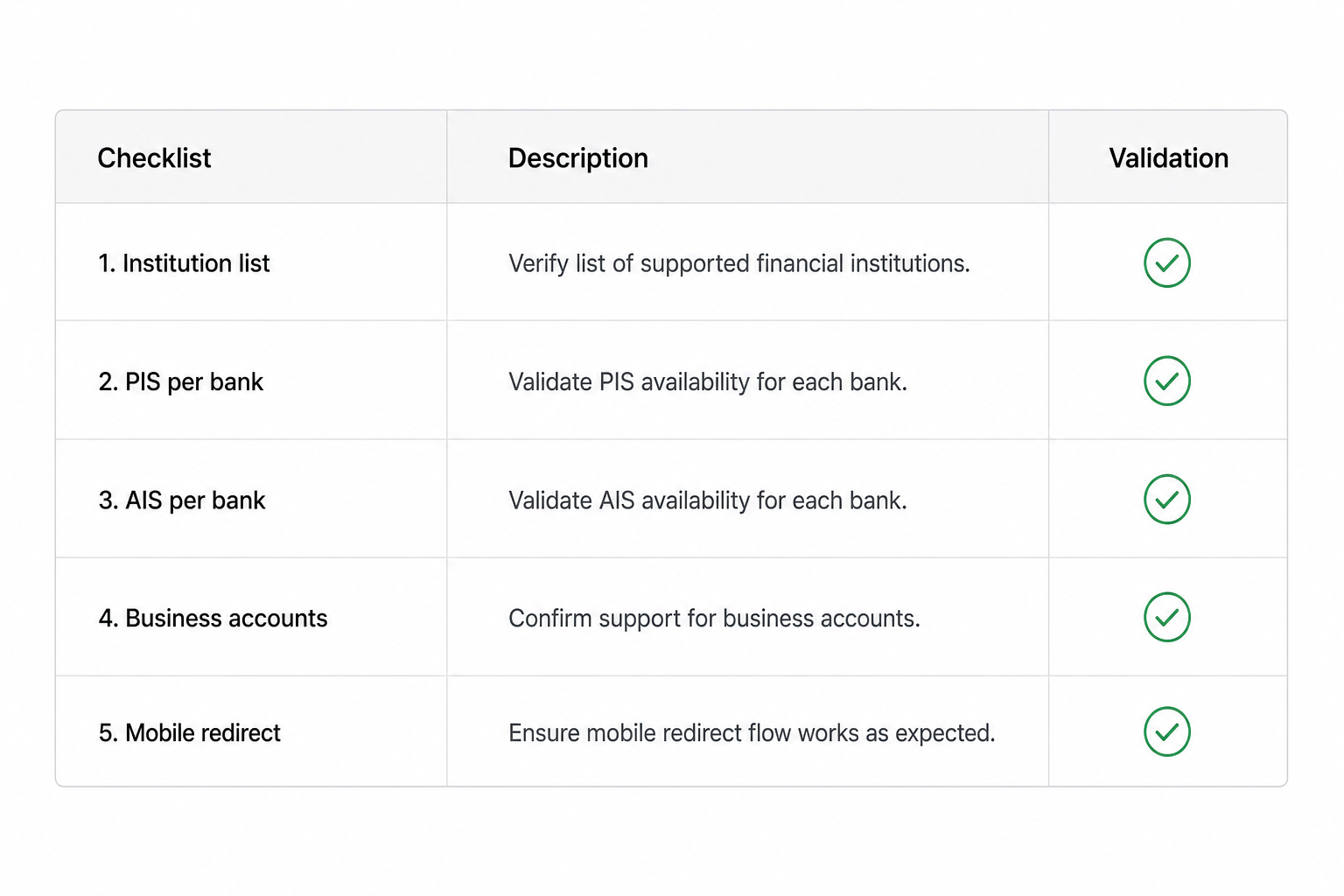

| Dimension | What to verify | Why it matters |

|---|---|---|

| Institution list | Named banks per DK/SE/NO/FI | Marketing “Nordics” hides gaps |

| Initiation vs data | PIS and AIS per bank | Verification without pay, or both |

| Business accounts | Separate testing | B2B flows differ from retail |

| Instant / local rails | Where you promise speed | Settlement messaging varies |

| Mobile UX | App vs desktop redirect | Most Nordic traffic is mobile |

Request exports filtered by country code and product, then run the same sandbox scripts in each market.

Which use cases drive Nordic open banking adoption?

Common bank api eu and Nordic deployments cluster around:

- Pay by bank checkout — e-commerce and marketplaces with high card costs

- Account verification — onboarding, lending, marketplace sellers

- Recurring collection — subscriptions and instalments where VRP or standing patterns exist

- Payouts — refunds and marketplace splits with verified IBAN

Match use case to rail: initiation for money movement, account information for verification. See AIS vs PIS in open banking if your team splits ownership between risk and payments.

How do you evaluate open banking providers for Nordic banks?

Run a two-market minimum pilot before you sign Nordic-wide claims:

Week 1 — lists and sandbox

- Send identical RFP appendix to finalists: DK/SE/NO/FI institution exports for your use case

- Test top five banks per country from your analytics on mobile

- Log success rate, latency, and webhook delivery

Week 2 — scorecard

- Weight coverage on your banks highest (30–40%)

- Add conversion, API/webhooks, commercial model, support

- Document per-country gaps — one “Nordic winner” rarely wins every bank

Use open banking provider comparison for the wider framework and how to shortlist open banking providers for workshop steps.

Frequently Asked Questions

What are open banking providers nordics?

They are licensed third-party providers and aggregators that connect your product to Nordic banks for payment initiation, account data, or verification — scope and bank lists vary by vendor.

How is open banking coverage nordics measured?

By named institutions per country and per rail (initiation vs data), tested in sandbox on the accounts your customers use — not by a single regional percentage.

Which open banking providers offer the best coverage in the Nordics?

There is no universal best: coverage is bank-specific. Shortlist providers against your mandatory list in DK, SE, NO, and FI, then compare sandbox evidence.

Is open banking Sweden different from open banking Denmark for providers?

Yes — institution mix, mobile UX, and business-account behaviour differ. Evaluate each country separately even when vendors sell a “Nordic package.”

Do Nordic open banking APIs differ from EU PSD2 APIs?

The regulatory frame is familiar, but bank implementations and local schemes differ. Treat Nordics as their own coverage project, not an automatic extension of Germany or France rollouts.

How does this relate to bank API EU strategies?

Many teams start with EU-wide RFPs then discover Nordic gaps. Add DK/SE/NO/FI bank lists to any bank api eu evaluation before go-live.

Conclusion

Open banking providers nordics selection is bank-list discipline across Denmark, Sweden, Norway, and Finland — mobile UX, business accounts, and initiation-vs-data splits included. Build per-country evidence, then compare finalists with the same scorecard you use elsewhere in the EU. When requirements are clear, use the provider directory to align capability tags with your shortlist.

Related articles

- Open Banking UK vs EU: What B2B Teams Need to Know

Your product roadmap probably mentions "Europe" as one market — but open banking UK vs EU is not a single integration. UK and EU buyers use different bank apps…

- Open Banking in Germany: Coverage and Provider Fit

Germany is where many EU payment roadmaps start — large banked population, strong mobile banking, and high B2B invoice volume — yet “open banking Germany” on a…

- Recurring Pay by Bank: UK Variable Billing on Bank Rails

Billing teams lose margin when every renewal runs on a card that expires, and they lose days of cash visibility when Direct Debit returns land late. Recurring…