Build vs Buy Open Banking: When to Partner or Build In-House

Build vs buy open banking is the decision that determines whether your first live bank payment ships in weeks or years. Most EU B2B teams should buy — integrate a licensed provider and focus on checkout, verification, or recurring flows that move revenue. A smaller set builds when they already hold payment institution status, need a proprietary orchestration layer across multiple aggregators, or cannot accept a single vendor's roadmap. This guide compares both paths on speed, cost, risk, and ops load so payments and product leads pick the right default — and know when to revisit it.

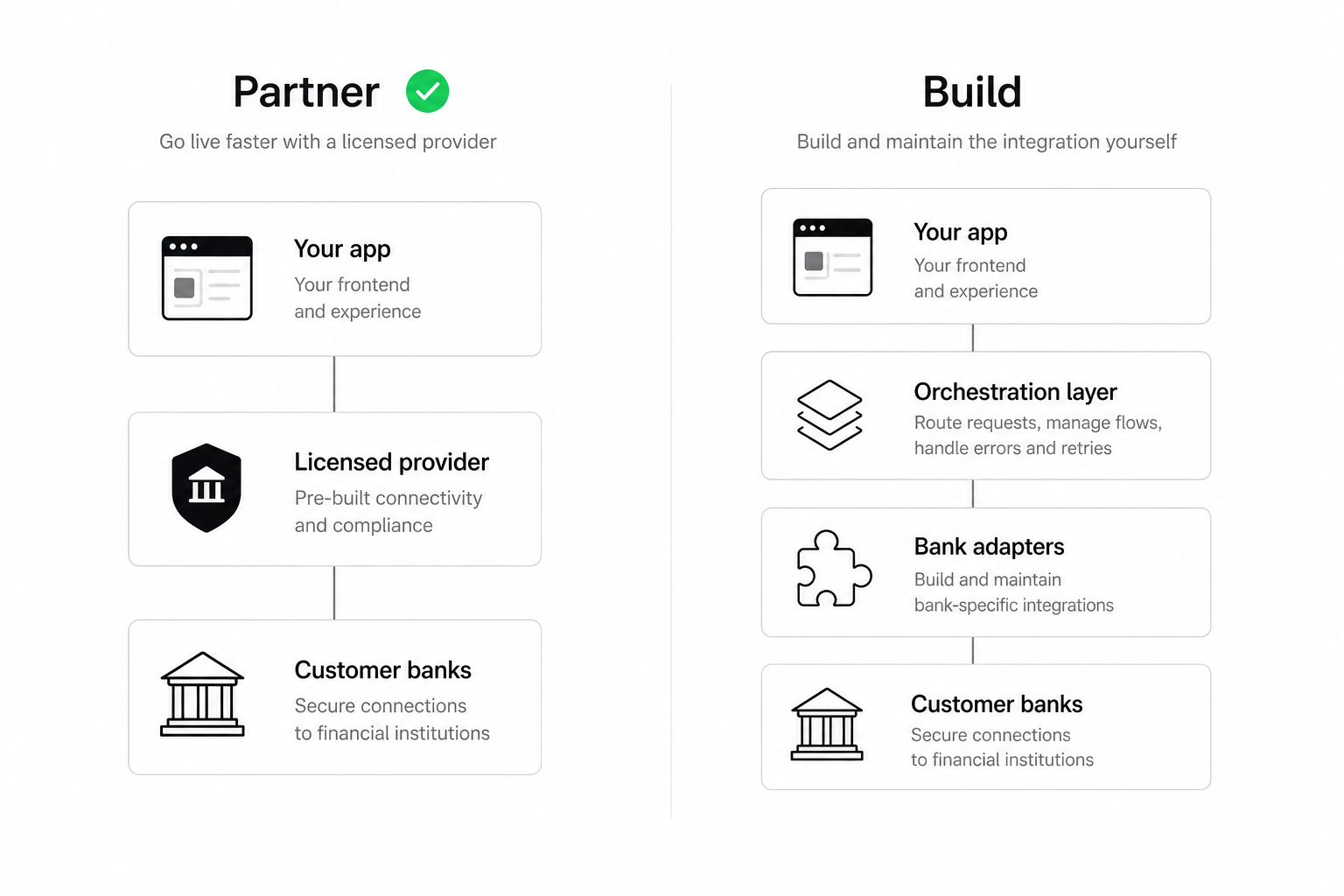

Build vs buy open banking: Whether you integrate a licensed third-party provider ("buy") or develop bank connections, consent flows, and operational tooling yourself ("build"). The buy path gets you to production faster; the build path trades time and compliance load for control over routing, failover, and per-bank economics.

When should you buy (partner with a provider) instead of building?

Buy by default if you are a non-bank product company shipping pay by bank, account verification, recurring collection, or payouts for the first time. A licensed partner holds bank relationships, regulatory packaging, and scheme updates — you integrate one API, map webhooks to your ledger, and measure conversion. You ship revenue in weeks to months instead of staffing a bank-integration programme measured in years.

Partnering wins when:

- Speed matters — you need one corridor live before the next funding or renewal cycle

- Coverage is wide — customers bank across many EU countries and institutions

- Team size is lean — fewer than five engineers can own payments end-to-end

- Regulatory scope is new — you do not already operate as a payment institution

The trade-off is dependency: new banks, scheme changes (such as UK commercial VRP or PSD3-driven access rules), and incident response partly follow your provider's roadmap. That is acceptable for most v1 products if you validate sandbox behaviour and contract exit terms up front. For shortlisting vendors before you commit, see how to shortlist open banking providers.

When does building open banking in-house make sense?

Build (or build a thick orchestration layer) when control over routing, settlement, or multi-vendor failover is a core product differentiator — not a nice-to-have. Typical profiles:

- Existing payment institution or e-money licence — you already run compliance, treasury, and bank ops; adding open banking is an extension, not a greenfield licence project

- Proprietary orchestration — you route traffic across two or more aggregators by cost, success rate, or country, and need your own abstraction layer (common among large PSPs and platforms)

- Dominant single-bank volume — one or two ASPSPs account for most traffic; direct integration returns better economics or UX than a middle layer

- Strict uptime SLAs — hybrid architecture with primary and secondary paths is non-negotiable for your ICP

Building does not mean ignoring partners entirely. Many "build" strategies are hybrid: one production provider plus a secondary for failover, or aggregator for long-tail banks and direct links for your top three institutions. The ops cost is real — you need people who understand consent revocation, webhook idempotency, and reconciliation across entities.

According to the European Banking Authority, EU payment and access rules continue to evolve (including PSD3/PSR implementation timelines). In-house teams must budget for regulatory change, not only initial API work. If your primary question is which provider to partner with, start from how to choose an open banking provider in the EU rather than assuming build is on the table.

What does a 12-month total cost model include?

Compare total cost of ownership, not headline per-transaction rates. A cheaper API with poor webhooks or missing banks often costs more in engineering and finance time.

| Cost bucket | Buy (partner) | Build / hybrid |

|---|---|---|

| Integration | Provider SDK + sandbox (weeks–months) | Bank adapters, consent UX, orchestration (quarters+) |

| Licences & compliance | Bundled in partner fees | PI/EMI status, audits, reporting if you operate rails |

| Per-successful event | Per call, platform fee, or enterprise commit | Bank scheme fees + infra + ops headcount |

| Failed payments | Billing rules vary — model explicitly | Same, plus retry logic you maintain |

| Ops & support | Provider incident comms + your L2 | You own L1–L3 for routing and reconciliation |

| Regulatory change | Mostly provider-delivered | Your compliance team + eng backlog |

Build a 12-month model with realistic volumes: successful payments, verifications, countries, and expected failure rates. Include one FTE-equivalent of engineering and finance ops unless you already have a payments platform team. Pricing model detail lives in the EU choose guide; this article focuses on the build vs buy fork, not renegotiating every fee line.

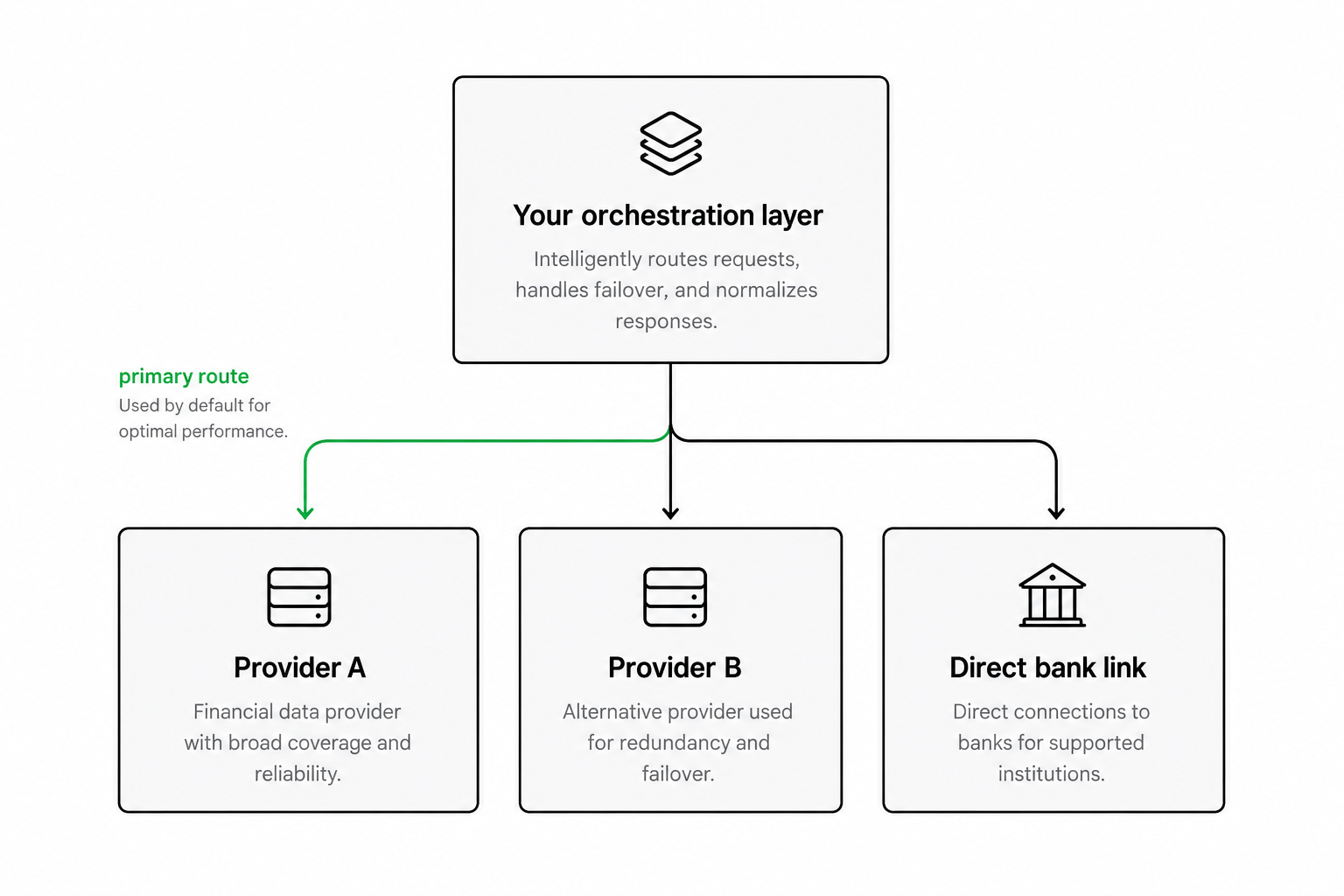

How do hybrid and multi-provider setups work?

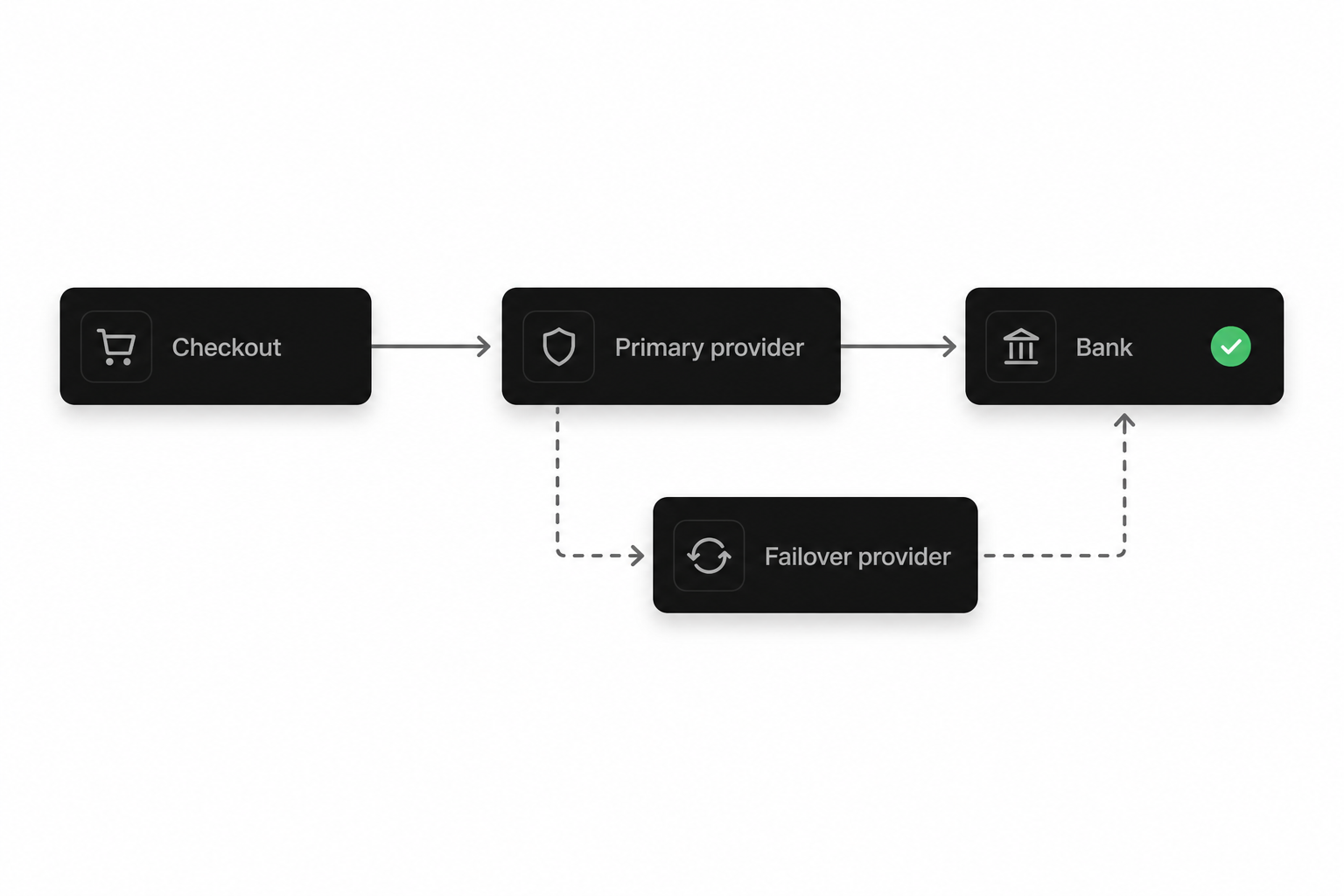

Hybrid is the middle path: partner for production volume, build orchestration when a single vendor cannot meet uptime or coverage targets. Common patterns:

- Primary + failover — route to provider A; on timeout or bank error, retry provider B for the same institution if contractually allowed

- Long tail + direct — aggregator for hundreds of banks; direct ASPSP link for the three institutions that drive 70% of volume

- Use-case split — one provider for checkout initiation, another for account verification, unified in your ledger

Each pattern adds operational complexity: duplicate sandbox testing, split reconciliation references, and clear customer-facing error handling. Justify hybrid only when measured downtime or conversion loss from a single-vendor approach exceeds the ops tax. For aggregator-specific evaluation, see open banking aggregator comparison 2026.

What should engineering validate before you commit?

Whether you buy or build, run the same production-shaped tests before signing:

- Happy path — consent, payment or verification, webhook to ledger, idempotent retry

- Failure path — insufficient funds, user cancel, bank timeout, expired consent

- Reconciliation — payer reference, IBAN, settlement timing match finance expectations

- Multi-entity — if you operate separate creditors per country, test each in sandbox

For buy: schedule a technical review where your engineers drive the agenda, not a slideware demo. For build: prove one bank adapter and one provider adapter behind the same orchestration interface before scaling the backlog.

Developers evaluating API surface and sandbox quality should cross-read best open banking API providers for developers (2026) — it complements this decision guide without replacing the commercial build vs buy frame.

Frequently Asked Questions

What does build vs buy mean for open banking?

It is the choice between integrating a licensed open banking provider (buy) and developing bank connections, consent flows, and operational tooling yourself (build). Most EU B2B teams buy for v1 to ship pay by bank, verification, or recurring flows faster; build suits licensed payment businesses or platforms that need proprietary routing across multiple providers.

Should a startup build its own open banking integration?

Usually no. Startups rarely hold payment institution licences or bank ops teams. Partner with a regulated provider, pilot one country and use case, measure conversion and reconciliation, then revisit build only if unit economics or uptime requirements outgrow a single vendor.

When is building an open banking orchestration layer worth it?

When you already process high payment volume, need failover between providers, or must optimize cost and success rate per bank — and you have engineering and ops capacity to maintain routing, webhooks, and compliance across entities. Enterprise PSPs often build this layer; typical SaaS or marketplace products do not need it for v1.

How much does it cost to build open banking in-house?

There is no single number — costs include licences (if you operate as a PI/EMI), bank scheme fees, engineering for adapters and consent UX, compliance, and ongoing regulatory change. A 12-month model should include failed-payment handling and finance ops, not only successful API calls. Partnering converts much of that into predictable provider fees.

Can you use both build and buy approaches together?

Yes. Hybrid setups are common: one primary provider for production, a secondary for failover, or an aggregator for long-tail banks plus direct links for top institutions. The trade-off is operational complexity — duplicate testing, split reconciliation, and incident ownership.

How long does each path take to reach production?

A focused partner integration for one use case and corridor often takes weeks to a few months, depending on sandbox quality and internal compliance review. Building direct bank connections or a full orchestration layer typically takes quarters to years, especially across multiple EU markets.

How do I choose a provider if I decide to buy?

Define one user story and your top countries and banks, filter vendors on institution-level coverage for that job, run sandbox happy and failure paths with engineering, then compare total cost on two to four finalists. When you are ready to compare providers against your build vs buy constraints, use the provider-matching form to share markets, use cases, and volume before deep RFP work.

Conclusion

Build vs buy open banking is a speed-versus-control trade-off, not a moral choice. Partner for v1 unless you already run licensed payment operations or need multi-provider orchestration as core infrastructure. Model 12-month total cost — integration, failures, ops, regulatory change — not only API list prices. Validate the same production flows in sandbox whether you buy or build. Revisit the decision when volume, markets, or uptime SLAs outgrow your first architecture — many teams start with buy, prove unit economics, then add orchestration selectively.

Related articles

- ASPSP Definition: What It Means in Open Banking (PSD2)

If your customers pay from a bank account or you verify IBANs before payout, you depend on ASPSPs — the institutions that actually hold those accounts. ASPSP d…

- Open Banking Aggregator Comparison 2026: EU TSP Evaluation

Open banking aggregator comparison 2026 matters when your team needs many EU banks without building dozens of direct integrations. Aggregators — licensed third…

- Open Banking Provider Comparison: What to Evaluate

Open banking provider comparison is not a feature checklist race. EU B2B teams compare providers because a wrong fit shows up as failed payments, slow payouts,…