Open Banking Subscription Billing: UK & EU Bank-Rail Renewals

Subscription revenue bleeds when renewals depend on cards that expire, chargebacks that eat margin, or mandates that cannot match a variable invoice. Open banking subscription billing lets you verify the account once, store consent or a mandate, and pull renewals on bank rails — with different mechanics in the UK (commercial variable recurring payments under UKPI) and the euro area (SEPA Direct Debit after verification). This guide maps the setup flows, dunning differences, and provider checks billing and product teams need before you promise bank-pay renewals to customers.

Open banking subscription billing: Collecting repeat subscription charges from a customer's bank account after one setup step — bank-app consent in the UK or a SEPA mandate in the euro area — instead of storing a card number. You get lower variable cost on many flows, fewer expiry-driven failures, and clearer IBAN-level reconciliation for finance.

Why are billing teams looking at bank rails for subscriptions?

Bank-rail renewals cut involuntary churn from expired cards and interchange on every successful cycle when your unit economics are tight. A SaaS plan at €30/month or a gym membership at £40/month may lose more margin to card fees than the ops team expects — especially at scale.

Open banking does not remove failed payments. Customers still run out of funds or revoke consent. What changes is the failure profile: no card replacement cycle, different retry windows, and reconciliation tied to IBAN references instead of last-four digits.

Teams pilot bank subscription billing when:

- Margin pressure — recurring revenue where interchange is a visible line item

- UK variable billing — usage-based or tiered plans where commercial variable recurring payments (cVRP) fits the sector

- EU B2B contracts — customers prefer paying from operating accounts with audit-friendly references

- Churn reduction — card-on-file expiry drives support tickets you want to shrink

Keep cards as fallback while you prove bank enrollment rates in your top markets.

How does open banking subscription billing work in the UK?

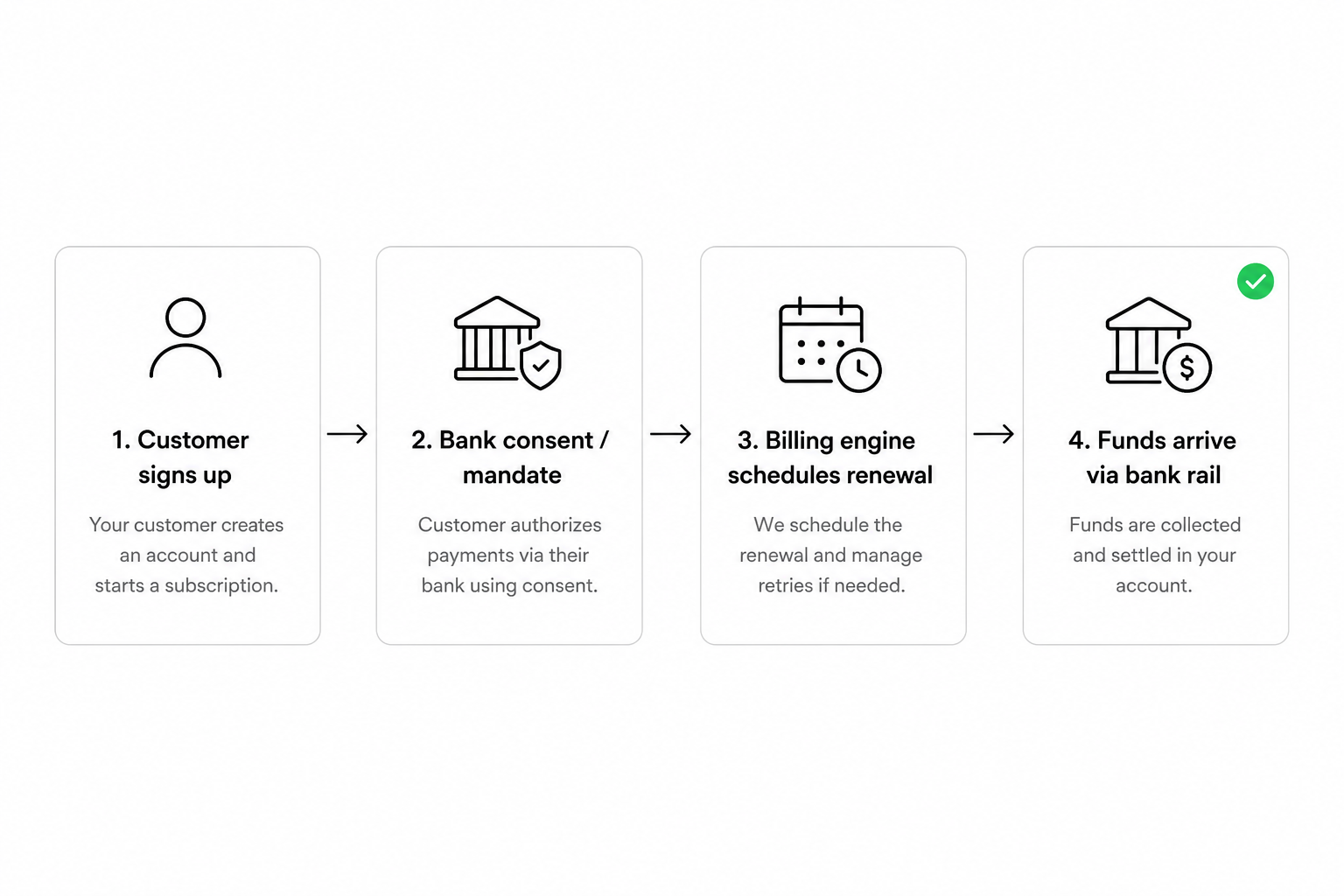

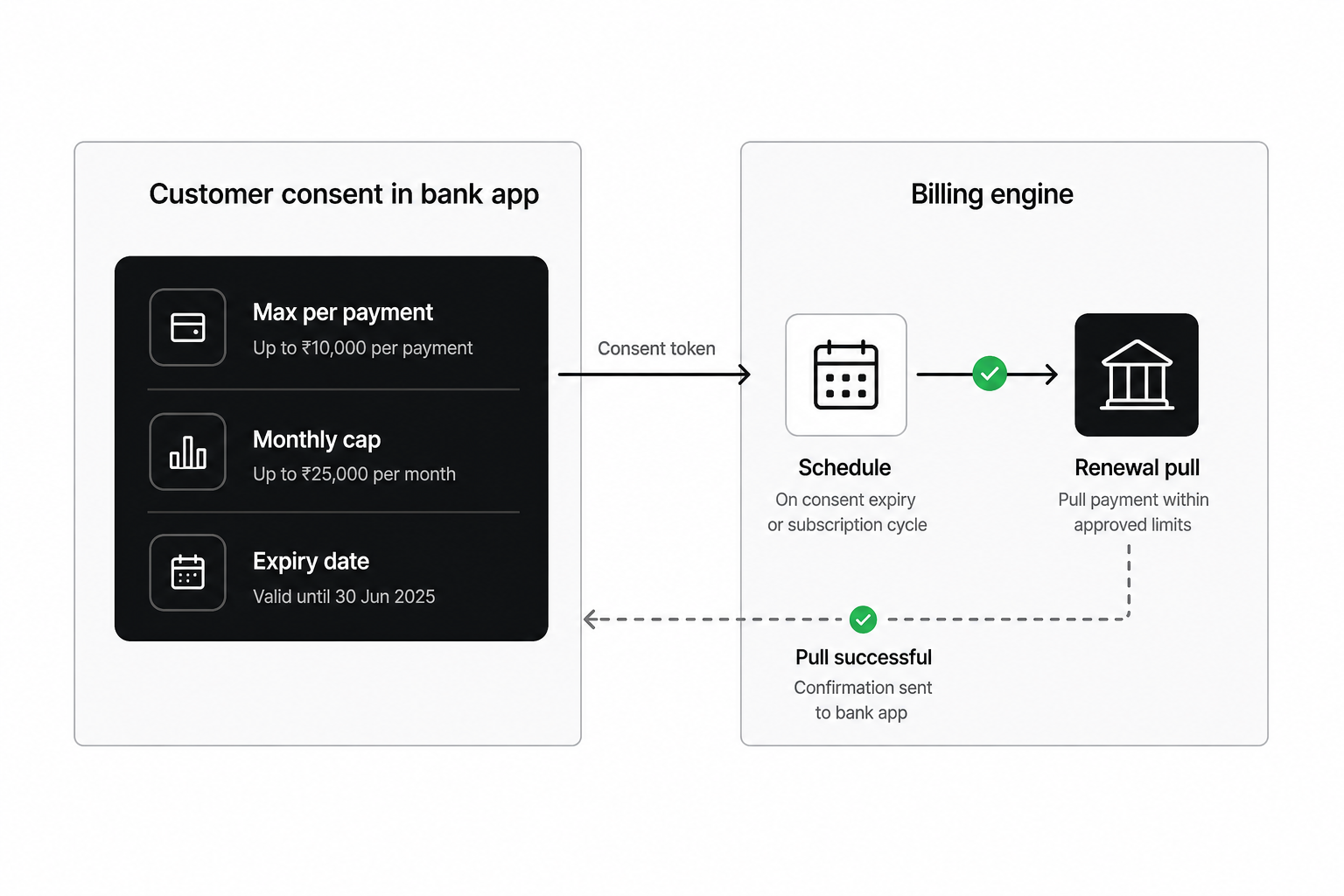

In the UK, subscription billing on bank rails typically follows a consent-first model: the customer approves your business in their banking app with caps on amount and duration, then your provider requests each renewal within those limits.

The UK Payments Initiative (UKPI) commercial scheme launched in June 2026 with Wave 1 sectors — regulated utilities, telecoms, financial services, government, and charities — before broader retail and general subscriptions in Wave 2 (expected later in 2026). If you run a generic B2C SaaS or streaming product, confirm Wave 2 eligibility before marketing bank-pay renewals UK-wide.

Typical UK flow

- Customer selects pay-by-bank at signup or billing portal

- Redirect to mobile or online banking to approve you (per-payment cap, monthly cap, expiry)

- Your billing engine schedules pulls against that consent

- Provider webhooks confirm success or failure; finance matches on creditor reference

This is the operational backbone behind bank on file — consent stored at the bank, not a PAN token. See variable recurring payments for the technical distinction between sweeping (own-account) and commercial collection.

Trade-offs in the UK

- Sector gates apply under UKPI Wave 1 — do not assume every subscription merchant qualifies today

- Balance checks before pull reduce blind failures but depend on bank and provider support

- Dispute paths differ from card chargebacks — train support on bank-scheme rules

How does subscription billing work in the EU?

Euro-area teams rarely have a single product labelled "VRP for subscriptions." The practical stack is verify the account, collect the first payment if needed, then run SEPA Direct Debit for renewals — sometimes after a pay by bank checkout that confirms the IBAN.

Typical EU flow

- Customer completes pay-by-bank checkout or account verification during signup

- You capture a SEPA Direct Debit mandate (paperless where supported)

- Billing engine submits collections on schedule; amendments follow SDD rules for amount changes

- Webhooks and bank reports feed reconciliation

Variable SaaS tiers or usage billing may require mandate amendment notices or a hybrid where the base fee runs on SDD and overages trigger one-off pay-by-bank. There is no EU-wide commercial VRP scheme equivalent to UKPI yet — national schemes and provider capabilities differ.

| Dimension | UK (cVRP / UKPI path) | EU (SEPA Direct Debit stack) |

|---|---|---|

| Setup UX | Bank-app consent with caps | Mandate + verification |

| Variable amounts | Designed for varying pulls within limits | Amendment rules; provider-dependent |

| Settlement speed | Faster Payments (often same day) | SDD batch timelines |

| Sector eligibility | UKPI Wave 1 sectors first | Broad if mandate rules met |

| Disputes | Bank/scheme model | SDD refund windows |

For vertical context, see open banking for SaaS platforms — the billing mechanics here apply across B2B software, memberships, and digital subscriptions.

What changes in your billing stack and dunning?

Switching or augmenting with bank rails is not a PSP toggle. Your subscription platform must handle consent revocation webhooks, failure codes that differ from card declines, and reference fields finance expects on bank statements.

Billing engine requirements

- Store provider consent or mandate IDs alongside customer records

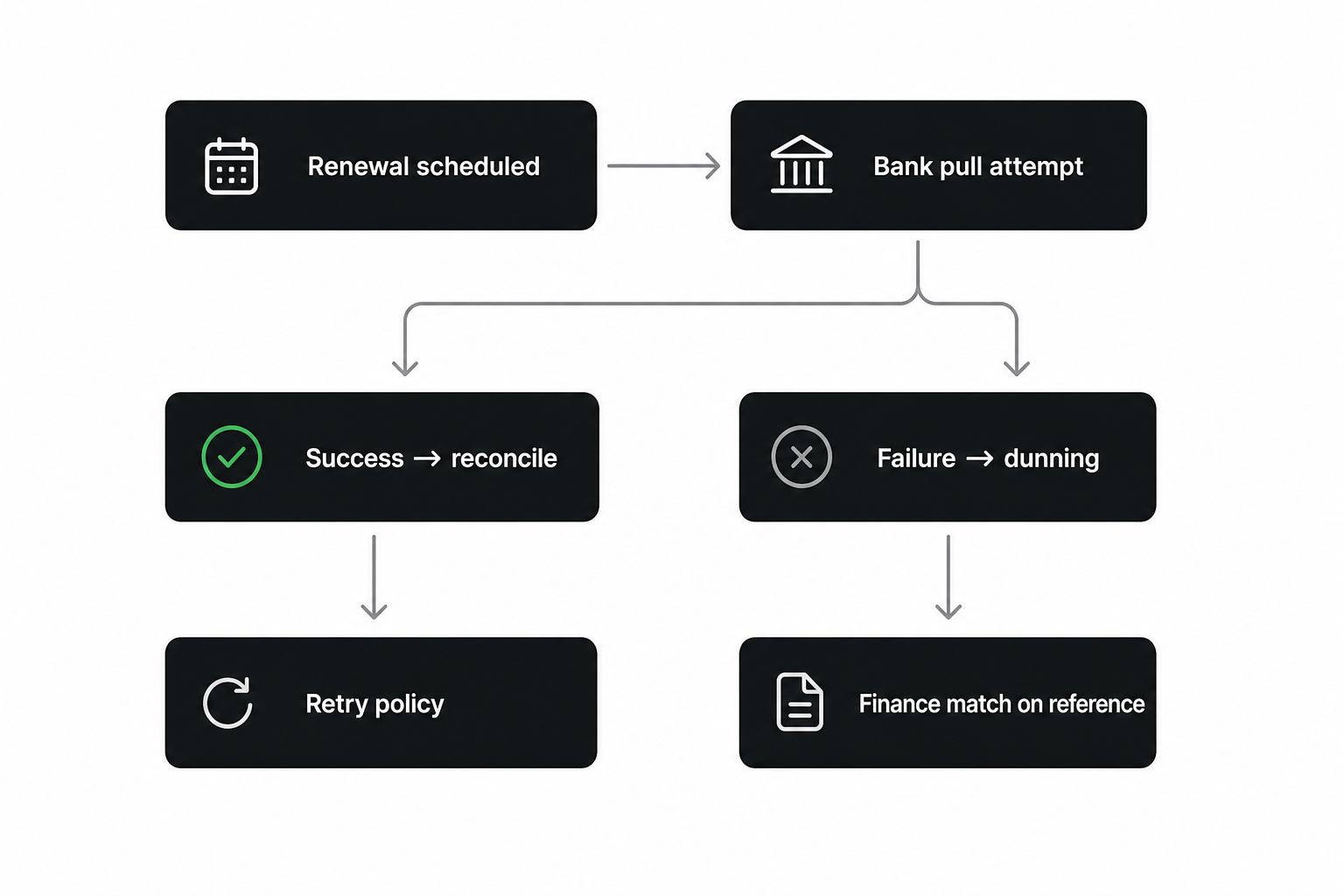

- Map bank failure reasons to dunning tiers (hard vs soft retry)

- Support partial migrations — bank-primary with card backup for customers who fail enrollment

- Emit deterministic creditor references for ERP matching

Dunning differences

Card dunning often retries on day 1, 3, 7 with the same token. Bank pulls may need longer spacing under scheme rules, and "insufficient funds" may be visible earlier if balance checks run pre-pull. Copy customer emails in plain language — "update your payment in your banking app" not acronym-heavy notices.

Reconciliation

Finance teams prefer bank subscription billing when statement lines include your merchant descriptor and a unique reference per invoice. Validate webhook payloads in sandbox with your exact amount patterns (e.g. €9.99 vs €10.00 rounding) before launch.

How do you evaluate providers for subscription billing?

No single checklist fits every market. Compare providers on coverage in countries where you bill, recurring rail support, and webhook quality before commercial terms.

| Criterion | What to validate |

|---|---|

| Recurring model | UK cVRP / commercial VRP vs SEPA DD vs hybrid |

| Variable amounts | Caps, amendment flows, usage billing fit |

| Bank coverage | Your top enrollment countries and customer banks |

| Consent UX | Mobile banking redirect completion rates in sandbox |

| Webhooks | Success, failure, revocation events with references |

| Sandbox parity | Test expiry, insufficient funds, mandate cancel |

| Incident response | Status during month-end billing peaks |

Run production-shaped tests: signup, first renewal, amount change, voluntary cancel, and forced failure. Read recurring transactions via open banking for rail-specific criteria, then use the provider-matching form to compare live coverage and recurring support for your billing countries — or start from the provider comparison guide for evaluation dimensions.

Frequently Asked Questions

What is open banking subscription billing?

Open banking subscription billing is collecting repeat charges from a customer's bank account after an initial setup — bank-app consent in the UK or a SEPA Direct Debit mandate in the euro area — instead of storing a card. It targets lower variable cost and fewer card-expiry failures while keeping customer control in their banking app.

Can open banking replace card-on-file for subscriptions?

It can for eligible customers and markets, but most teams run a hybrid: bank rails for segments where enrollment and sector rules allow, cards as fallback. UK general B2C SaaS may need to wait for UKPI Wave 2; EU teams typically pair verification with SEPA Direct Debit rather than flipping every subscriber at once.

How is UK cVRP different from EU subscription billing?

UK commercial variable recurring payments use open-banking consent with amount caps under the UKPI scheme — settlement on Faster Payments. EU subscription billing usually relies on SEPA Direct Debit mandates with scheme rules on amendments and batch timing. The customer experience and ops playbooks differ; do not assume one integration covers both.

Do open banking subscriptions support variable or usage-based pricing?

Yes, within limits. UK cVRP is designed for varying amounts inside customer-approved caps. EU usage billing often combines SDD for a base fee with pay-by-bank for overages, or follows mandate amendment processes. Confirm with your provider before promising unlimited amount flexibility.

What causes involuntary churn on bank subscription billing?

Insufficient funds, revoked consent or cancelled mandates, and sector or bank coverage gaps — not card expiry. Dunning logic should treat bank failures separately from card retries, with copy that directs customers to their banking app when consent needs renewal.

How do I choose a provider for subscription billing?

Compare bank coverage in your billing countries, support for your recurring model (fixed vs variable), webhook fields for reconciliation, sandbox tests on failure and revocation paths, and incident transparency. Pilot one product corridor before a full migration announcement.

Conclusion

Open banking subscription billing gives finance and product teams a path to lower per-renewal cost and fewer card-expiry failures when bank enrollment and scheme eligibility align with your customer base. The implementation split is geographic: UK teams track UKPI Wave 1 vs Wave 2 sector access and cVRP consent limits; EU teams build verify-then-SEPA-DD stacks with amendment rules for variable plans. Measure enrollment rate, pull success, and reconciliation time in a pilot corridor — then expand with cards as backup, not as an afterthought.

Related articles

- cVRP Explained: Commercial Variable Recurring Payments

cVRP stands for Commercial Variable Recurring Payments — a UK way to collect repeat payments straight from a customer’s bank account after they approve once in…

- Bank on File vs Card on File: EU & UK Recurring Billing

Recurring revenue depends on a stored funding method you can charge again without asking the customer to re-enter details every cycle. Card on file is the defa…

- Variable Recurring Payments (VRP) for EU and UK Teams

Subscription and usage billing breaks when every renewal needs a new card authorisation or a fixed direct debit that cannot match the invoice. Variable recurri…