Open Banking Aggregator Comparison 2026: EU TSP Evaluation

Open banking aggregator comparison 2026 matters when your team needs many EU banks without building dozens of direct integrations. Aggregators — licensed third-party providers (TSPs) that connect to account servicing payment service providers (ASPSPs) on your behalf — trade a single API contract against less control per bank. This guide explains what aggregators do, who should use one, which dimensions separate strong from weak fits, and how to shortlist in two weeks without treating any vendor as a default winner.

Open banking aggregator: A regulated provider that connects your product to many customer banks through one integration — so you can initiate payments, verify accounts, or read transaction data without negotiating separate technical links with each ASPSP.

What is an open banking aggregator?

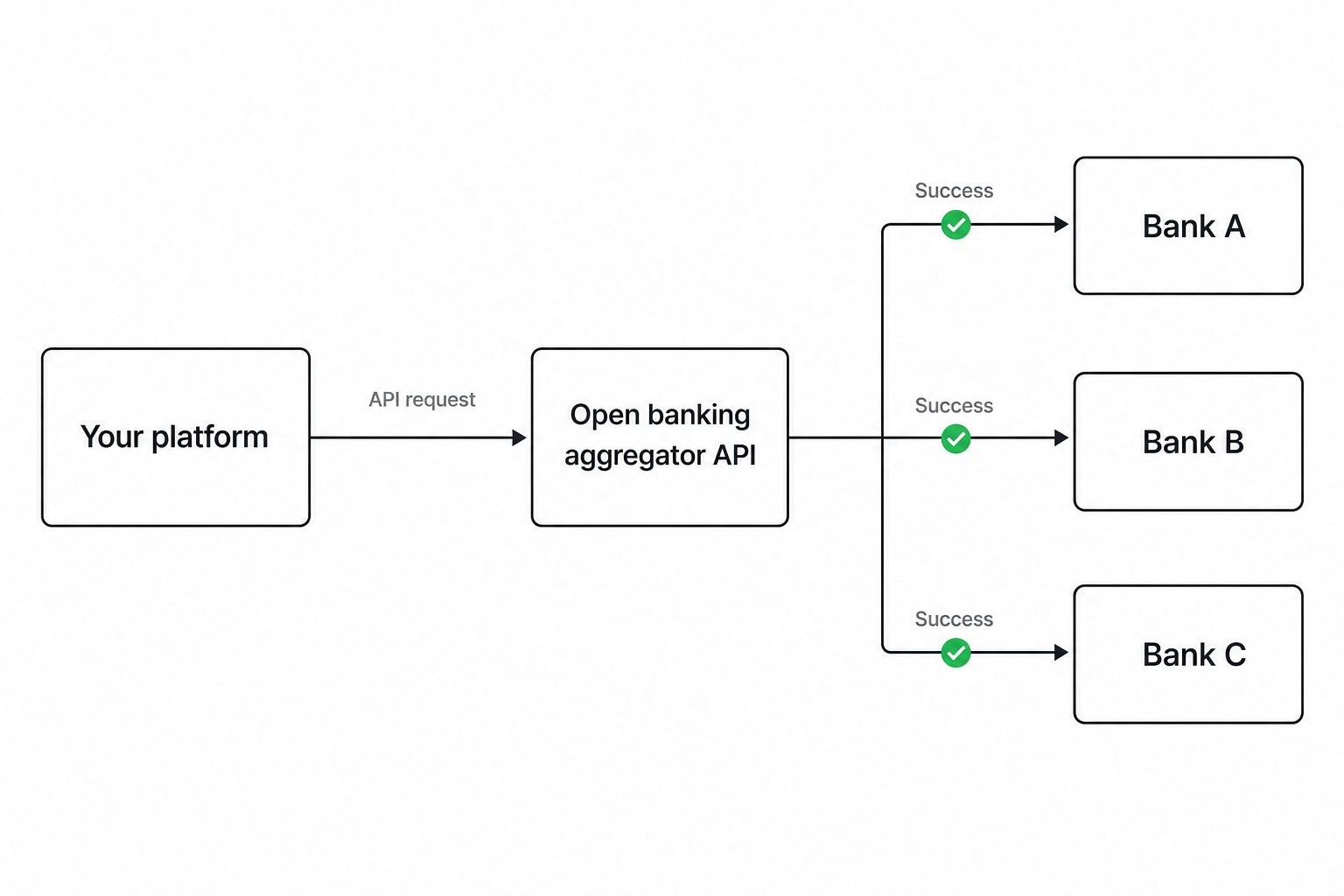

An open banking aggregator is a licensed third-party that maintains connections to many banks and exposes them through a unified API. Your engineers integrate once; the aggregator handles bank-specific redirects, consent flows, and protocol differences behind that surface. You still need customer consent for each access, but you avoid staffing a bank-by-bank integration programme.

Aggregators are not the same as direct bank APIs. A direct link means you contract with one ASPSP (or a small set) and integrate its proprietary or PSD2 interface yourself. Aggregators sit in the middle when your roadmap spans countries, use cases, or institutions faster than your team can ship native connectors.

For a broader evaluation framework that covers any provider type — not only aggregators — see open banking provider comparison. For initiation vs data rails, see AIS vs PIS in open banking.

Who needs an aggregator vs direct bank connections?

Choose an aggregator when coverage breadth and time-to-market outweigh per-bank control. Typical profiles:

- Multi-country checkout or pay by bank — you need initiation across DE, FR, NL, and more within one sprint cycle

- Verification at scale — onboarding or lending flows that must work on whichever bank the customer uses

- Lean engineering — a small payments squad cannot maintain twenty bank adapters

Consider direct connections when one or two banks dominate your volume and you want maximum control over UX, settlement messaging, or commercial terms with that ASPSP. Some enterprises run a hybrid: aggregator for long tail, direct for top-three institutions.

| Situation | Aggregator tends to win | Direct tends to win |

|---|---|---|

| Bank spread | Many countries, many institutions | One country, 1–3 banks > 80% volume |

| Team size | Under 5 engineers on payments | Dedicated bank-integration squad |

| Use case mix | PIS + AIS on one contract | Single-rail specialist need |

| Speed | Live in weeks on sandbox | Months acceptable for one bank |

Neither path removes compliance work — you still map roles, contracts, and customer messaging. The trade-off is integration surface area vs depth per bank.

Which dimensions should you compare between aggregators?

Open banking API providers and banking API providers marketing pages look similar; production separates on operational detail. Score each aggregator on dimensions that map to money and ops, not slide decks.

Coverage per bank and rail

Request institution lists filtered by payment initiation and account information separately. A bank enabled for AIS may not support PIS on the same aggregator. Match the list to your analytics: top five banks per country, not generic “EU coverage” maps.

Initiation vs data on one contract

If you need pay by bank and account verification, ask whether one agreement covers both rails with consistent user and payment identifiers. Dual contracts double legal review, webhook handling, and reconciliation logic.

Webhooks, idempotency, and sandbox parity

Failed payments and stuck verifications surface in webhook reliability and idempotent APIs. In sandbox, replay the same payment creation twice, simulate bank timeouts, and confirm webhook delivery matches production behaviour. Sandboxes that only happy-path test hide the costliest bugs.

Onboarding and commercial shape

Compare time from contract signature to production keys, dedicated support channels, and how pricing ties to successful events vs API calls. Minimum commits and failed-payment charges change unit economics more than headline per-transaction rates.

Pricing shape (not a winner table)

Document each vendor’s model in the same currency and event definition: per successful payment, per verification, platform fee, minimums. Do not rank providers as “cheapest” in a public article — your traffic mix makes one model cheaper than another. Use written quotes and sandbox volume tests instead.

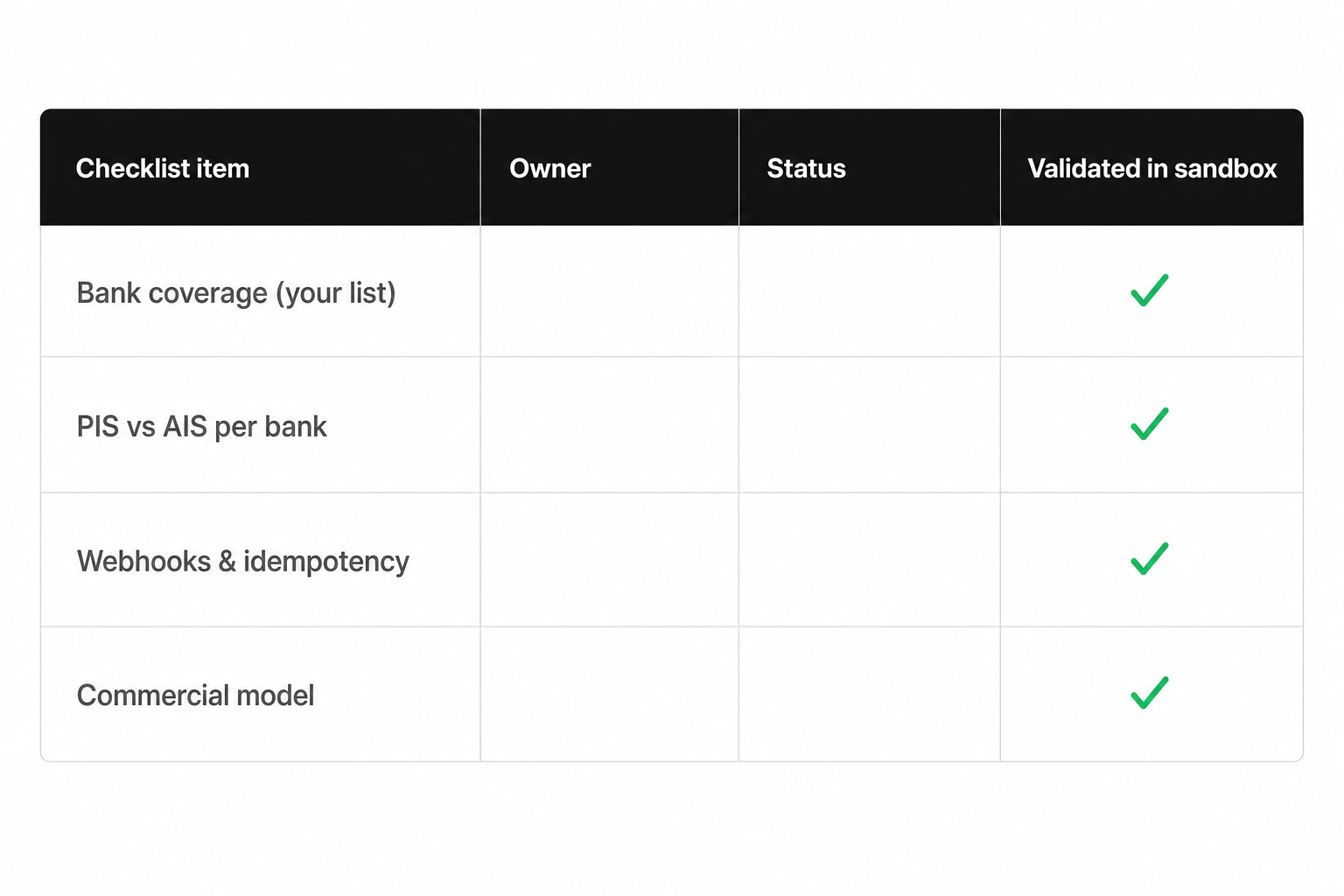

How do you use a comparison table without picking a “winner”?

Build a private matrix your payments and engineering leads own. Rows are mandatory banks and use cases; columns are finalists only after sandbox evidence.

| Dimension | What to record | Pass / fail signal |

|---|---|---|

| PIS coverage | Your top 5 banks per country | Below 95% sandbox success on mandatory list |

| AIS coverage | Same banks for verification | Consent + refresh works on mobile app flow |

| Latency | Redirect to confirmation | p95 within your checkout SLA |

| Webhooks | Payment finality events | No missed events in 100 test runs |

| Support | Incident channel | Named contact before go-live |

| Commercial | All-in cost per success | Model fits your success/failure ratio |

Leave a “notes” column for quirks: banks that only work on mobile, institutions with delayed settlement, or extra steps for business accounts. Two aggregators can both pass coverage slides yet fail different banks on your list — that is why the table is bank-specific, not generic.

How do you shortlist open banking aggregators in two weeks?

A two-week shortlist keeps scope tight: three to four aggregators maximum, one use case, one country cluster first.

Week 1 — evidence

- Day 1–2: Publish your mandatory bank list and primary use case (initiation, verification, or both). Send the same RFP appendix to each vendor — institution export, webhook spec, sandbox access.

- Day 3–5: Engineering runs identical scripts: create payment or consent, complete redirect on mobile where relevant, log status transitions and webhooks.

- Day 6–7: Payments reviews conversion friction (steps, language, errors) and records cost assumptions from written pricing.

Week 2 — decision input

- Day 8–9: Cross-functional scorecard — coverage 30%, conversion 20%, API/webhooks 15%, settlement 15%, commercial 10%, support 10% (adjust weights to your ICP).

- Day 10: Narrow to two finalists; optional spike on edge cases (refunds, business accounts, retry logic).

- Day 11–12: Legal and security review on finalists only.

- Day 13–14: Executive readout with recommendation to pilot — not “winner declared,” but pilot partner + backup with explicit bank-level risks.

Detailed workshop steps live in how to shortlist open banking providers. API-led teams should also read best open banking API providers for developers (2026) for SDK and documentation criteria — complementary to this aggregator-focused comparison.

When you are ready to match requirements to vendors without bias toward a single brand, use the provider directory after your matrix defines non-negotiable banks.

Frequently Asked Questions

What is the difference between an open banking aggregator and an API provider?

In practice the terms overlap: most open banking API providers act as aggregators by connecting many banks through one API. “Aggregator” emphasises breadth of bank connections; “API provider” emphasises the developer surface (REST, webhooks, SDKs). Compare both labels against your bank list and use case, not the marketing name.

How is open banking aggregator comparison 2026 different from comparing banks directly?

A 2026 aggregator comparison focuses on one integration covering many ASPSPs, sandbox parity across those institutions, and TSP commercial models. Direct comparison means evaluating each bank’s interface and contract separately — lower aggregator fees per call but higher build and maintenance cost across countries.

Which open banking aggregators cover the most banks in the EU?

Published bank counts are not comparable across vendors without the same rail filter (initiation vs data) and the same institution identifiers. Ask each finalist for an export matched to your mandatory list and validate in sandbox; coverage that matters is your customers’ banks, not the largest integer on a slide.

Should I use one aggregator for payments and another for account data?

Use one aggregator when a single contract delivers both rails with consistent identifiers and reconciliation. Split vendors only when evidence shows disjoint bank wins that outweigh dual integration, dual legal review, and split finance ops — common in niche specialists, rare for greenfield products.

How do banking API providers price aggregator access in 2026?

Models vary: per successful payment, per verification, monthly platform fees, and minimum commits. Normalise quotes to cost per successful outcome on your expected success rate, including failed redirects you still pay for. Get failure and refund handling in writing before pilot.

When should I compare open banking providers instead of only aggregators?

Compare the full open banking provider landscape when you might blend aggregator access with a direct bank link, a card acquirer, or a vertical specialist. Start from use case and bank list — aggregator vs direct is an implementation choice, not the first question. The open banking provider comparison framework covers that wider lens.

Conclusion

Open banking aggregator comparison 2026 is an exercise in bank-level evidence, not logo selection. Define your use case and mandatory institutions, test initiation and data separately in sandbox, score finalists on webhooks and commercial fit, and pilot with explicit risks — especially on mobile flows and business accounts. The right aggregator is the one that reliably delivers your outcomes on the banks your customers actually use.

Related articles

- Build vs Buy Open Banking: When to Partner or Build In-House

Build vs buy open banking is the decision that determines whether your first live bank payment ships in weeks or years. Most EU B2B teams should buy — integrat…

- ASPSP Definition: What It Means in Open Banking (PSD2)

If your customers pay from a bank account or you verify IBANs before payout, you depend on ASPSPs — the institutions that actually hold those accounts. ASPSP d…

- Open Banking Provider Comparison: What to Evaluate

Open banking provider comparison is not a feature checklist race. EU B2B teams compare providers because a wrong fit shows up as failed payments, slow payouts,…