Open Banking API Integration: EU B2B Playbook

Open banking API integration is how your product connects to regulated bank rails without building hundreds of bank adapters yourself. Done well, you ship pay by bank, account verification, or recurring collection in weeks — with webhooks that match your ledger and consent flows customers recognise. Done poorly, you burn engineering on sandbox quirks, duplicate payments, and finance teams chasing unmatched references. This playbook walks EU B2B payments and product leads through scoping, testing, and production rollout so the first live flow is measurable, not a science project.

Open banking API integration: Connecting your application to a licensed provider's API so customers can pay from their bank, verify an account, or share transaction data with consent — without you maintaining direct links to every EU institution. Your code handles user journeys and ledger mapping; the provider handles bank connectivity, regulatory packaging, and scheme updates.

What should you scope before starting an open banking API integration?

Pick one user story and one corridor before you write integration code. "Open banking everywhere" is how teams stall in sandbox for quarters. A tight v1 scope sounds like: UK pay-by-bank checkout, German account verification for onboarding, or Netherlands recurring collection for subscriptions — not all three at once.

Write the scope as outcomes your finance team can reconcile:

- Initiation — customer pays from bank; you receive settled or authorised status via webhook

- Verification — you confirm account holder and IBAN before first payout or invoice

- Data — you read categorised transactions for affordability or matching (with refreshed consent)

Map each outcome to countries, banks that matter for your ICP, and failure modes (insufficient funds, user cancel, timeout). If you have not decided buy vs build yet, read build vs buy open banking first — most teams integrate a provider rather than direct ASPSP links for v1.

When you are ready to compare providers against that scope, use the provider-matching form to filter on markets, use cases, and volume before deep technical review.

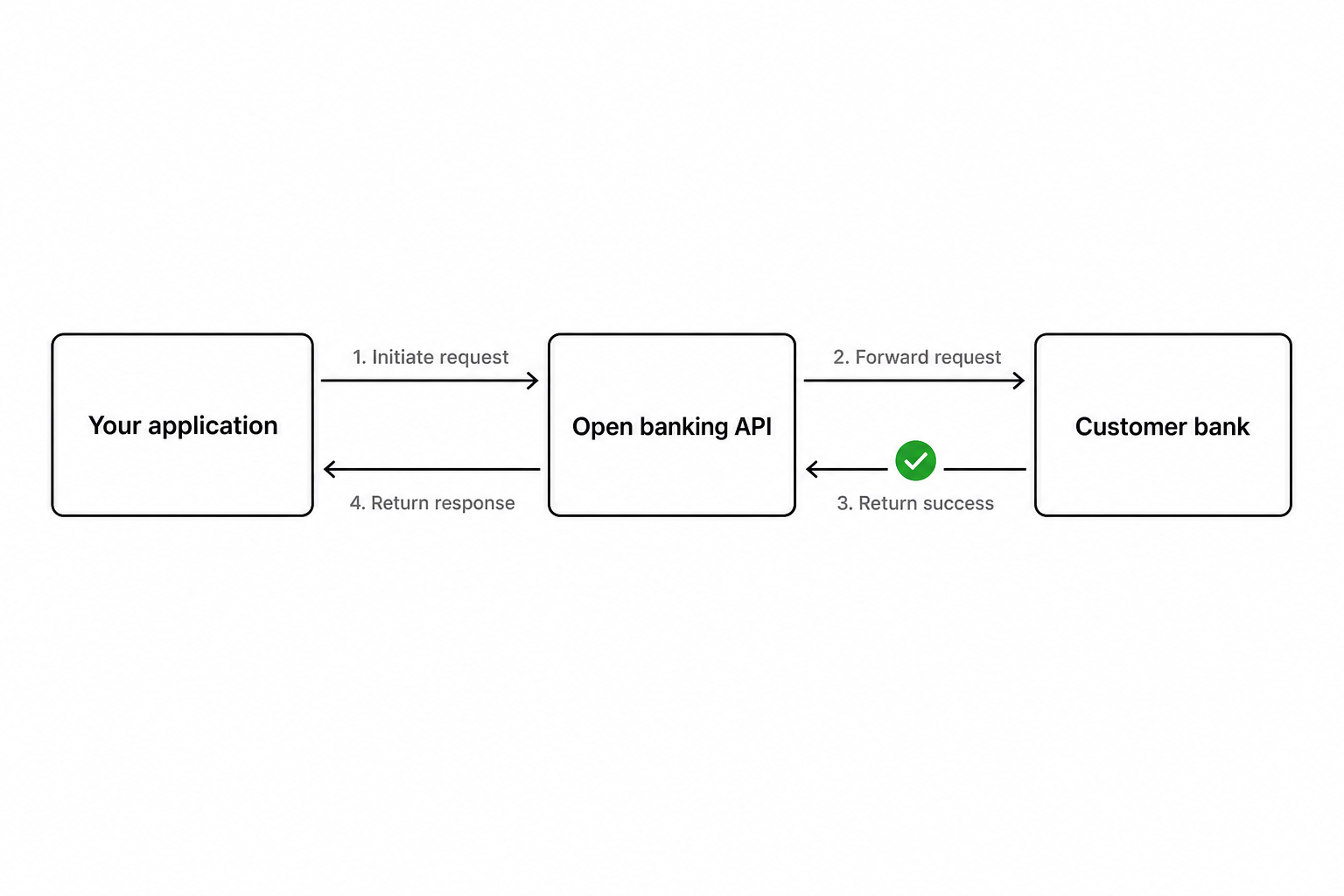

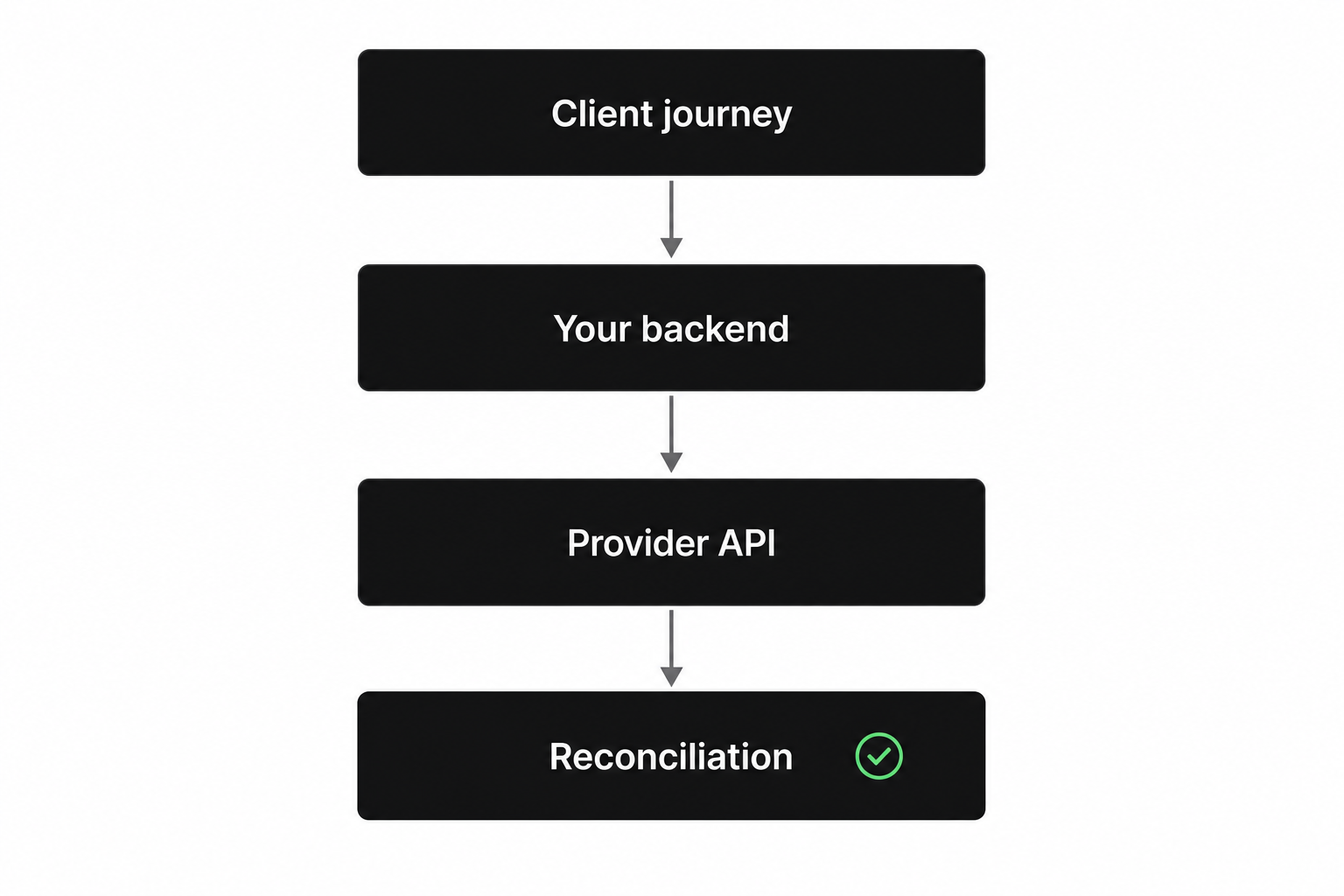

How do you structure the integration architecture?

Your application owns UX, ledger, and idempotency; the provider owns bank connectivity. A typical EU B2B stack has four layers:

- Client journey — redirect or embedded flow where the customer selects their bank and approves consent

- Your backend — creates payment or data requests, stores internal IDs, validates webhooks

- Provider API — routes to ASPSPs, normalises responses, emits status events

- Reconciliation — maps provider references to invoices, subscriptions, or payout batches

Enterprise PSPs sometimes add an orchestration layer that routes across two providers for failover or per-bank economics. That is a build-vs-buy decision, not a v1 default. For a single-provider v1, keep your abstraction thin: one interface in your codebase so you can swap providers later without rewriting checkout.

Link payment initiation vs data-only flows in AIS vs PIS open banking when your scope includes both — mixing them in one consent screen confuses customers and support.

What should you test in sandbox before production?

Run happy path, failure path, and webhook replay in sandbox with production-shaped payloads. Sandbox quality varies by provider and bank — treat institution-level behaviour as something you verify, not something marketing pages guarantee.

Minimum test matrix:

| Scenario | What you assert |

|---|---|

| Successful payment | Webhook arrives; ledger status updates; idempotent retry does not double-charge |

| User cancels at bank | Your UI shows recoverable state; no orphan ledger entry |

| Insufficient funds | Failure reason maps to customer messaging and dunning rules |

| Timeout / unknown | Retry policy and support playbook defined |

| Expired consent (data) | Re-auth flow tested for verification or affordability use cases |

| Multi-currency entity | Separate creditor IDs per country if your finance model requires it |

Schedule engineering-led reviews with finalists — not slideware demos. Developers evaluating API ergonomics should cross-read best open banking API providers for developers (2026) for sandbox and documentation criteria; this article focuses on your integration checklist, not vendor rankings.

According to Open Banking Limited, UK open banking adoption continues to grow with industry-led standards updates — EU teams should still validate per-country bank behaviour because sandbox coverage labels do not always match production success rates.

How do webhooks and idempotency prevent duplicate payments?

Treat every webhook as untrusted until verified, and every outbound request as retryable. Open banking flows are asynchronous: the customer may complete authorisation seconds or minutes after your API call, and providers may deliver the same event more than once.

Production rules:

- Sign or verify webhook payloads per provider documentation; reject unsigned test traffic in production

- Store idempotency keys on create-payment and create-mandate calls so network retries do not spawn duplicate instructions

- Deduplicate by provider event ID in your ledger — second delivery updates status, not a new row

- Define terminal states (

SETTLED,FAILED,CANCELLED) so late events do not reopen closed accounting periods

Finance ops should see the same reference in your CRM, payment record, and bank statement extract. If references differ by country, document the mapping in runbooks before go-live. For invoice-specific flows, see pay by bank invoice payment for B2B reconciliation patterns that pair well with initiation integrations.

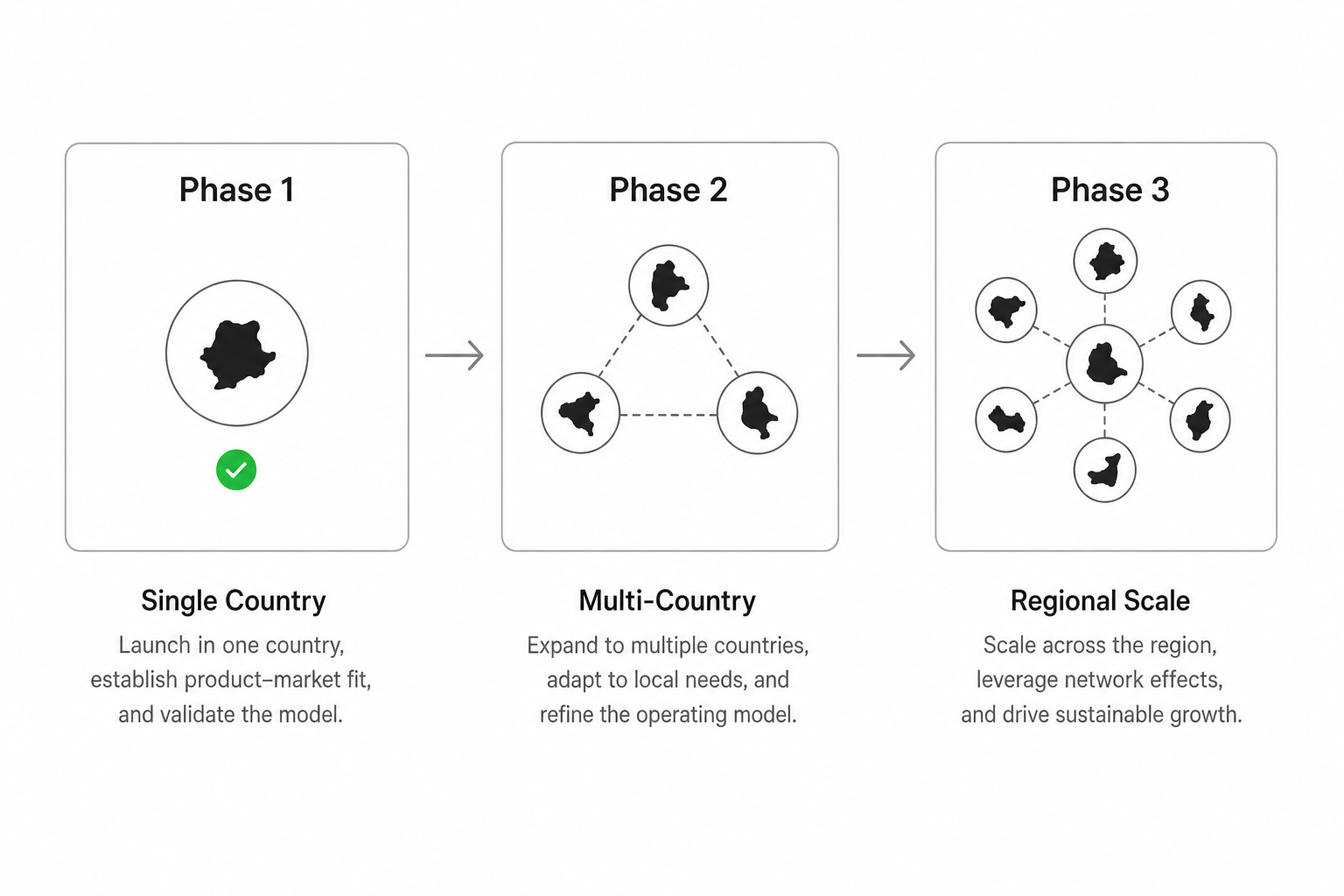

How do you roll out across multiple EU markets?

Sequence countries by revenue and bank concentration, not alphabetically. Launch where your top three institutions are well supported in sandbox, then expand long-tail banks through the same provider rather than opening new integrations per country.

Rollout checklist:

- Legal entity — confirm which licensed provider entity contracts for each market

- Creditor identifiers — SEPA creditor ID, UK service user numbers, or local equivalents configured per entity

- Localised copy — bank picker labels, error strings, and support macros in customer language

- Monitoring — success rate and latency dashboards split by country and bank

- Incident ownership — define when L1 support escalates to provider vs internal payments engineering

PSD3 and PSR will tighten access and conduct rules over the coming implementation window; your integration should not hard-code today's consent copy as permanent. The PSD3 open banking guide summarises what changes on the horizon — budget provider upgrades, not only initial build.

What operational runbooks do you need on day one?

Go-live is when reconciliation load starts, not when engineering merges the PR. Day-one runbooks should cover:

- Customer support — how to identify a stuck payment from internal ID; when to ask the customer to retry vs when to escalate

- Finance — cut-off times, settlement delays per scheme, and how refunds or reversals appear

- Engineering — on-call steps for webhook backlog, certificate expiry, and provider status pages

- Product — feature flags per country so you can disable a market without a full deploy

Run a pilot merchant or internal dogfood period with real money limits before marketing pay by bank broadly. Measure conversion, support tickets per 1,000 attempts, and time-to-reconcile — those three metrics tell you whether to expand scope or fix UX before the next country.

Frequently Asked Questions

What is open banking API integration?

Open banking API integration is the work of connecting your product to a licensed provider's API so customers can pay from their bank, verify an account, or share transaction data with consent. Your team builds checkout or onboarding UX and ledger mapping; the provider maintains bank connections and regulatory requirements across EU institutions.

How long does open banking API integration take?

A focused v1 — one use case, one or two countries, single provider — often takes weeks to a few months depending on sandbox quality, internal compliance review, and reconciliation complexity. Multi-country rollout with failover or custom orchestration typically takes longer; direct bank adapters without a provider are measured in quarters or years.

Do you need a banking licence to integrate open banking?

Usually no. Most B2B products integrate through a licensed payment or account-information provider that holds the regulatory permissions. You remain responsible for customer experience, data handling under GDPR, and accurate ledger treatment. If you operate as a payment institution already, you may mix direct and partner connections — see build vs buy guidance for that fork.

What are open banking webhooks used for?

Webhooks notify your backend when a payment status changes, a mandate is confirmed, or data access is ready. They let you update orders, subscriptions, and finance records without polling. Production integrations must verify webhook authenticity, handle duplicate deliveries idempotently, and map provider statuses to your internal ledger states.

How do you test open banking APIs before going live?

Use the provider sandbox to run successful payments, user cancellations, insufficient funds, and timeouts. Replay webhooks to confirm idempotency. Validate institution-level behaviour for banks your customers actually use — not only demo institutions. Include finance in a pilot with real references and settlement timing before marketing the flow.

What is the difference between AIS and PIS integration?

Payment initiation (PIS) integrations move money — checkout, invoices, payouts. Account information (AIS) integrations read transaction and balance data for verification, affordability, or reconciliation. They require different consent copy and retention rules; many products start with PIS for revenue flows and add AIS when onboarding or risk workflows need bank-verified data.

How do you choose a provider for integration?

Define one user story, list countries and banks that matter, filter vendors on institution-level coverage for that job, and run sandbox tests with your engineers driving the agenda. Compare total cost including failed payments and ops load, not headline per-call fees. When your scope is documented, use the provider-matching form to shortlist finalists before contract negotiation.

Conclusion

Open banking API integration succeeds when you scope one measurable outcome, prove sandbox behaviour for banks your customers use, and treat webhooks as the source of truth for your ledger. EU B2B teams that skip those steps ship flows that look finished in staging but create reconciliation debt in production. Start narrow, measure conversion and match rates, then expand countries through the same provider abstraction — and revisit orchestration only when uptime or economics force it.

Related articles

- PSD3 Open Banking: What EU Teams Should Plan Now

If you rely on bank APIs to collect payments, verify accounts, or pull transaction data, PSD3 open banking is the EU package that will reset your integration r…

- Best Open Banking API Providers for Developers (2026)

<!-- refreshed from API_overview_text.md 2026-06 --> Your team should not pick an open banking API provider from a headline bank count. The best open banking A…

- Pay by Bank Invoice Payment: B2B Collection Without Card Fees

Finance teams add pay by bank invoice payment when card fees on large B2B invoices, slow manual transfers, and reconciliation gaps cost more than a short bank-…