Open Banking for Travel: 8 Use Cases for EU Airlines & OTAs

A single long-haul booking or packaged holiday can run to thousands of euros — yet most EU airlines and OTAs still absorb card interchange and chargeback risk on every ticket sold. Open banking travel is how many operators shift high-value checkout and refunds onto regulated account-to-account rails: under PSD2 (Payment Services Directive 2), licensed TPPs (Third Party Providers) initiate payments and read account data with explicit customer consent. This article maps eight use cases payments and product teams at airlines, OTAs, tour operators, and travel agencies deploy today, plus trade-offs, sequencing, and what to ask providers before you integrate.

Open banking for travel: The use of regulated PSD2 APIs — PIS (Payment Initiation Service) for customer payments and refunds, AIS (Account Information Service) for account data, and verification services — by airlines, OTAs, and travel merchants to collect booking payments, issue tickets after confirmation, process cancellations, and support fraud and finance operations, with explicit customer consent under PSD2.

Why open banking matters for travel specifically

Travel payments are shaped by high average order value, tight issuance deadlines, and refund volume when plans change. Card interchange scales with ticket price — a meaningful line item at €800 or €2,000 per booking. Chargebacks from disputes, cancellations, or fraud add ops cost on top. Open banking payment initiation can change the unit economics and dispute profile on eligible flows, but only where bank UX converts and your provider covers the banks your travellers use.

According to the European Payments Council, account-to-account payments can confirm in seconds where participating banks support instant schemes — relevant when you must release a seat or room only after funds are sure.

Patterns to keep in mind:

- Payment confirmation gates ticketing — PIS success webhooks should drive PNR or voucher issuance, not the other way around.

- SCA (Strong Customer Authentication) applies on every initiated payment and fresh AIS consent.

- Refunds are a product promise — schedule changes and cancellations need a rail you can operate at scale.

1. Pay by Bank for high-value bookings

The core open banking travel use case is checkout: the traveller selects Pay by Bank, authenticates in their banking app, and authorises payment for flights, hotels, or packages via PIS. For high-AOV baskets, the economics versus card interchange often get serious attention in finance reviews — especially when card fees are quoted as a blended rate across mixed domestic and cross-border traffic.

Product requirements differ from low-ticket retail: show the exact amount, operator legal entity, and booking reference in the bank payment screen; support mobile-first flows where most travel is booked; keep card and wallet fallback for travellers who will not use a bank redirect. For a structured comparison of fees, chargebacks, settlement, and conversion, see pay by bank vs cards at checkout.

2. Lower processing cost on large transactions

Interchange and acquirer fees compound on expensive itineraries — multi-sector trips, business class, or family bookings. Open banking is typically priced per successful transaction without card interchange, which shifts the breakeven point upward as basket size grows.

Model all-in cost including failed attempts, retries, and manual ops — not headline PIS pricing alone. Savings should be validated on your actual route mix and domestic versus intra-EU share, not assumed from a single market benchmark.

3. Chargeback and dispute profile

Card chargebacks are a known pain in travel — friendly fraud, service disputes after cancellation, and scheme reason codes that tie up finance teams. Authorised account-to-account payments completed with SCA do not follow card chargeback schemes; dispute handling routes differently, often through bank complaint processes.

That changes risk reporting and support playbooks — it does not eliminate customer complaints or regulatory obligations on refunds. Clear fare rules, refund SLAs, and payment descriptors in the bank app reduce confusion at the source.

4. Instant payment confirmation before ticketing

Airlines and OTAs usually cannot issue a ticket on promise — they need confirmed funds. PIS returns a deterministic success or failure from the payer bank; wired correctly, your booking engine issues the PNR or voucher on webhook, not on redirect alone (redirects can be abandoned after authorisation).

Latency targets matter for hold timers: if a fare lock expires in fifteen minutes, bank redirect plus SCA must fit inside the window with buffer for slow ASPSPs. Load-test peak booking periods, not only happy-path sandbox banks.

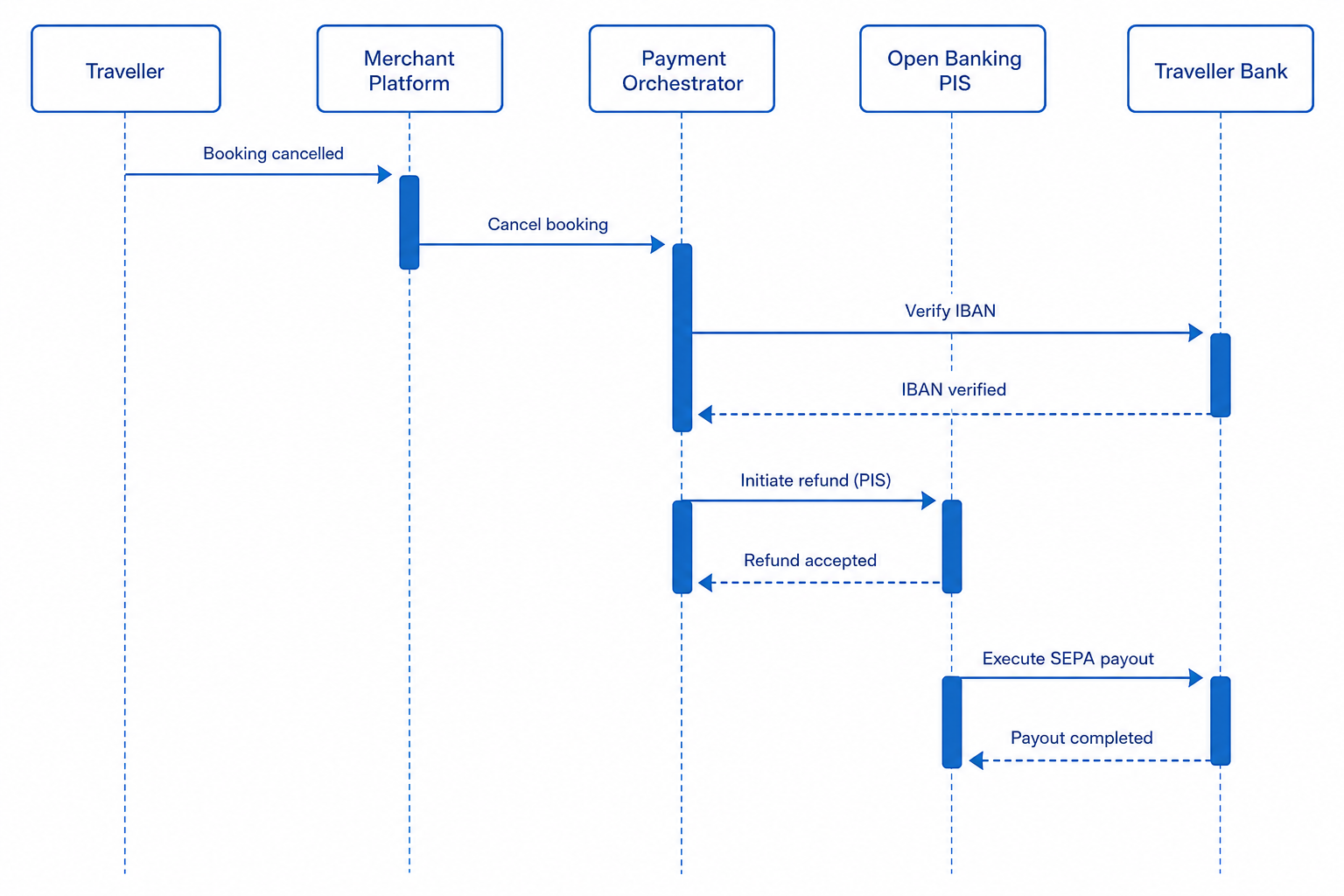

5. Refunds, cancellations, and schedule changes

When itineraries change, money must flow back — full refund, partial credit, or airline-invoked cancellation. Payment initiation to a verified customer IBAN (often captured at booking) can be faster to execute than card reversals subject to scheme timing and partial-match issues.

SEPA Instant Credit Transfer can accelerate refunds where receiving banks participate; otherwise standard SEPA timelines apply. Ops teams should align customer communications with actual rail speed — "instant refund" copy fails when compliance review or bank cut-offs delay payout.

6. Cross-border EU traveller payments

A German OTA selling to French, Dutch, and Spanish customers needs banks in each market — not a generic EU label. One provider integration can reach many ASPSPs, but coverage maps should be checked per country before marketing Pay by Bank as a primary method.

UK open banking and EU PSD2 remain separate technical and regulatory stacks; operators selling across both need dual readiness. Multi-market connectivity patterns for platform businesses are covered in open banking for fintech; travel adds issuance deadlines and refund regulation on top.

7. Fraud prevention and account verification

High-value bookings attract fraud — stolen cards, synthetic identities, and mis-keyed payout details for refund abuse. AIS-backed verification confirms account holder name against IBAN before you store payout instructions or release tickets on first purchase.

This complements 3-D Secure on cards rather than replacing broader fraud strategy. Verification at booking also reduces wrong-IBAN refunds that become contact-centre work during disruption events.

8. Reconciliation and finance operations

Travel demand is seasonal — peaks around holidays and school breaks spike transaction counts. PIS webhooks plus AIS feeds help finance match booking references to bank movements without waiting for batched card settlement files.

For groups selling across brands or entities, reconciliation complexity multiplies; open banking metadata (IBAN, reference, timestamp) should map cleanly to your order ledger. AIS does not replace ERP — it shortens the gap between bank statement and booking system.

How to choose which use cases to start with

Most travel merchants sequence like this:

- Pay by Bank on high-AOV routes — one market, measurable conversion versus card, with fallback live.

- Ticketing gated on PIS confirmation — engineering and ops aligned on failure handling.

- Refunds to verified IBAN — especially if cancellation volume is high.

- Expand bank coverage for additional traveller countries once core flows are stable.

See also: /blog/open-banking-psd2-explained and /blog/pay-by-bank-vs-cards-for-checkout. Optional cross-read: open banking for e-commerce for marketplace payout patterns that parallel large OTAs.

How to evaluate open banking providers for travel

Prioritise: PSD2 licensing in countries you sell into, PIS reliability for high-value checkout, webhook and idempotency design for ticketing, refund and SEPA Instant coverage, account verification quality, documented bank uptime by market, EU data residency, and contractual acceptance of travel sector activity. Sandbox banks should mirror production countries you care about — not only one domestic market.

Provider fit depends on airline direct versus OTA marketplace model, refund volume, and traveller geography — not a single leaderboard.

Frequently Asked Questions

What is open banking for travel companies?

Open banking for travel is the use of regulated PSD2 APIs by airlines, OTAs, and travel merchants to collect booking payments, confirm funds before ticketing, process refunds, and support verification and reconciliation — with customer consent. Most integrate through a licensed TPP rather than connecting to each bank directly.

Is open banking legal for airlines and OTAs in the EU?

Yes, when used through licensed providers with customer consent for defined purposes. PSD2 governs payment initiation and account access; travel consumer law and carrier obligations still apply to refunds and cancellations. You do not need your own TPP licence if you partner with a regulated AISP or PISP.

What is the difference between AIS and PIS for travel use cases?

PIS moves money — customer payments for bookings and outbound refunds. AIS reads account data — balances, transactions, and verified account holder details — for fraud checks and finance reconciliation. Many programmes use both: verify via AIS at booking, collect and refund via PIS.

Can open banking reduce chargebacks on flight bookings?

Authorised account-to-account payments do not use card chargeback schemes, which changes dispute handling and cost profile on those flows. Customer complaints and refund rights under travel regulation still apply — open banking is not a substitute for clear policies and ops.

How does Pay by Bank conversion compare to cards for expensive trips?

Conversion depends on market, device, traveller bank, and how prominently Pay by Bank is offered versus cards and wallets. High-AOV travellers may prefer cards for loyalty points; others prefer bank app authorisation. Most operators run both and optimise by segment and route.

How do I evaluate open banking providers for a travel platform?

Map traveller countries to bank coverage, test high-value checkout and refund paths in sandbox and pilot, review webhook SLAs for ticketing, confirm Instant refund routing, validate verification match rates, and align commercial terms with seasonal volume forecasts before full rollout.

Closing thought

Open banking for travel targets the payments problems that scale with ticket price — interchange, chargebacks, confirmation before issuance, and refunds when plans change. Airlines and OTAs that succeed start with a narrow high-AOV experiment, measure bank-level conversion and refund ops honestly, and expand markets only where connectivity supports the promise. Your route network, traveller mix, and refund policy determine which of these eight use cases to prioritise first.

Related articles

- Open Banking for Payroll: Disbursement & Verification

Payroll platforms lose trust when salaries land late or on the wrong account. Open banking for payroll providers connects verification and disbursement to regu…

- Open Banking for Online Casinos: EU Deposits & Compliance

Licensed online casino operators lose players when deposits fail at the card gateway and when withdrawals sit in manual review. Open banking casino flows — pay…

- Open Banking for Marketplaces: 8 Use Cases for EU Platforms

Two-sided platforms live on money moving twice: collect from buyers, hold or route platform fees, pay sellers on time. Cards work until interchange, chargeback…