Open Banking Affordability Check: How EU Teams Map Obligations

Self-declared budgets and uploaded bank statements still miss the repayments, rent, and buy-now-pay-later instalments that actually leave a customer's account each month. An open banking affordability check reads consented transaction history after the applicant authenticates in their banking app — so credit, rental, and subscription teams score disposable income from source-verified outflows, not guesswork. This guide explains how the flow works, which obligation signals matter in production, where it fits alongside income verification open banking, and how to evaluate providers without building every EU bank connection yourself.

Open banking affordability check: Assessing whether a customer can afford a new commitment by analysing consented bank transaction history — mapping recurring outflows, estimating disposable income, and feeding your credit or rental policy with source-verified obligation data instead of self-declared figures alone.

What an open banking affordability check delivers

Affordability teams need to know whether a new loan instalment, rent payment, or subscription fits what the customer already spends — not what they typed on a form. Open banking delivers four measurable outcomes:

- Fewer overstated budgets — recurring outflows from the source account are harder to omit than self-declaration

- Faster decisions — structured obligation signals in minutes instead of manual statement review

- Lower first-payment default — catch hidden BNPL, overdraft reliance, and duplicate loan repayments before approval

- Audit-ready evidence — timestamps and categorised transactions for credit committees and rental disputes

The customer stays in control: they choose the bank, approve access in the banking app, and can revoke consent under standard EU renewal rules. You integrate one licensed open banking provider — you do not wire each EU bank yourself.

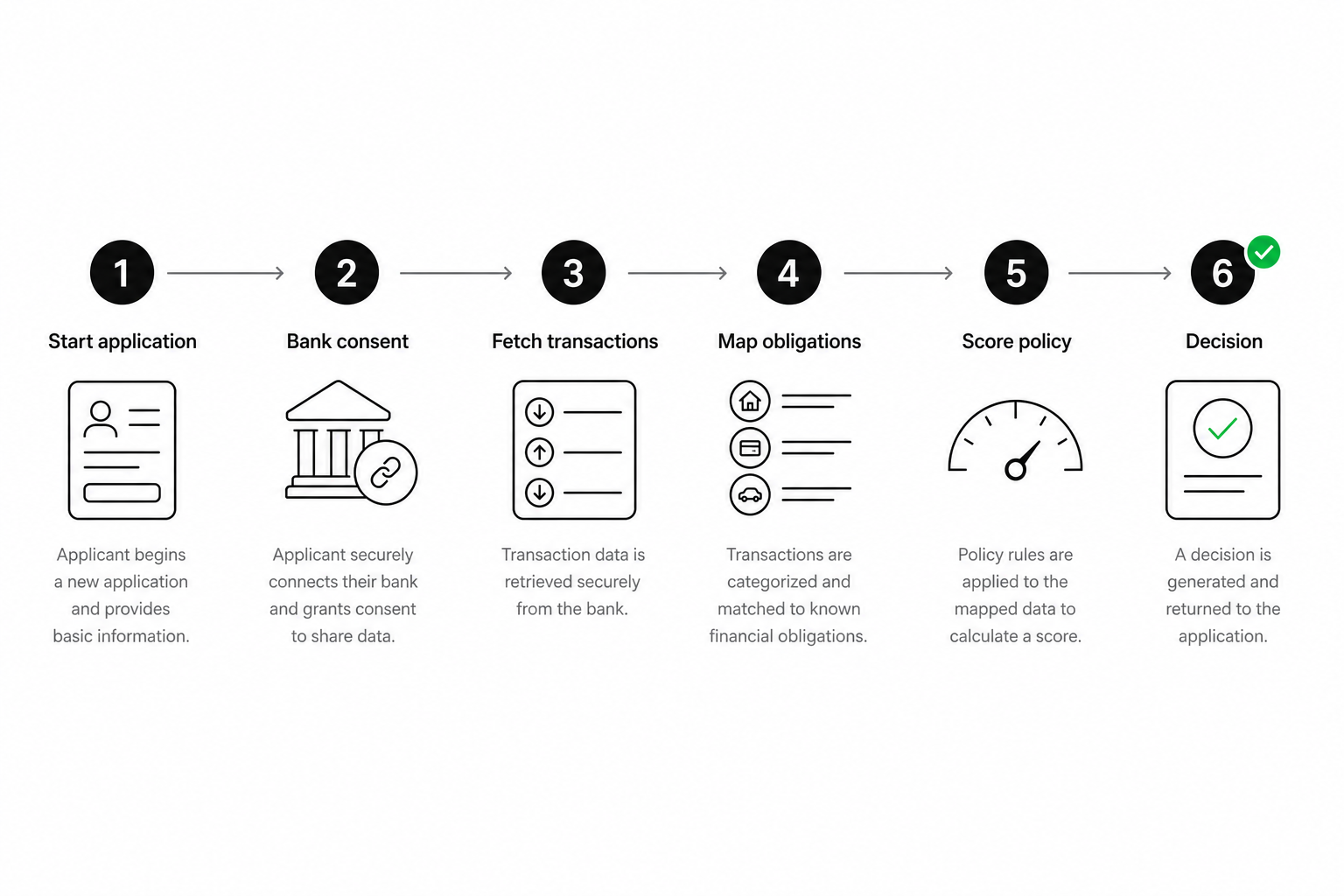

How the affordability check flow works

A typical production path looks like this:

- Applicant starts in your loan, rental, or subscription journey and chooses "verify affordability with bank."

- Bank selection — they pick their institution from your provider's coverage list.

- Authentication — they approve in mobile or web banking (strong customer authentication).

- Data fetch — your provider returns accounts and transaction history within the consented scope.

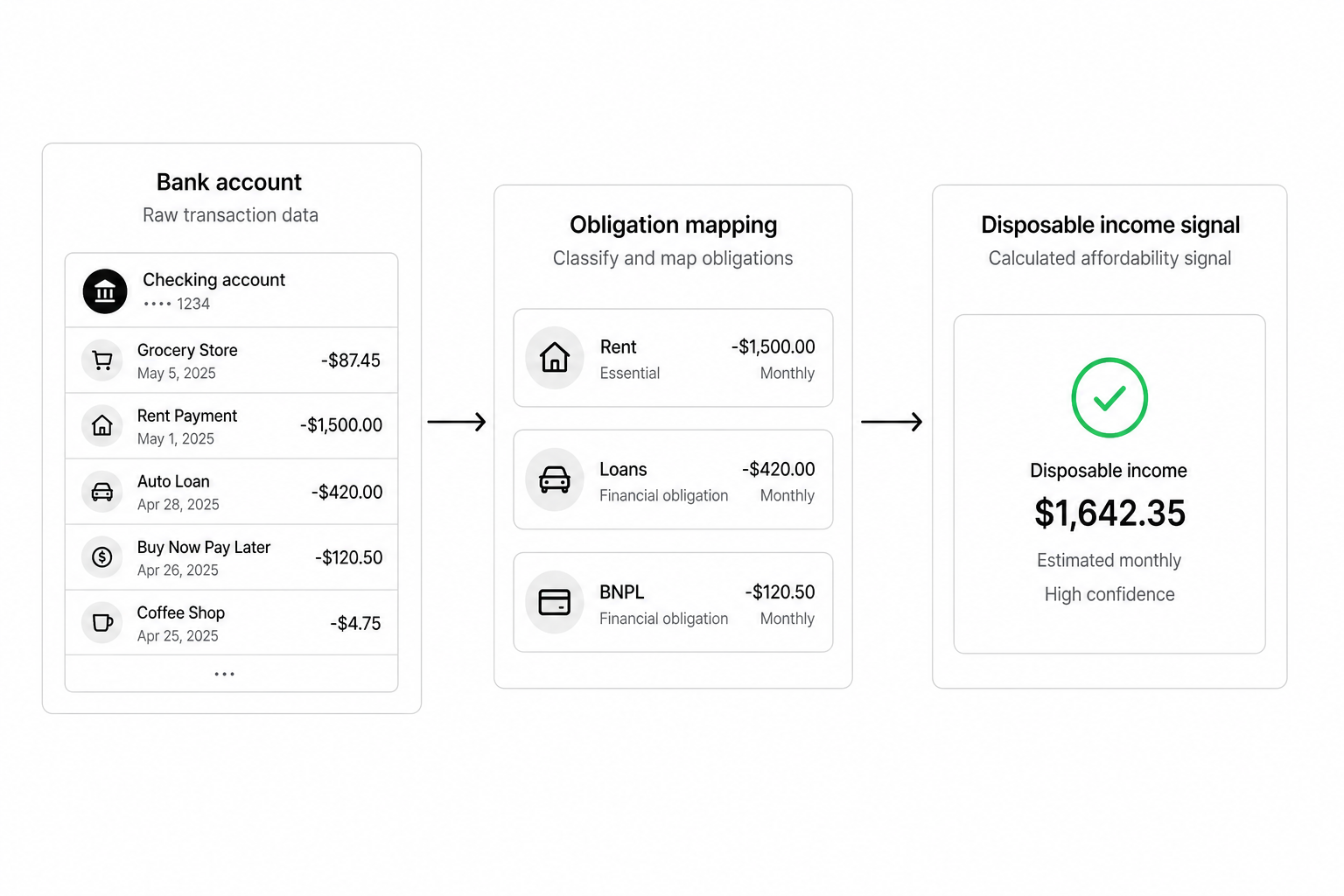

- Obligation mapping — your engine or the provider's models identify recurring debits, loan repayments, rent-like transfers, and BNPL instalments.

- Policy scoring — your rules compare disposable income against the new commitment and return approve, refer, or decline.

Engineering work concentrates on UX, policy thresholds, and exception handling when no clear recurring pattern exists — not on maintaining hundreds of bank APIs.

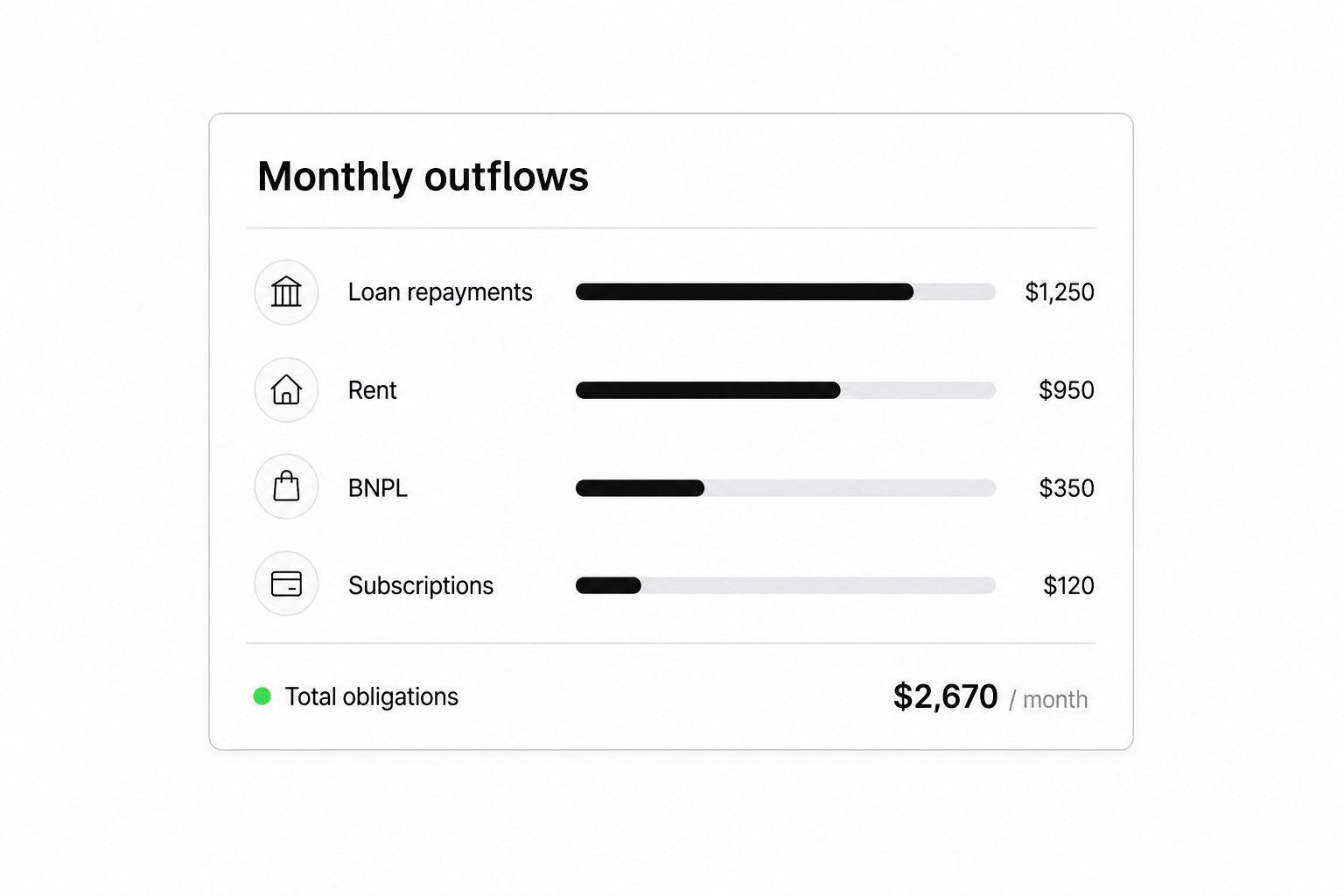

Which obligation signals teams actually score

Affordability is not a single number — it is a set of patterns your policy weights. Teams commonly evaluate:

Recurring loan and credit repayments

Existing personal loans, car finance, credit-card minimums, and overdraft usage show committed outflows before you add another instalment. Duplicate or undisclosed loans are a common reason to refer applications that looked fine on a payslip alone.

Rent and housing costs

Regular transfers to landlords, property managers, or standing orders labelled as rent often appear even when applicants understate housing on forms. Joint accounts and split rent need explicit rules — some teams require the primary salary account; others accept a secondary account with documented co-tenancy.

Buy-now-pay-later and subscription stacks

BNPL instalments and stacked digital subscriptions rarely appear on payslips but show clearly in transaction history. Policy caps on total BNPL exposure prevent approving customers already committed to multiple short-term plans.

Income minus obligations

Affordability checks pair with income verification open banking: inflows confirm salary; outflows confirm what already leaves the account. Disposable income is the gap your limit engine uses — not gross salary alone.

Red flags that trigger manual review

Round-number self-transfers, sudden balance drops before application, gambling merchant codes, or accounts with no history may indicate thin files or first-party abuse. Open banking complements — does not replace — bureau data and identity checks.

Where affordability checks fit: lending, rental, and subscriptions

Different verticals share the same primitive — obligation mapping from consented bank data — but weight signals differently.

| Vertical | Primary question | Typical obligation focus |

|---|---|---|

| Consumer lending | Can they afford this instalment? | Existing loans, BNPL, overdraft |

| Rental / lettings | Can they afford this rent? | Rent history, housing transfers, income stability |

| Subscriptions / telco | Will they pay recurring charges? | Subscription stack, failed payment patterns |

| SME credit | Can the business service debt? | Operating outflows, tax movements, seasonality |

For the full credit lifecycle — origination, disbursement, collections — see open banking for lending. Affordability is usually step two after income confirmation, before disbursement verification.

When bank-verified affordability beats self-declaration

| Scenario | Self-declared budget / PDF | Open banking affordability check |

|---|---|---|

| Speed | Days of manual statement review | Minutes when bank is supported |

| Hidden obligations | BNPL and informal loans often omitted | Recurring debits visible in history |

| Fraud risk | Inflated income, understated costs | Bank-authenticated inflows and outflows |

| Thin files | Weak when no payslip | Cash-flow evidence when bureau history is sparse |

| Joint accounts | Hard to interpret from one document | Rules for which account to link |

Self-declaration still matters for edge cases: cash-heavy sectors, applicants who refuse bank connection, or markets with low bank coverage. Mature teams run hybrid policies — open banking first, documents and bureau as fallback — and measure auto-approval rate versus manual review cost.

Product and operational considerations

Outcome-first copy beats jargon: "Connect your main account to confirm your regular payments" works better than acronym-heavy modals.

Before launch, align product, risk, and legal on:

- Purpose limitation — affordability decisioning only, stated clearly at consent

- Retention — how long you store raw transactions versus derived features

- Automated decisions — adverse action workflows when scoring declines

- Re-consent — operational alerts before access expires on ongoing monitoring

- Joint accounts — documented rules so ops knows when to refer

Under forthcoming EU payment rules — including the 180-day re-consent cycle outlined in the PSD3 open banking package — build refresh workflows into your ops calendar so affordability signals do not silently go stale mid-book review.

How to evaluate providers for affordability checks

Prioritise practical criteria over feature checklists:

| Criterion | Why it matters for affordability |

|---|---|

| Bank coverage in your markets | Unsupported banks force fallback paths |

| Transaction history depth | 90–180 days captures seasonal patterns |

| Categorisation quality | Rent, loan, BNPL labels reduce manual tagging |

| Income + obligation models | Some providers ship affordability-ready scores |

| Webhook reliability | Ops needs timely fetch completion signals |

| Sandbox fidelity | Test top borrower banks before commercial shortlist |

| Data retention and EU hosting | Align with your legal team's policy |

Run sandbox tests against your top ten applicant banks before any commercial decision. A provider strong for German retail neobanks may be weak for French joint accounts your rental line needs. Provider fit depends on product type, markets, and whether you need data-only or combined payment rails — compare options through a structured shortlist rather than a single vendor narrative.

Frequently Asked Questions

What is an open banking affordability check?

An open banking affordability check assesses whether a customer can afford a new financial commitment by analysing consented bank transaction history. It maps recurring outflows — loans, rent, BNPL, subscriptions — and compares disposable income against the proposed payment, usually through a licensed open banking provider rather than manual statement uploads.

How is an affordability check different from income verification?

Income verification confirms money coming in — salary credits, regular transfers, gig payouts. An affordability check focuses on money going out — existing loan repayments, rent, BNPL instalments, and overdraft usage — to estimate disposable income. Most lenders run both on the same bank connection during underwriting.

Is open banking affordability checking legal in the EU?

Yes. Teams use regulated providers to access account information with explicit customer consent. You typically partner with a licensed entity for regulated activities rather than holding all licences yourself on day one. Legal teams still define purpose, retention, and automated decisioning rules for your products.

Which industries use open banking affordability checks?

Consumer lenders, rental and lettings platforms, telco and subscription businesses, and some SME credit teams use affordability checks to reduce first-payment default and manual statement review. Each vertical weights obligation signals differently — rental teams prioritise housing transfers; lenders prioritise existing credit commitments.

What are the limitations of bank-based affordability checks?

Cash spending, prepaid accounts, and unlinked joint accounts may not appear in the connected history. Applicants can refuse bank connection — you need document and bureau fallbacks. Coverage varies by bank and country; validate your target segments in sandbox before promising instant decisions everywhere.

How long does an open banking affordability check take?

When the applicant's bank is supported and authentication succeeds, fetch and categorisation typically complete in minutes. Manual review adds time when patterns are ambiguous — for example, irregular gig income or unclear rent labels. Engineering and policy design determine how much you auto-decide versus refer.

How do I choose a provider for affordability checks?

Shortlist providers by bank coverage where your customers bank, quality of transaction categorisation, depth of history returned, affordability-ready scoring if you need it, webhook reliability, sandbox access to your priority banks, and contract terms for your sector. Test with real bank connections in sandbox before production rollout.

Conclusion

Open banking affordability checks turn self-declared budgets into source-verified obligation maps — so lending, rental, and subscription teams approve with fewer hidden commitments and less manual statement work. Pair them with income verification on the same connection, keep hybrid fallbacks for unsupported banks, and validate categorisation quality in sandbox before you scale auto-decisions.

Related articles

- Income Verification With Open Banking for EU Lenders

Manual payslips and uploaded PDFs slow underwriting and still miss what actually hits the borrower’s account. Income verification open banking lets applicants…

- Open Banking for Lending: 8 Use Cases for EU Credit Teams

EU consumer and SME lenders still lose days on manual payslips, stale bank PDFs, and self-declared income that does not match what actually lands in the accoun…

- Best Open Banking APIs for Account Verification (2026)

Wrong-IBAN payouts and slow onboarding checks cost more than a bad API choice — they cost support tickets, compliance rework, and customers who abandon before…